Photo by Gajus

“Get the fundamentals down and the level

of everything you do will rise.”

– Michael Jordan

The stock market has been ripping upwards ever since the U.S. election on November 9th, with investors pouring more than $100 billion into U.S. equity ETFs during the last two months of 2016. As stocks continued to rise into the close of 2016, several bullish Trump-centric investing narratives have been put forth to explain the increase in animal spirits behind this rally. These narratives, we believe, are overly optimistic and incorrectly dismissive of several important fundamental factors that are likely to stand in the way of strong U.S. stock market returns during the intermediate period ahead.

Before discussing the challenging economic fundamentals facing investors, let us first review the bullish stock market narrative we would like to dispel. The financial press, always ready to explain a stock market rally, eagerly suggests that “it’s time to buy U.S. stocks because…”

- Following the playbook of Ronald Reagan, Donald Trump is going to unleash a fiscal stimulus that will accelerate the current U.S. economic recovery; and

- Trump is going to create trade deals that will revive the U.S. manufacturing sector which will boost wages and the economy.

These narratives, in our view, may be misleading and potentially harmful for an investor’s long-term financial health.

In light of the recent stock market rally and a considerable increase in political and economic uncertainty since the election, we think that it is as important as ever for investors to “get the fundamentals down.” With that goal in mind, we offer several counter-points for consideration:

- New Presidents and Recessions

Newly elected Presidents are often greeted with recessions; this has been particularly true with respect to newly elected Presidents who are replacing a retiring two-term President. Barack Obama, George W. Bush, Ronald Reagan, and Gerald Ford all faced recessions in the early years of their administrations, and that was just in the past 50 years. Furthermore, the Great Depression, the Dot-Com Bubble, and the Financial Crisis all transpired just as new presidential administrations were taking office. We provide these data points as a warning that presidential turnover in modern times, have often coincided with economic slowdowns.

- Limited Power

The President has a limited ability to influence the economy, either for good or for harm. Despite the fact that Trump will be working with a House and Senate that are majority-ruled by Republicans, the President’s actions remain limited by the Supreme Court, by Congress, by the economic cycle, by interest rates, by trading partners, and by a myriad of other factors. The way in which these factors will interact with one another during a Trump administration is a complex puzzle, making it difficult for anyone to provide an accurate forecast.

- Economic Cycle Longevity

The U.S. economy has been expanding for the past eight years, which is a relatively long time. U.S. economic expansions have never exceeded ten years without a recession, and, historically, most U.S. economic expansions have lasted fewer than eight years. We do not know precisely when the next recession will begin, but we do believe that we are likely closer to the end of the current expansionary cycle than we are to the beginning.

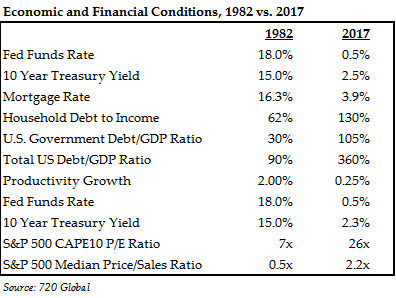

- 2017 is not 1982

The U.S. stock market did indeed experience an enormous bull market during the Reagan administration. However, the bull market in stocks began under Reagan’s watch only after a deep economic recession and a significant bear market in stocks transpired during Reagan’s first two years in office. It is also important to note that stocks were much cheaper at the start of Reagan’s tenure, with the S&P 500 trading at roughly 7x cyclically-adjusted earnings vs 26x today. Furthermore, a credit expansion began in 1982, supporting strong increases in both government and consumer spending during a time when both sectors had ample capacity to lever their balance sheets. Today, the opposite situation exists; interest rates are near a multi-generational low level, while debt levels are at record highs.

- Fiscal Stimulus an Unlikely Savior

We are skeptical that a massive fiscal package will be passed without the impetus of a recession occurring first, given the reluctance of Republicans in Congress. We are similarly skeptical that a stimulus package will provide anything more than a moderate, short-term jolt to the economy, unless the package results in productivity-enhancing investments. Furthermore, if Trump is successful in his goal of reducing the trade deficit, foreign investors will be unlikely to supply the United States with much needed capital for a fiscal stimulus program, because the foreign capital inflows that the United States enjoys today only occur due to the country’s current account deficit.

- Financial Conditions Tightening

The Federal Reserve raised interest rates in December 2016, a few weeks after the election, and Federal Reserve Chairperson Janet Yellen is setting an expectation that, barring unforeseen circumstances, the Federal Reserve will likely raise interest rates three more times in 2017. Unfortunately, as interest rates rise, so too will debt service costs for the Federal government, for local and state governments, for corporations, and for consumers. In an economic recovery where growth has thus far been driven largely by credit expansion, any increase in interest rates should lower economic growth as consumption and investment must be curtailed for increased interest payments.

- Strong Dollar

During the presidential campaign, Donald Trump clearly voiced his interest in seeing a weaker dollar to boost U.S. exports and generate additional U.S. manufacturing jobs. Since the election, the U.S. dollar has not weakened; rather, it has strengthened considerably. A stronger dollar not only makes it harder for Trump to achieve his export goals, but it also reduces corporate profits due to a decline in the dollar value of the overseas profits of U.S.-based multinational corporations. If the dollar remains strong, we expect U.S. corporate profits to decline during 2017, all else equal. Indeed, it appears to us that the only plausible path for sustainable growth is an economic stimulus driven by a devalued U.S. dollar. However, U.S. trading partners, including Japan, China, and Europe, are trying to do the same with their currencies. We suspect that Donald Trump, behind the scenes, will be seeking trade agreements that limit the role of the U.S. dollar as the world’s reserve currency, thereby reducing worldwide demand for U.S. dollars.

- Profit Margin Pressure

Beyond the impact of a strong dollar, other sources of profit margin pressure include higher interest rates and increased labor costs, possibly mitigated by Trump’s plan to cut corporate tax rates. Companies that choose to move their manufacturing operations back to the United States might create additional domestic jobs, but increased labor costs should reduce corporate profit margins. While Congress may reduce the corporate tax rate, we expect any tax rate reductions will be offset with fewer tax loopholes, resulting in an effective corporate tax rate that might not be significantly different in the aggregate from what U.S. corporations pay today.

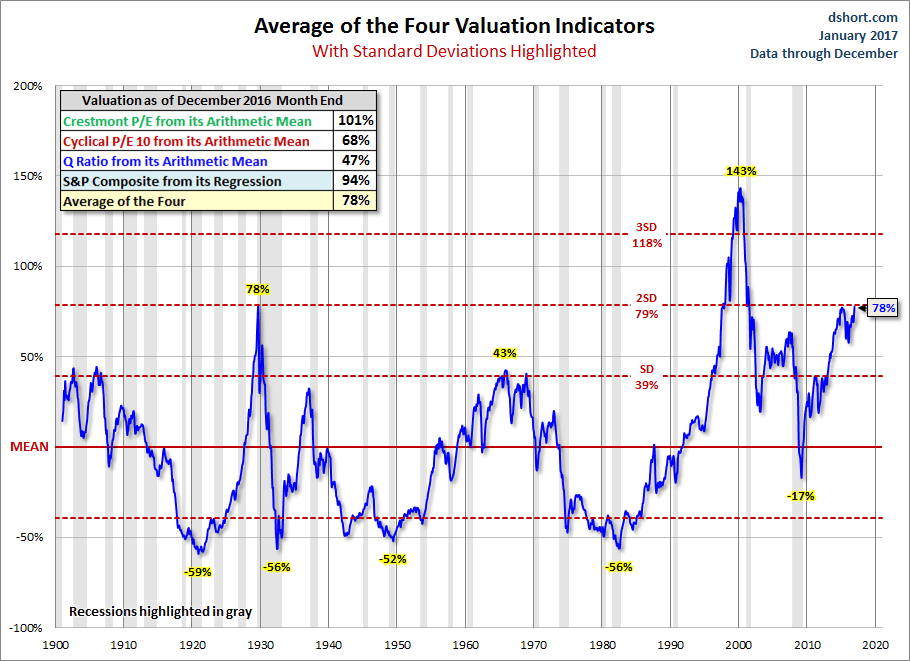

- U.S. Stocks are Historically Expensive

The chart below depicts the simple average long-term valuation history of the S&P 500 using four different, but widely used, valuation techniques. Regardless of the measure used, U.S. stocks appear expensive on an absolute basis and relative to history; in the chart below, the only two times that the S&P 500 Index was more expensive than the present time over the last century occurred in 1929 and in the period between 1998 and 2000. Passively investing in the S&P 500 Index during those two periods generated a poor investment return during the decade that followed, to say the least. While the U.S. stock market could become more expensive in the short-term than it is currently, we believe prudence and selectivity are currently warranted with regards to U.S. stocks.

- Trade Wars Loom

Even before Trump was elected, global trade had been declining, driven by a slowdown in China, by lower commodity prices, and by lower oil prices. Trump appears serious about pursuing a more protectionist trade policy to strengthen the domestic job market and reduce the U.S. trade deficit. Increased global trade has been an enormous tailwind to the global economy over the past 30 years; it is difficult to imagine how a decline in global trade going forward would not represent an enormous headwind for the global economy and a significant source of geopolitical and economic risk.

Despite the short-term revival of investors’ animal spirits since the election, we would suggest that long-term investors ignore the noise of the short-term market rally and pay closer attention to the long-term fundamentals which will have a more important influence on long-term investment returns. U.S. stock market valuations are elevated, while interest rates are historically low. High levels of debt continue to create a burden on many sectors of the global economy, and an increase in interest rates have only worsened this burden. Global trade has been declining, and there is the risk that developed counties either back away from globalization or inadvertently stumble into a trade war. We expect that idiosyncratic investment opportunities will continue to surface; nevertheless, now is a time to maintain investment discipline, in our view.

Renowned value investor, Benjamin Graham, once said that, “In the short run, the market is a voting machine but, in the long run, it is a weighing machine.” Truer words have never been spoken. After U.S. voters finished voting at the ballot box, investors have been voting with their capital, driving up already-expensive U.S. share prices, at least for now. In the long-term, we expect the factors described in this letter will likely weigh on U.S. equities, resulting in sub-par broad stock market returns over the intermediate period ahead.

During the recent market upturn, we have generally been trimming U.S. equity positions and selling U.S. stocks that have appreciated above our estimates of intrinsic value. Should U.S. stocks continue to rise, we expect to take advantage of additional selling opportunities and park the proceeds in cash or short-term bonds. While attractive investment opportunities in U.S. stocks currently appear to be few and far between, foreign stock valuations are generally more attractive. We are busy researching companies and preparing a shopping list for both foreign and domestic investment opportunities, readying ourselves for the time when the current climate of political and economic uncertainty spreads to the stock market.

With regards to fixed income investments, we think prudence is warranted here as well. Treasury bond yields are moderately more attractive compared to the record low yields reached in the summer of 2016, but corporate credit spreads continue to compress further, which means that corporate bond investors are presently being paid insufficiently for taking on corporate credit risk. Until corporate credit spreads widen, we are buying the fixed income issues of companies with better than average credit quality. As it is with the stock market, and with a nod to Warren Buffet’s famous quote, we believe that now is a time to be more fearful rather than greedy. When Mr. Market inevitably becomes more fearful, we expect to become aggressive buyers once again.

*****

With 2016 behind us and 2017 just beginning, we want to take this opportunity to wish our clients and their families a happy, healthy, and prosperous New Year. We thank you for your long-term commitment to our investment philosophy, our investment approach, and our investment team. We are only able to make the strategic decisions discussed in this letter because we have clients, like you, with patience and a long-term outlook. This support allows us to act and invest with prudence and discipline during markets that can sometimes be difficult to comprehend.

Sincerely,

Pekin Hardy Strauss Wealth Management

This commentary is prepared by Pekin Hardy Strauss, Inc. (dba “Pekin Hardy Strauss Wealth Management”, “Pekin Hardy”) for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any security. The information contained herein is neither investment advice nor a legal opinion. The views expressed are those of the authors as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. Pekin Hardy Strauss Inc. cannot assure that the type of investments discussed herein will outperform any other investment strategy in the future. Although information has been obtained from and is based upon sources Pekin Hardy believes to be reliable, we do not guarantee their accuracy. There are no assurances that any predicted results will actually occur. Past performance is no guarantee of future results. The S&P 500 Index measures an index of 500 stocks chosen for market size, liquidity and industry grouping, among other factors.