I think our dollar is getting too strong, and partially that’s my fault because people have confidence in me. But that’s hurting—that will hurt ultimately. Look, there’s some very good things about a strong dollar, but usually speaking the best thing about it is that it sounds good. It’s very, very hard to compete when you have a strong dollar and other countries are devaluing their currency.

– President Trump, speaking to the Wall Street Journal on April 12, 2017

I’m the king of debt. I’m great with debt. Nobody knows debt better than me.

-President Trump, in an interview with CBS News on June 22, 2016

The King of Debt does not appear to care for King Dollar. Source: Wikipedia

The King of Debt does not appear to care for King Dollar. Source: Wikipedia

If the dollar strengthens significantly, it will have a significant impact on your investment portfolio. Similarly, if the dollar weakens, it will also have an impact on your investment portfolio.

If you are an investor, or, for that matter, if your earnings are denominated in dollars, it’s worth paying attention to what Donald Trump says about the dollar.

I say this because President Trump has enormous influence over what happens to the purchasing power of the dollar. As President, he appoints the Secretary of Treasury and the members of the Board of Governors of the Federal Reserve. Trump signs legislation that will affect fiscal spending. He is in charge of the country’s foreign policy.

For years, Donald Trump has consistently communicated that he wants a weaker dollar. You might be wondering, is this just rhetoric, or does he plan to make appointments and pursue fiscal policies and foreign policies that will actually weaken the dollar? Put more simply, does Trump mean what he says about wanting a weaker dollar?

In my view, it’s more than just rhetoric. Donald Trump is highly motivated to keep interest rates low and devalue the dollar. I say this because of where his own political and business interests lie.* I believe it’s possible to examine Donald Trump’s interests and determine whether Trump is more likely to be a weak-dollar President or a strong-dollar President. So far, I have found four reasons that support my view that he will be a weak-dollar President.

Reason #1: Almost 90% of Donald Trump’s $3.5 billion in estimated net worth is tied to real estate.

Donald Trump is a billionaire, but more importantly, he is a real estate billionaire.

Real estate is an asset class that is highly sensitive to interest rates. When interest rates go up, real estate values decline, and vice versa (all things being equal). Real estate investments are valued according to the present value of their future cash flows. Low-interest rates increase the present value of those future cash flows.

That might be just one of the reasons why Donald Trump recently said, “I do like a low-interest-rate policy, I must be honest with you,” in April 2017.

Real estate also tends to hold its value in an inflationary environment. When the cost of the materials used in constructing a building increase, the replacement costs of existing real estate properties increase commensurately. As a result, property values tend to increase in an inflationary environment.

A decline in the value of the dollar would likely lead to increased rents and increased replacement costs for Trump’s various real estate properties. Conversely, an increase in the value of the dollar would likely result in a decline in property prices. Weak-dollar policies will serve Donald Trump’s investment interests better.

Donald Trump’s business interests are aligned with that of real estate investors who benefit from low interest rates and a weaker dollar.

Reason #2: The majority (~52%) of Donald Trump’s estimated net worth is tied to New York City real estate.

Trump Tower is just one NYC trophy property among many that Donald Trump owns. Source: Wikipedia.

New York City real estate is dependent on the health of the local NYC economy, which is, in turn, dependent on the health of the financial markets. When financial markets boom, so too do New York City and New York City real estate. When financial markets bust, so too does New York City and its real estate.

During the 2008 financial crisis, Trump’s estimated net worth declined by almost 50%, from $3.0 billion to $1.6 billion, and at least one of his properties filed for bankruptcy. That’s what will probably happen again during another financial crisis.

Since the 2008 financial crisis, as markets have rallied, Trump’s net worth has more than doubled, from $1.6 billion to $3.5 billion, driven by increased profits for banks, hedge funds, and wealthy investors located in New York City.

Low-interest rate and weak dollar policies also support the financial markets which should indirectly provide support for President Trump’s New York City real estate empire.

Reason #3: Trump’s various real estate holdings are encumbered with approximately $1.1 billion of debt.

In one important respect, Donald Trump’s financial interests are aligned well with that of the United States. Both Trump and the United States have a lot of loans to pay to creditors.

By depreciating the dollar, President Trump, in effect, reduces his own indebtedness. If the dollar declines in value, Trump would still have $1.1 billion in loans outstanding, but the real (inflation-adjusted) value of those loans would be lower. As a result, the real (inflation-adjusted) value of his net worth would increase substantially.

Let’s use some simple math example to illustrate this concept.

Forbes estimates that Donald Trump owns $4.2 billion in real estate which is encumbered with $1.1 billion of mortgage-related loans. Thus, Donald Trump’s real estate net worth is approximately $3.1 billion ($4.2 billion of real estate assets minus $1.1 billion of debt).

Let’s now assume that Donald Trump manages to devalue the dollar by 50% and that, as a result of a devalued dollar, all real assets double in price. His real estate would then be worth $8.4 billion, but his debts would remain at $1.1 billion. Donald Trump’s real estate net worth would increase from $3.1 billion to $7.3 billion. Because of the debt leverage that Trump is employing, his real estate net worth increases by 135%.

Donald Trump’s weak dollar policies will likely be helpful for real estate investors who have a manageable level of debt leverage.

Reason #4: Donald Trump wants to bring jobs back to the industrial manufacturing states of Michigan, Ohio, Pennsylvania, and Wisconsin.

Without winning these Midwest manufacturing states during the 2016 election, Donald Trump would not be President of the United States today. The states of Wisconsin, Michigan, Pennsylvania, and Ohio provided Trump with a total 64 electoral votes. He won these states by promising to bring jobs back to the United States. Without delivering on his promise, Trump will likely not win these same states again when he runs for re-election in 2020.

If the dollar increases in value, the competitiveness of U.S. manufacturers will decline relative to foreign producers. If the dollar declines in value, the relative competitiveness of U.S. manufacturers will increase. I see no way for Trump to deliver on his promise to the industrial manufacturing states without figuring out a way to reduce the value of the dollar.

To maximize manufacturing jobs in the United States, Donald Trump will make appointments and pursue policies that result in a weaker dollar in an attempt to bring jobs back to the United States and secure his re-election. The companies that will likely benefit from the most from a weaker dollar are U.S. exporters.

Investment Implications of a Weak Dollar

Donald Trump’s commercial and political interests suggest that the President is highly motivated to depreciate the dollar. Doing so will contribute to the real value of his net worth and help his chances of being re-elected. If I’m right, some of the investment implications include the following:

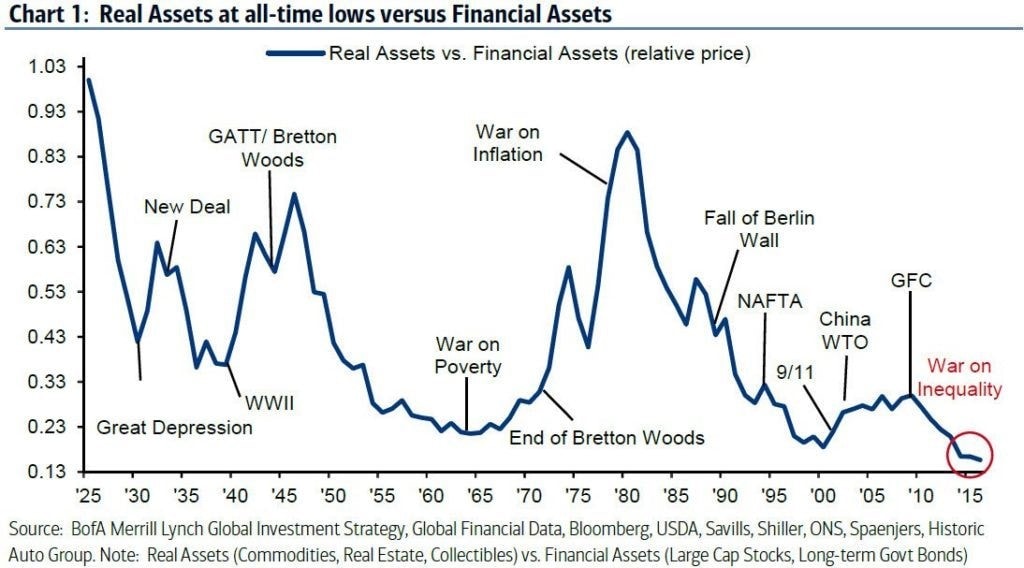

- Real assets: Real assets should maintain their inflation-adjusted values. Owning gold, real estate, and other tangible assets should protect the purchasing power of your investment portfolio as the dollar declines in value. I would expect real estate assets to outperform financial assets (see what happened in the 1970s below).

- U.S. stocks: Although the inflation-adjusted return from owning U.S. stocks during the next ten years may be poor due to high valuation ratios, the U.S. stock market may rise in nominal terms as the dollar declines in value. U.S. corporations that rely on exports should perform better than U.S. companies that rely on imports.

- Foreign stocks: Foreign stocks in countries where valuation ratios are reasonable should outperform U.S. stocks, and a weak dollar will be a strong tailwind for overseas stocks. A few weeks ago, I discussed some of the reasons why South Korea stocks are attractive right now.

- S. bonds: Even if the nominal price of your bonds remains the same during the Trump administration, your bond portfolio might buy less over time as the dollar depreciates.

If you would like to discuss the investment implications of a lower dollar on your investment portfolio, please do not hesitate to reach out to us.

*Source: In my analysis, I am relying on Forbes for estimates related to Donald Trump’s assets and liabilities.

This article is prepared by Pekin Hardy Strauss Inc (“Pekin Hardy”) for informational purposes only and is not intended as an offer or solicitation for business. The views expressed are those of the author as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. The information and data in this article does not constitute legal, tax, accounting, investment or other professional advice. Pekin Hardy cannot assure that the strategies discussed herein will outperform any other investment strategy in the future, there are no assurances that any predicted results will actually occur.