Photo by JackF

“Things fall apart; the centre cannot hold;

Mere anarchy is loosed upon the world,

The blood-dimmed tide is loosed, and everywhere

The ceremony of innocence is drowned;

The best lack all conviction, while the worst

Are full of passionate intensity.”

− W.B. Yeats, “The Second Coming”

Slowly but surely, the world has been moving from compromise and coordination to name-calling and tribalism. We read news of impeachment inquiries, trade wars, mass demonstrations, accusations of treason, worsening geopolitical tensions, conspiracy theories, fake news, and Twitter curses, sometimes all in the same day. The current period will likely be studied closely by historians trying to make sense of the many seemingly irreconcilable conflicts that have surfaced.

Rising areas of contention include, but are not limited to: the United States vs. China, the rich vs. the poor, the old vs. the young, capitalists vs. socialists, Democrats vs. Republicans, and globalists vs. nationalists. Many of these conflicts seem irreconcilable, which means that a risk exists that some conflicts could be fought until won or lost rather than negotiated through compromise. The ongoing news about these conflicts creates uncertainty and stress for all concerned citizens.

As investors, we do not yet know how these conflicts will get resolved. Just as it would have been impossible to predict the drone attack that took place in September against Saudi Arabia, crippling approximately 50% of its oil processing capacity, it would be folly for us to make concrete predictions about political outcomes. Nevertheless, we have no choice but to express an opinion about probable outcomes through the investment decisions we make on behalf of our clients.

In this regard, we thought it would be useful to focus on a few areas of particular friction and discuss their likely economic and financial implications.

Global Geopolitical Uncertainty

Two phenomena have driven the increased friction between the United States and China. First, as China’s economic and military strength has grown, China is increasingly able to challenge the global hegemony of the United States from economic, military, cultural, and monetary standpoints. Second, ever since China joined the World Trade Organization in 2002, U.S. manufacturing job losses accelerated as U.S. companies built new production capacity in China while closing down domestic manufacturing facilities, which has exacerbated rising economic inequality within the United States.

While President Trump and Chairman Xi negotiate the terms of the U.S./China bilateral relationship, the uncertainty is unsettling for financial markets. President Trump often tries to buoy the stock market with hopeful tweets about trade discussions, except for when he scares the stock market with defiant tweets that stoke geopolitical tensions. As time passes, it grows more likely that the United States and China could enter a new cold war. In a worst-case scenario, we would expect to see a bifurcation of supply chains, payment systems, technology infrastructure, financial markets, and even the Internet. In a best-case scenario, we would expect a bilateral agreement between the United States and China that allows for limited trade and places additional restrictions on currency manipulation.

With regard to the Middle East, the United States is trying to withdraw from its role as a regional peacekeeper. As we write this letter, President Trump has announced his intent to withdraw from Syria. The drone attack on Saudi Arabia’s processing facilities probably took advantage of the Trump administration’s communicated lack of appetite for engaging in new regional conflicts in the Middle East. With less interest and ability to project power in the region, the U.S. will allow other countries like Russia, China, and Iran to fill the void.

The international monetary system, too, is in the middle of a transition as a unipolar monetary system centered around the U.S. dollar becomes increasingly multipolar. Since the Financial Crisis, perhaps in anticipation of current geopolitical shifts, foreign central banks have been turning away from the U.S. dollar as a hard currency reserve and turning towards gold. The United States has attempted to combat these efforts through economic sanctions, but sanctions are causing many countries to become even more eager to reduce their reliance on a U.S. dollar-centric monetary system.

With the United States withdrawing or reducing its military presence in the Middle East, the role of the U.S. dollar as the currency of choice in oil markets will inevitably diminish. China, which has become the largest importer of Middle East oil, should find it increasingly easier to buy oil without using U.S. dollars to do so. For example, in September, Petroleum Economist reported the terms of a strategic partnership between China and Iran whereby China would provide Iran with $400 billion of direct investment and 5,000 Chinese security personnel in return for Iran’s agreement to accept non-dollar currencies for its oil, including the Chinese renminbi. This development, and others like it, will inevitably reduce long-term global demand for U.S. dollars.

As the world shifts from a unipolar one with the United States as the world’s policeman and reserve currency issuer to a multipolar one, it should inevitably mean higher trade barriers, less globalization, less foreign hoarding of U.S. dollars, more support for gold as an international reserve, and fewer military commitments overseas for the United States.

Domestic Political Uncertainty

Over the past 30 years, with increased globalization, low inflation, and declining interest rates, U.S. investors have benefited greatly from increasing corporate profit margins and strong financial returns. At the same time, while wage gains have been robust for the upper 10% of the income distribution and especially for the upper 1% and above, wages for the bottom 90% of the income distribution have remained stagnant. As a result, income and wealth inequality has reached extreme levels not seen since the early 1930s, resulting in social discontent, class conflict, and the rise of populist politicians like Donald Trump on the Republican side and Bernie Sanders, Elizabeth Warren, and Andrew Yang on the Democrat side.

When considering the theme of economic inequality, we are reminded of historian Will Durant’s warning that an “unstable equilibrium generates a critical situation, which history has diversely met by legislation redistributing wealth or by revolution distributing poverty.” Current prescriptions that propose to address economic inequality vary. Some propose devaluing the dollar (e.g., Warren, Trump), thereby reducing the real value of debt obligations. Others propose wiping away debts, such as college loans (e.g., Warren, Sanders). Meanwhile, several want to use tax and fiscal policy to redistribute wealth explicitly (e.g., Yang, Sanders, Warren).

Regardless of the outcome of the 2020 election, whoever becomes president will likely face a starkly divided nation, enjoying wild popularity among one-half the electorate while being despised by the other half.

For investors, however, it may be the similarities between President Trump’s plans and various Democrat plans that are worth noting. President Trump has made it abundantly clear that he has no intention to lower the Federal deficit. If anything, he would be eager to sign a bill that increases spending to invest in infrastructure or further reduce tax rates. While Democratic candidates are calling for increased taxes, the taxes planned would hardly pay for proposed new spending. The top presidential candidates seem to all agree that keeping the Federal deficit under control is no longer a policy priority.

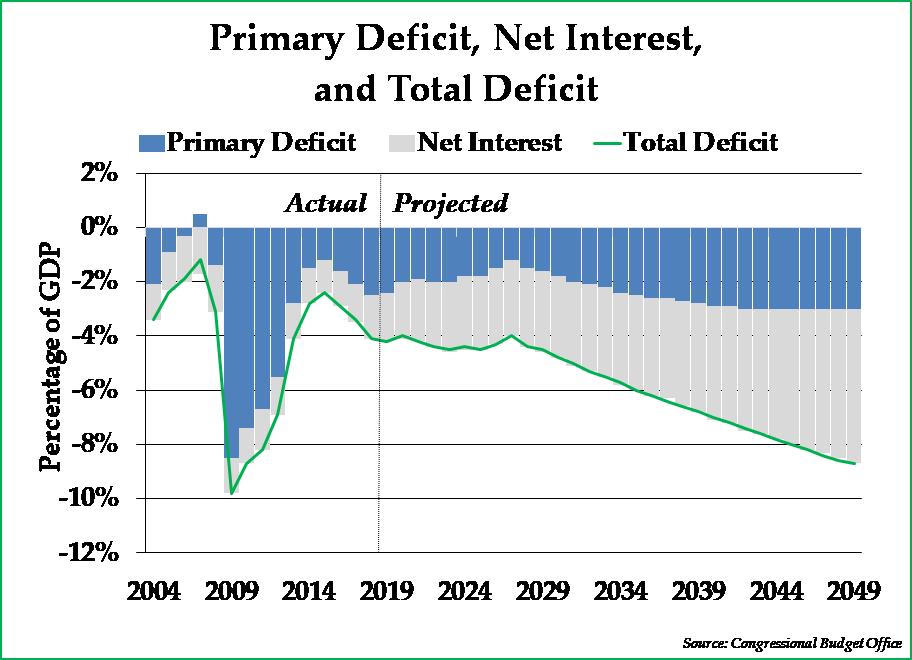

During the three consecutive years between 2016 and 2018, the budget deficit has expanded without a recession for the first time in U.S. history and is currently running at approximately 4% of GDP (see chart below). Based on current Congressional Budget Office projections, it is difficult to see anything that would get in the way of growing deficits during the next several decades, even without any policy changes. The policy proposals of President Trump and most Democratic presidential candidates would worsen an already poor budget outlook.

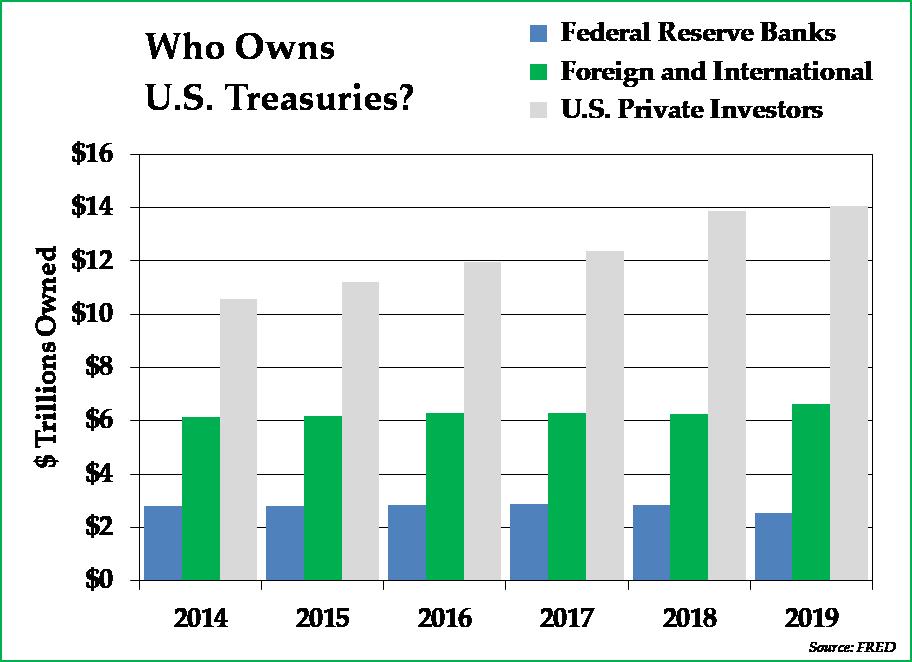

An increasing deficit is concerning enough, but the situation is made worse by the fact that the U.S. Treasury is starting to have increasing difficulties in financing these deficits. Since 2014, U.S. private investors, especially U.S. primary dealers such as JPMorgan Chase, have absorbed most of the additional supply of U.S. Treasuries (see chart below). However, these primary dealers have little room to expand their balance sheet further to buy U.S. Treasuries, which is why the Federal Reserve will have to become an increasingly significant source of government funding.

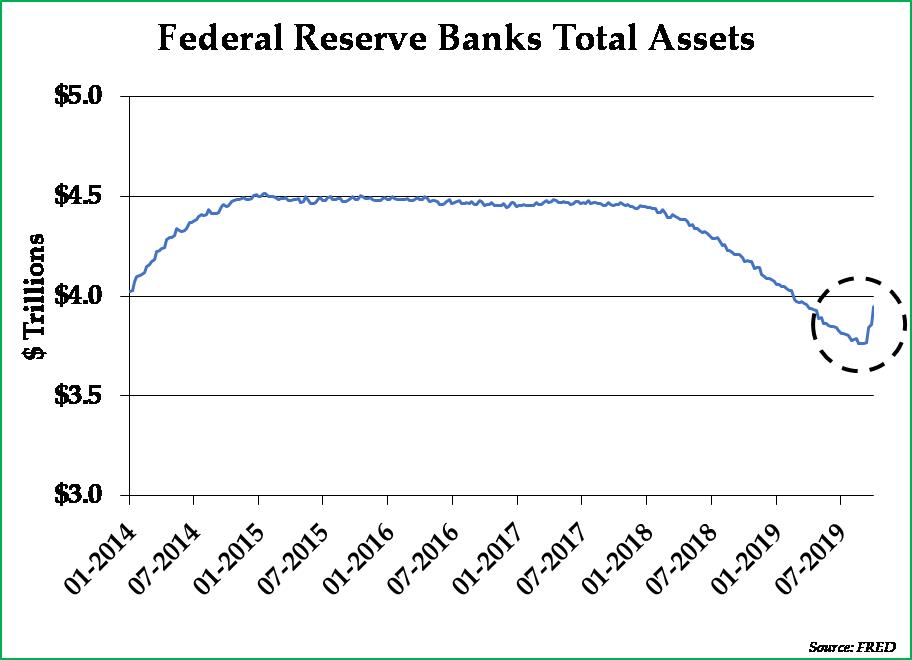

Indeed, in recent weeks, the Federal Reserve has begun to increase the size of its balance sheet again by purchasing U.S. Treasury bills to ensure that the Federal government remains funded (see chart below). While denying any kinship to the quantitative easing measures that took place earlier this decade, the Federal Reserve has resumed these purchases while the only visible difference is that its purchases are restricted to short-term Treasuries.

We expect that the Federal Reserve will continue to “inject liquidity” and buy U.S. Treasury bonds as necessary with that liquidity, with no end in sight. Our confidence level is supported by the large supply of Treasury bonds that already has become too large for private investors to absorb and should only increase in the future.

Investment Implications

The ongoing, centrifugal transition towards a multipolar geopolitical environment and a more populist but divided political environment should have important repercussions on the economy and financial markets. For the United States, a less globalized economy and increasing fiscal deficits monetized by the Federal Reserve are likely to result in higher wages, lower corporate profit margins due to increased labor costs, accelerating cost-push inflation, reduced capital inflows, a lower exchange rate for the U.S. dollar, and a renewed policy focus on domestic manufacturing production.

Inflation’s acceleration has already begun, albeit quietly, due to a combination of increased tariffs, reduced immigration, and minimum wage increases, despite the dollar remaining strong up until this point. The consumer price index (CPI) is currently at a ten-year high. Further acceleration of inflation, while harmful to consumers and especially so to retirees, would make it easier for the U.S. government to reduce the real debt burdens of the Federal government, U.S. corporations, and U.S. households alike.

With a weakening dollar, we would expect foreign stock markets, commodities, and gold to outperform. On the other hand, those companies which have benefited greatly from globalization trends, such as Apple and Boeing, will probably have a difficult time maintaining current profit margins. Stocks that are expensive and trade at elevated P/E ratios should also have a difficult time performing well, as P/E ratios tend to contract when inflation expectations increase. We are still buying selected U.S. stocks for clients, but they are generally not the stocks of companies that have benefited so much from the globalization trend of the past 30 years, and they are generally stocks that already have low P/E ratios.

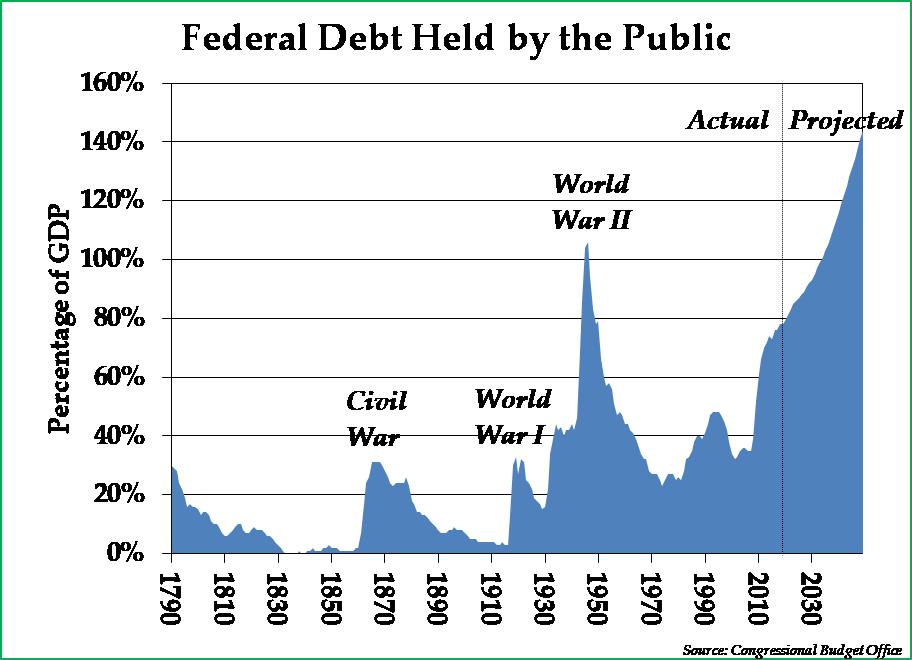

Despite inflation accelerating, we would expect interest rates to remain low, thanks to U.S. Treasury purchases by the Federal Reserve that would cap interest rates and provide funding for increasing budget deficits. This has happened before, in the years following World War II, when the United States also had a large debt load relative to GDP (see chart below). Because inflation could very well remain at a level above that of long-term interest rates, long-term bonds remain unattractive investments.

In periods of history where it sometimes feels like everything might be falling apart, such as the one we are all currently living through, trust comes at a premium. Our primary goal is to act as a trusted steward for our clients in managing their assets, during good times and especially during challenging times. We thank you once again for your ongoing trust.

Please do not hesitate to reach out to us with any questions.

Sincerely,

Pekin Hardy Strauss Wealth Management

This commentary is prepared by Pekin Hardy Strauss, Inc. (dba Pekin Hardy Strauss Wealth Management, “Pekin Hardy”) for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any security. The information contained herein is neither investment advice nor a legal opinion. The views expressed are those of the authors as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. Although information has been obtained from and is based upon sources Pekin Hardy believes to be reliable, we do not guarantee its accuracy. There are no assurances that any predicted results will actually occur. Past performance is no guarantee of future results. The Consumer Price Index (CPI) is an unmanaged index representing the rate of the inflation of U.S. consumer prices as determined by the U.S. Department of Labor Statistics.