Photo by Georgios Kollidas

“The four most expensive words in the English language are

‘this time it’s different.’”

– Sir John Templeton, Investor

It’s different this time, and it’s also not different this time.

It’s different this time because the credit-driven U.S. economy is burdened with a monumental level of financial obligations relative to GDP. According to the Bank of International Settlements (BIS), outstanding loans and debts that burden U.S. corporations, households, and government entities have reached $48.3 trillion or 250% of U.S. GDP. Including off-balance sheet items, the effective level of debt outstanding is almost $100 trillion or more than 500% of GDP. It’s different this time because the U.S. economy has never in its history piled on so many financial obligations.

With that said, it’s also not at all different this time, because this is not the first time that a society’s financial obligations have grown to unsustainable levels. This story has been repeated often through history, and it usually ends poorly. The downside risk today for investors is captured in Charles Bullock’s account of Dionysus of Syracuse, from more than 2000 years ago.

Having borrowed money from citizens of Syracuse and being pressed for repayment, he [Dionysus] ordered all the coin in the city to be brought to him, under penalty of death. After taking up the collection, he re-stamped the coins, giving to each drachma the value of two drachmae, so that he was enabled to pay back both the original loan and the money he had ordered brought to the mint.

Displaying a level of creativity that could compete with today’s central bankers, Dionysus defaulted on his debts by debasing the currency, to the detriment of Syracusans who held their savings in drachmae. When a debt obligation becomes too big to repay, it is no longer a problem for the debtor; it becomes a problem for the creditor. The warning caveat emptor, which translates to “buyer beware,” remains timeless because “this time” is hardly ever different.

$100 Trillion of Financial Obligations

Let’s review the U.S. economy’s financial obligations one-by-one to better understand what makes up the $100 trillion of financial obligations of U.S. consumers, households, and government entities:

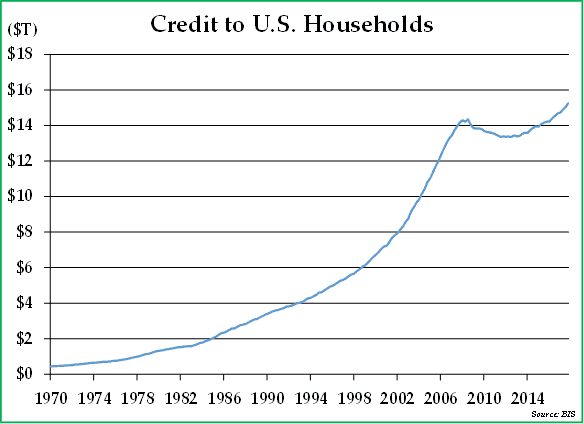

- Credit to households ($15.25 trillion or 79.7% of GDP): S. household debt includes $10.1 trillion of mortgage debt, $1.5 trillion of student debt, $1.1 trillion of auto loan debt, and $0.8 trillion of credit card debt. While still very high, the level of household debt relative to GDP has declined slightly over the past ten years due to the many mortgage-related defaults that have occurred since the financial crisis. Nevertheless, household debt has increased dramatically at a rate of over 7.1% per annum over the past forty years as household income has simply not kept pace with increases in living expenses for most Americans, particularly with regards to healthcare, housing, and education expenses.

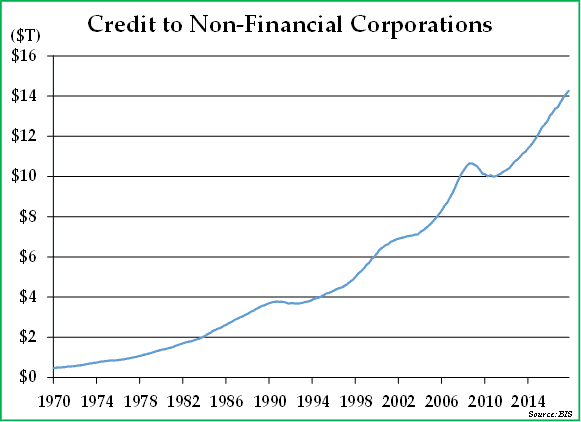

- Credit to non-financial corporations ($14.26 trillion or 73.5% of GDP): Corporate debt stands at a record level and continues to grow, driven by corporate buybacks and the growth of leveraged buyouts. Record issuance of corporate bonds and leveraged loans in recent years has boosted the share prices of both public and private companies, driving outsized compensation increases for management teams and private equity firms through financial engineering.

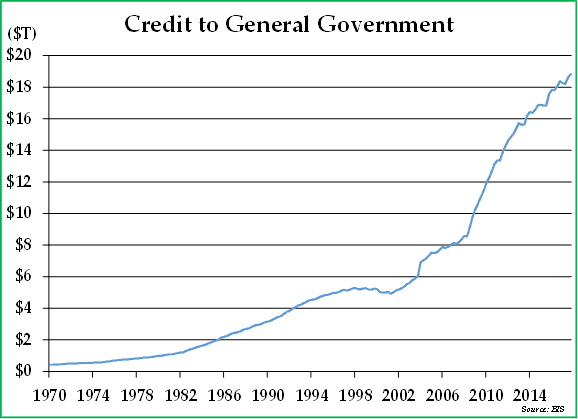

- Government debt ($18.81 trillion or 97.0% of U.S. GDP): Government debt includes $3.1 trillion owed by various state and local governments along with $15.4 trillion owed to the public by the Federal government. These debts are also at record levels and continue to grow at a faster rate than GDP, driven by demographics, military spending, deficits generated during the Financial Crisis, and a persistent mismatch between tax revenues and spending levels. Unfortunately, Congress and the Trump administration further impaired the Federal government’s financial strength by passing the Tax Cuts and Jobs Act (TCJA) of 2017, which is projected to increase future U.S. government deficits by almost $1.5 trillion per annum over the next decade and by approximately $1.0 trillion per annum thereafter.

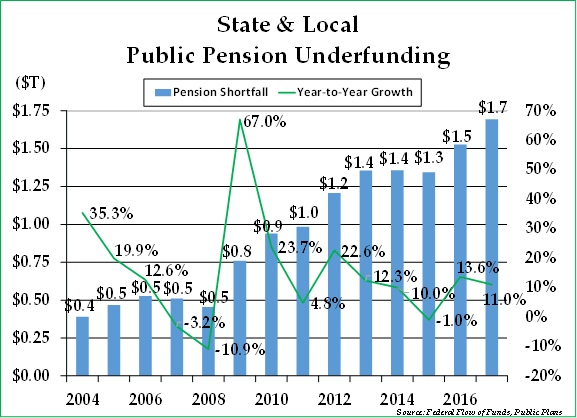

- Pension underfunding ($2.25 trillion or 11.6% of GDP): While not officially tallied on anyone’s balance sheet, pension plans are woefully underfunded and represent an enormous off-balance sheet liability for cities like Chicago, states like Illinois, and multi-employer pensions. According to the Center for Retirement Research at Boston College, state and local pension plans are only 72% funded today, representing a total shortfall of $1.7 trillion. Surprisingly, these unfunded obligations have more than doubled since 2009 despite a strong bull market in the prices of all kinds of financial assets, from stocks to bonds to private equity investments. Meanwhile, multi-employer pension plans are only 46.4% funded, with a corresponding unfunded liability of $500 billion.

- Social insurance obligations ($49.0 trillion or 253% of GDP): Every day, 10,000 baby boomers retire and begin collecting Social Security and Medicare benefits for the first time. As the retiree to worker ratio increases, demographic challenges will increasingly put pressure on the Federal budget. According to U.S. General Accountability Office (GAO) estimates, the net present value of the Federal government’s Social Security obligations is $15.4 trillion, or 79.4% of GDP, while the net present value of Medicare obligations is $33.5 trillion, or 172.8% of GDP. Because most of these obligations represent benefits to the elderly, these costs are driven by demographics and runaway healthcare price inflation.

Why These Obligations Are Problematic

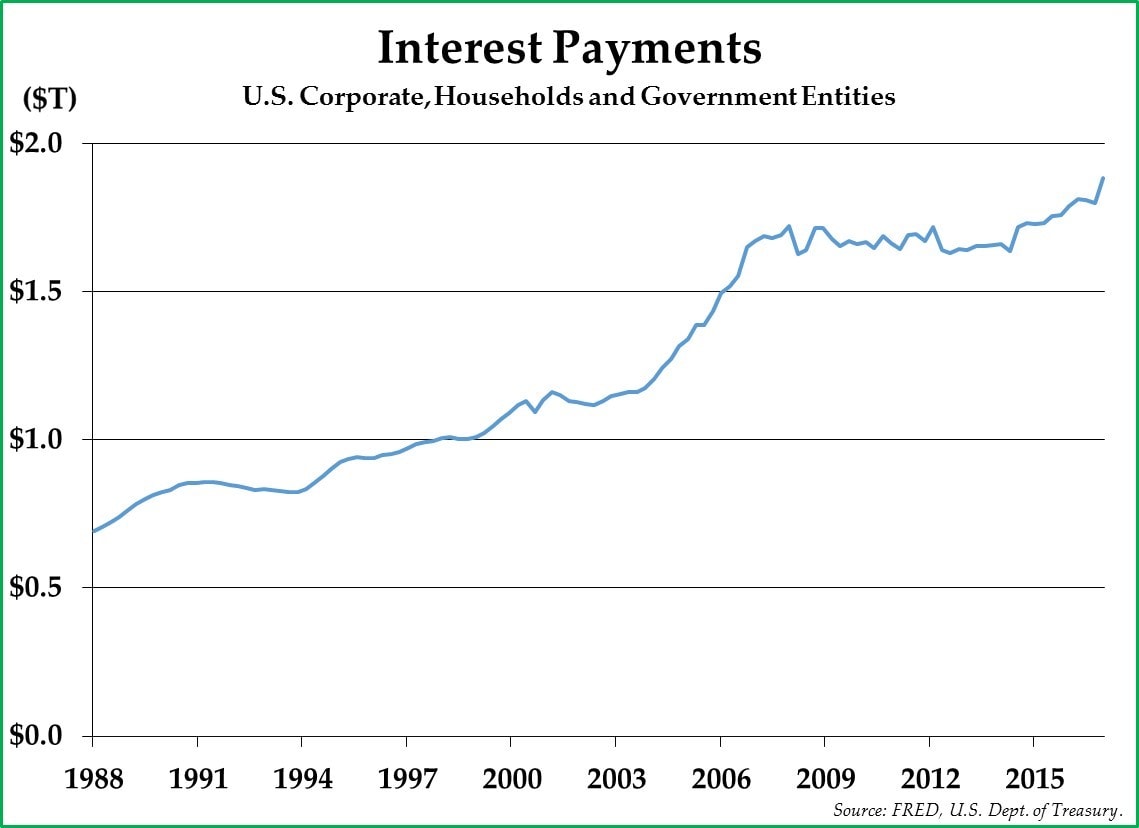

As debts have increased and as interest rates have begun increasing, interest payments for U.S. corporations, households, and government entities are now almost $2 trillion annually. Even without the Federal Reserve raising interest rates further from current levels, interest payments should exceed 10% of GDP in 2018. If interest rates were to rise to levels close to the historical average, interest rate payments would devastate the U.S. economy and likely result in another debt crisis. These payments prevent households from saving money for a rainy day, corporations from investing in new factories, and governmental entities from investing in basic infrastructure.

Policy Implications

Thus far our discussion has centered on the U.S. economy, but the excessive financial obligations are widespread across the world. The Financial Crisis was, after all, a global crisis, affecting large multi-national banks across the world, and other countries’ challenges are similar to or even worse than that of the United States. For example, while the combined private and public debt/GDP ratio is 252% in the United States, countries like the United Kingdom, China, Japan, and Canada have ratios of 283%, 256%, 373%, and 289%, respectively.[1] Put simply, many of the largest economies across the world are seemingly drowning in excessive financial obligations.

These financial obligations are deflationary and make the global financial system more fragile. If the world were to enter a deep recession and global GDP were to decline by 5%, the debt ratios listed above would materially increase. As corporations, consumers, and perhaps even some governments defaulted on their debts, global GDP would likely decline further, creating a vicious cycle which economist John Maynard Keynes famously described as a liquidity trap, whereby everyone just wants to own cash. During the Great Depression, many banks failed because cash was no longer available for depositors to withdraw.

To prevent a liquidity trap, central banks around the world have been providing unprecedented levels of monetary stimulus to keep the global economy from deflating. Such stimulus has taken various forms, but the two primary forms thus far have been 1) zero percent or negative interest rates and 2) quantitative easing, whereby central banks increase the money supply by printing money to buy securities. In the United States, the Federal Reserve has purchased U.S. Treasuries, while other central banks like the Bank of Japan have been purchasing equity ETFs.

For advanced economies like the United States, Europe, and Japan, policymakers are likely to continue a set of policies known as financial repression until debt/GDP ratios decline to historically normal levels. Financial repression was also the playbook of advanced economy policymakers after World War II when the debt/GDP ratio in the United States was also high. Dr. Carmen Reinhart, who literally wrote the book about debt crises and financial repression (ironically titled This Time is Different) suggests that most advanced economy countries pursue financial repression when addressing excessive domestic debt. Financially repressive policy includes the following:

- Maintaining negative real interest rates: Keeping real (e., inflation-adjusted) interest rates persistently negative over several decades is the cornerstone of financial repression. This opaque tax on fixed income investors makes it easier for GDP to grow faster than public debt, thereby reducing the debt/GDP ratio.[1] Alternatively, a surprise burst of inflation accomplishes the same goal, but in a shorter timeframe.

- Herding domestic investors into public debt: Laws and regulations that force or coax investors into owning more public debt represent the other critical component of financial repression. For example, the money market funds we have selected for clients own 100% U.S. Treasuries because, as of October 2016, other types of money market funds became eligible to “break the buck” should bond prices decline. This regulation alone has thus far resulted in $1 trillion dollars of additional domestic capital that now own U.S. government debt.

So far, these policies have not worked as successfully as they did after World War II because the debt/GDP ratio has only continued to increase since the Financial Crisis. We suspect the efficacy of financial repression in the current era is somewhat hampered by demographic challenges. In addition, more recently, Congress and the Trump administration have enacted revenue cuts along with budget increases which should further increase the budget deficit and government debt.

While interest rates have risen recently, so too has inflation. Between the increased fiscal stimulus and the possibility that the United States may no longer want to export its dollars in return for imported goods, the likelihood of a surprise burst of elevated inflation seems to be increasing, in our view.

Investment Implications

In a financially repressive interest rate and regulatory regime, a significant wealth transfer from creditors to debtors can occur over a generation or longer. If you are making long-term financial plans, we suggest taking several considerations into account.

- You should stay on top of tax policy and tax policy changes in order to minimize your tax liabilities. We try to help you with this by sharing with you our Navigator reports, where we are increasingly trying to focus on tax minimization strategies.

- Due to underfunded state and local pensions, you should expect that state and local taxes on income, sales, and property will continue increasing at an elevated rate.

- Given the protracted negative interest rate environment, it will be more important than ever to maintain a high savings rate to grow your assets over time.

At the present moment, interest rates and inflation are rising, U.S. stocks are generally expensive, geopolitical risks are increasing, and the economy, while firing on all cylinders, has been expanding for nearly a decade. Given this backdrop, taking asset allocation measures that err on the side of prudence and defensiveness seems appropriate.

Set forth below are our thoughts on the relative attractiveness of various investment options:

- Deposits and CDs: Unattractive

Bank deposits and bank CDs generally earn a lower return than the inflation rate, but they also earn a lower return than what is available today from short-term U.S. Treasuries and short-term corporate bonds. While maintaining a certain amount of cash is prudent, we would not recommend holding an outsized position, given the alternatives available.

- Short-term bonds: Attractive (as a money market substitute)

With the Federal Reserve raising interest rates, two-year U.S. Treasuries are providing a nominal yield of 2.59%. While still generating a negative inflation-adjusted interest rate, such bonds provide a more attractive return than most bank deposits or CDs. Some short-term corporate bonds offer a positive real interest rate, but they have a bit more credit risk; for that reason, selectivity matters. Most importantly, if inflation accelerates and interest rates spike, the price impact on short-term bonds will be muted relative to long-term bonds.

- Long-term Treasury bonds: Unattractive

Although the interest rate on long-term Treasury bonds has increased in recent months, so too has the inflation rate and forward inflation expectations. If inflation grinds on for years at a rate slightly above the long-term interest rate or if an inflation surprise arrives (which is more likely than not) long-term bonds will generate a negative real return. If interest rates rise significantly as inflation accelerates, long-term bonds could generate a significantly negative nominal return.

- S. Equity Index Funds and ETFs: Unattractive

U.S. index funds and ETFs have outperformed almost every other asset class over the past ten years, just as they did during the 1990s. Importantly, two-year U.S. Treasuries now provide a better income yield at 2.63% than the 1.9% dividend yield of the S&P 500 Index. On almost every possible valuation measure, the U.S. stock market trades at a level which is well above historical averages and which is greater than almost any other period of history except for the peak of the Dot-Com bubble in 2000.

- Selected value stocks: Attractive

The key to generating attractive long-term investment returns is purchasing assets when they are cheap and then selling those assets when they are dear. Just as bargains could be found at the peak of the Dot-Com bubble, we believe bargains can be found today, despite the high valuation of the overall U.S. stock market, but it requires taking an active approach, buying stocks that are not held widely in the largest ETFs, and steering clear of being exposed to the most wildly overvalued sectors of the U.S. stock market. If inflation accelerates, valuation ratios (such as the P/E ratio) should compress, but likely more so for those companies that trade at an expensive P/E ratio than for those companies that trade at a discounted P/E ratio.

- Foreign stocks: Attractive

Equities outside the United States are generally more attractively valued than U.S. stocks, and emerging market stocks are also attractively valued at the present moment, in our view. We are continuing to look for and find interesting investment ideas in foreign markets which should diversify your portfolio geographically. If a U.S.-centric inflation surprise happens, foreign stocks with profits denominated in a foreign currency should perform well.

- Precious metals (g., gold): Attractive

Historically, gold has generated better returns than bonds in negative real interest rate environments. Given how expensive the stock market currently is, we would further suggest that gold is likely to generate better returns over the next decade than the S&P 500 Index. Due to concerns about the U.S. fiscal situation, foreign central banks have stopped accumulating U.S. Treasuries, but they continue to accumulate gold. Besides being a good insurance policy, gold should perform well in an environment where inflation is likely to increase and interest rates are not likely to keep pace with inflation.

- Real estate: Depends

Real estate is generally an attractive asset class under financial repression. If you purchase an attractively-priced property, you should be able to increase rents with inflation. Furthermore, if you finance your investment with a low-cost mortgage, your returns are likely to be enhanced by the negative real interest rate environment.

In summary, due to the financialized U.S. economy and where we are in the market cycle, we are pursuing an investment approach of defensiveness along with an emphasis on return of capital above return on capital, diversifying investments across asset classes, and protecting the real value of your portfolio against a negative real interest rate environment. The time will come again to invest more aggressively, but that time is not now.

Pekin Hardy Strauss Wealth Management

This commentary is prepared by Pekin Hardy Strauss, Inc. (“Pekin Hardy”) for informational purposes only. Pekin Hardy Strauss, Inc. does business as Pekin Hardy Strauss Wealth Management, encompassing financial planning and separate account management services for individuals and families, and as Appleseed Capital, the firm’s institutionally-focused arm. The information contained herein is neither investment advice nor a legal opinion. The views expressed are those of the authors as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. Although information has been obtained from and is based upon sources Pekin Hardy believes to be reliable, we do not guarantee its accuracy. There are no assurances that any predicted results will actually occur. Past performance is no guarantee of future results. The S&P 500 Index measures an index of 500 stocks chosen for market size, liquidity and industry grouping, among other factors.