Photo by zimmytws

Variable annuities are highly complex financial instruments that, despite their popularity, appear to be unsuitable for most investors. While these vehicles offer various theoretical guarantees that may appear attractive to certain investors, the exorbitant costs, poor liquidity, and potentially low returns offered by variable annuities raise questions about their appropriateness for many investors. In this Navigator, we will explain how variable annuities work and review the arguments both for and, more importantly in our estimation, against owning such instruments.

Variable Annuities

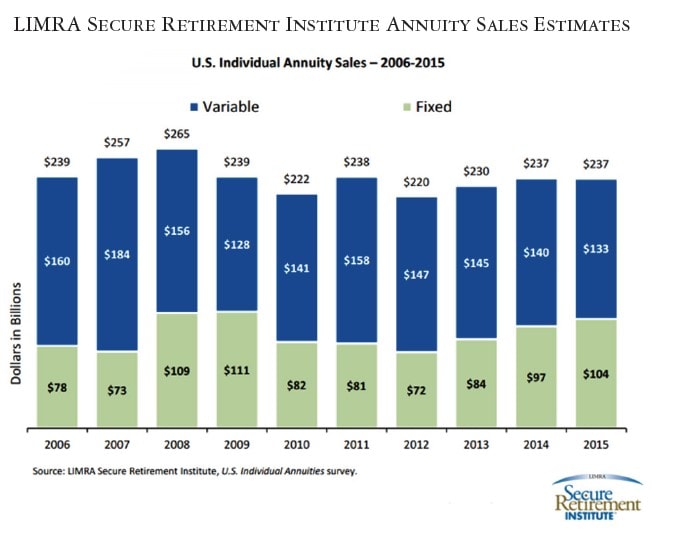

Variable annuities are among the most popular products in the financial services industry, with total sales of approximately $133 billion in 2015.1 These products have long played a role in many investors’ retirement strategies; ironically, despite their widespread use, variable annuities are simultaneously among the most maligned financial products currently available. There is no shortage of insurance brokers ready to praise variable annuities, while there are just as many financial professionals and journalists who stand ready and willing to speak about the ills of variable annuity products. Our goal in this Navigator is to explain the product in simple terms and sort out the pros and cons.

A myriad of annuity structures are sold today, with fixed and variable annuities being the most popular. A fixed annuity is a relatively simple product that consists of a contract between an individual and an insurance provider; the insurer agrees to make fixed payments to the individual, either immediately or at some point in the future, in exchange for a single lump sum payment or a series of payments.2 A variable annuity, however, is a far more complex creature. With a nearly endless menu of options and riders, any two variable annuity contracts are rarely identical. To simplify the discussion, we want to focus our analysis on the basic variable annuity structure and function with the caveat that our description will most certainly not be applicable to all variable annuity contracts.

As the below chart of annuity sales indicates, variable annuity sales have consistently outpaced fixed annuity sales in the United States over the past 10 years. As we will show throughout this article, it seems that this is more a result of questionable sales tactics and insufficient consumer knowledge than the actual suitability of variable annuity products for most investors.

The Basics of Variable Annuities

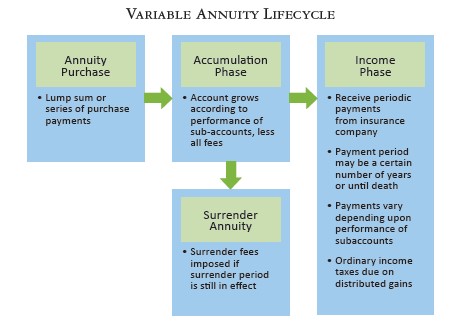

At the most basic level, a variable annuity is essentially a mutual fund or collection of mutual funds, with an insurance contract wrapper. Just as with a fixed annuity, the owner of a variable annuity pays an insurance company a lump sum or series of payments in exchange for the promise of a series of future payments in return, either immediately or at some point in the future. While a fixed annuity grows at a guaranteed, constant rate, a variable annuity grows at a variable rate that depends upon the performance of the underlying investments, called sub-accounts.

During the accumulation phase of an annuity contract, a variable annuity owner contributes money to his or her annuity, and that money is used to purchase “accumulation units” in the insurance company’s separate account. The separate account purchases shares in various sub-accounts, which are managed portfolios of stock and bond mutual funds. These sub-accounts allow annuity owners to participate, to a certain extent, in the performance of various markets. Many annuities also have a fixed interest rate option in which the insurance company “guarantees” a certain minimum annual interest rate.3 Typically, variable annuity owners can reallocate funds among the available investment options, though such asset re-allocations may be subject to a transfer fee. During the accumulation phase, assets invested in variable annuity sub-accounts grow on a tax-deferred basis and are taxed only when the contract owner withdraws those earnings from the account.

After the accumulation phase comes the income phase. Over time, variable annuity assets should theoretically increase in value to the point at which the contract owner decides he or she would like to begin withdrawing money from the account. The income phase begins when the contract owner decides to “annuitize” the account, meaning that he or she will begin to receive regular payments from the insurance company. The size of payments depends on the contract value, the future performance of the underlying sub-accounts, and the duration over which the contract owner wishes to receive payments. Therefore, unlike with a fixed annuity where future payments are pre-determined, variable annuity payments are subject to variability.

Positive Aspects of Variable Annuities

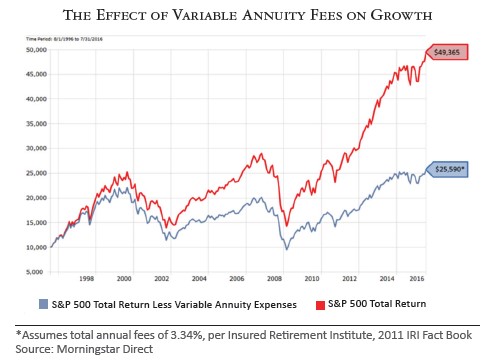

An individual might purchase a variable annuity for several reasons, but the most frequently cited reason is the theoretical guarantee against loss of principal. As described already, most variable annuity contracts have some form of guarantee that limits or eliminates the losses that a contract holder might otherwise experience in down markets. The risk of an extended period of poor investment returns causes many investors to allocate a portion of their investable assets to variable annuity contracts in order to guarantee some amount of income during retirement, regardless of what happens in the securities markets. However, it is important to note that any guarantees come at a high cost, as variable annuities charge all-in fees of 3-4% of the contract value each year. This can be double or triple what comparable investment accounts or standalone mutual funds charge. To better understand the adverse impact of above-average product fees on investment performance, please see the following chart.

Another characteristic of annuities that many buyers find attractive is the tax treatment of annuity earnings. During the accumulation phase of an annuity contract, all taxes on gains that occur within the annuity are deferred. Only when the contract holder begins to receive payments from the annuity are taxes due on those gains. Therefore, individuals who are in a high tax bracket and who have exhausted all of the other tax-advantaged savings options available to them (e.g., IRAs, 401(k) plans, etc.) may find value in the tax-deferral offered by annuity contracts. However, just as with other tax-advantaged retirement vehicles, withdrawals made from an annuity before the contract owner reaches age 59½ may be subject to Federal and state tax penalties.

The Downside of Variable Annuities

While variable annuities have some characteristics that may make them attractive to certain individuals with unique circumstances, they also carry with them a number of drawbacks that make them, in our view, unsuitable for many investors.

COST

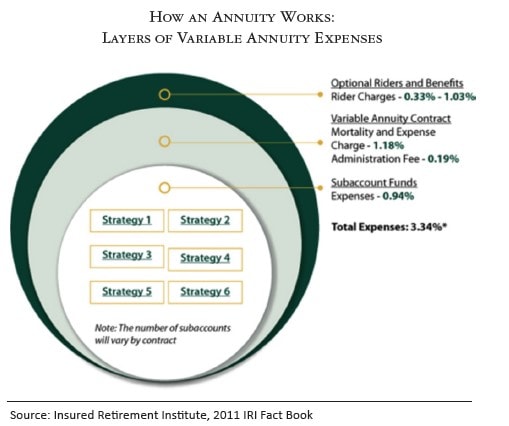

The most significant issue that annuities typically present is high cost. As mentioned earlier annuities have several layers of fees and expenses that can, in aggregate, create a drag of up to 3-4% of the contract’s value each year. A typical annuity can carry many different types of fees, and we have outlined the most common fees below.

- Mortality and expense (“M&E”) risk charge

This expense compensates the insurer for the risk that it assumes under the terms of the contract. Effectively, this is the cost of the “insurance wrapper” that the contract owner purchases as part of the annuity contract. M&E expense charges are calculated as a percentage of the contract value and typically amount to around 1.25-1.50% per year. In many cases, the revenue generated by this charge is used to pay the commission of the broker or agent who sold the annuity. - Administrative fees

Annuity issuers pass on record keeping and other administrative costs to the contract owner. This can be in the form of a flat annual fee or a percentage of the contract value. Administrative fees may be included as part of the M&E risk charge or may be assessed separately. - Fund management expenses

Variable annuities that are invested in mutual fund sub-accounts must also pay management fees charged by the underlying mutual fund managers. These fees can range from 0.2% for passive funds to 1.5% or more for actively managed funds. - Rider charges

Annuity contracts can be customized in a number of ways to serve the specific needs of the contract owner. Some common variable annuity riders include guaranteed minimum accumulation benefit (GMAB), guaranteed minimum withdrawal benefit (GMWB), and guaranteed minimum income benefit (GMIB).4 Riders such as these, as well as most others, typically come with material additional cost. - Surrender charges

A salesperson who sells a variable annuity is typically paid a disproportionately high percentage of the first year’s contract fees in the form of a commission. For that reason, issuers will typically impose stiff penalties on contract owners who decide to terminate their contracts within a certain number of years after their purchase, as the issuers typically make profits after paying their salespeople. Most surrender periods range from six to eight years, although some contracts may impose a surrender charge up to 15 years after the contract is initiated. A typical surrender charge might start at 7% in the first year and then decline by 1% per year until reaching zero, at which point the surrender period would end.

TAX TREATMENT

Somewhat ironically, while favorable tax treatment is often cited as a major reason for purchasing an annuity, variable annuities may actually have some material disadvantages with regards to tax treatment in comparison to many taxable investment accounts.

- Ordinary vs. Capital Gains Tax

As mentioned previously, taxes on any earnings enjoyed by a variable annuity are deferred until those gains are withdrawn, at which time they are taxed as ordinary income. While this could be advantageous for investors who are in a high tax bracket, investors in low or moderate tax brackets may actually end up paying more in taxes upon withdrawal of funds from an annuity than if they had simply paid capital gains taxes on the realized earnings generated by investments in a taxable investment account. While it is true that distributions taken from other tax-deferred accounts such as IRAs and 401(k)s are also taxed at ordinary income rates, in many cases there is a tax deduction for the initial contribution to these types of accounts. Contributions to a variable annuity provide no such tax deduction. - No Cost Basis Adjustment

Variable annuities tend to be highly inefficient vehicles for passing wealth to the next generation because they do not enjoy a cost basis adjustment when the original contract owner dies. When the owner of a taxable investment account passes away, the cost bases of the investments held in the account are adjusted to reflect the market prices of those investments at the time of the owner’s death. In the case of securities that have appreciated in value, this zeroes out any unrealized gains on those investments, along with any associated tax burden that would otherwise fall on the deceased account owner’s heirs. Therefore, heirs can inherit a taxable investment portfolio with a “clean slate” from a tax perspective.Such is not the case with variable annuities. Investments held within a variable annuity do not receive a cost basis adjustment when the original owner of the annuity dies. This means that any accumulated unrealized gains will be passed on to the annuity owner’s heirs, along with the associated tax burden. Even worse, beneficiaries must pay ordinary income tax rates on distributed gains rather than capital gains rates.

CONFLICTS OF INTEREST

One significant issue related to variable annuities is the potential for conflicts of interest that may exist on the part of annuity salespeople. Unlike a financial advisor, who has a fiduciary duty to make investment decisions that benefit the client, an insurance broker has no such fiduciary obligation. Annuity sales are highly lucrative for the insurance professionals who sell them because of high upfront sales commissions. This defining feature is especially true in the case of variable annuity sales, which pay sales commissions of up to more than 10% of the annuity contract’s value. The strong financial incentive for insurance salespeople to push variable annuity products raises questions regarding the suitability of such products for many investors to whom they are sold. Investors who are considering purchasing a variable annuity should fully consider these potential conflicts of interest when determining whether or not such a product makes sense in the context of his or her financial goals.

GROWTH CAPS

While variable annuities are designed to allow investors to participate in the growth of various securities markets, many variable annuities actually limit the degree to which contract holders can enjoy such growth when it occurs. Many variable annuity contracts contain language which places a cap on the percentage of gain that can be experienced by certain sub-accounts. These caps prevent the annuity owner from fully participating in a portion of gains that could otherwise be enjoyed in years in which markets generate substantial returns. From an outsider’s perspective, it would seem that investors are trading a cap on investment returns for the aforementioned guaranteed floor on investment returns.

LACK OF LIQUIDITY

Variable annuities are highly illiquid investment vehicles. As noted above, surrender charges can severely limit an annuity owner’s ability to move assets out of an annuity in the early years of the contract. Further, while most variable annuities allow contract owners to withdraw a specified amount during the accumulation phase, withdrawals beyond this amount typically result in a company-imposed charge. Any withdrawals of gains are subject to ordinary income taxes on the Federal level and associated state income taxes, and withdrawals made before the contract owner reaches age 59 ½ may be hit with an additional 10% tax penalty. Withdrawals made from a fixed interest rate investment option could also experience a “market value adjustment” or MVA. An MVA adjusts the value of the withdrawal to reflect any changes in interest rates from the time that the money was invested in the fixed rate option to the time that it was withdrawn.

COMPLEXITY

Variable annuities can be extremely complex products, which can confuse buyers and obfuscate fees and expenses. Quite often, even the salespeople who sell them do not fully understand how they work, and so salespeople sometimes prey on a buyer’s emotions to sell variable annuities rather than the merits and suitability of the products themselves. We believe that investors should fully understand what they own and how much they are paying to own it.

CREDIT RISK

Variable annuity assets invested in variable sub-accounts are considered assets of the contract holder and not the issuing insurance company, meaning that these assets would not be at risk in the event of an insurance company failure. However, the same cannot be said for variable annuity assets held in fixed rate investments. These assets legally belong to the insurance company and would therefore be at risk if the company were to fail. Similarly, any guarantees that the insurance company has agreed to provide, such as a guaranteed minimum income benefit, would be in question in the event of a business failure. There are some third-party protections in place for variable annuity owners, such as state guaranty associations, but these protections are limited. Therefore, potential purchasers of variable annuities should understand and consider the financial condition of the issuing insurance company before entering into an annuity contract.

Who Should Own a Variable Annuity?

While the advantages and drawbacks of various types of annuities can be debated, the real issue surrounding annuities is that of suitability. Put simply, the question is: who should own a variable annuity? This question can be difficult to answer, given the myriad variations available in the variable annuity universe, but there are some basic guidelines that can help investors decide whether or not annuities should play a role in their financial plans.

These products are designed to deliver a series of cash flows with a guaranteed floor, typically in the latter stages of one’s life, as a hedge against the risk of outliving one’s assets. Investors who have substantial asset bases and who therefore face minimal longevity risk would generally have little use for annuities, especially given the high costs of such products. Similarly, individuals who are part of employer-sponsored pension plans or who receive material Social Security payments would get little incremental value from the protections afforded by annuity products because these individuals already have protection in place against longevity risk.

Given the structure, costs, tax treatment, etc. of variable annuities, it would appear to us that the only investors who should consider owning variable annuities would be those who:

- Are in a high income tax bracket and expect to be in a lower tax bracket in retirement;

- Have exhausted all other tax-deferral vehicles;

- Have little need for liquidity;

- Expect to have a substantial remaining lifespan;

- Are comfortable relinquishing control of their capital to an insurance company;

- Are willing to accept full or partial constraints on the transfer of assets to their heirs upon their demise;

- Have a very low tolerance for investment loss.

This situation is highly limited; few people really fit into this rather tight description. Individuals who do not meet these criteria would be better served, in our estimation, by putting their capital toward other types of investments that could potentially generate greater investment returns that are not dragged down by the high fees associated with variable annuities while also providing greater liquidity and potentially more optimal tax treatment.

Closing Thoughts

We believe that we have taken an objective and nuanced approach to understanding and analyzing variable annuities, and we conclude that, in most cases, the drawbacks of these products simply outweigh the benefits that they might confer. Of course we understand that every investor’s situation is unique; therefore any discussion of a specific variable annuity contract should take into consideration the investor’s unique circumstances and the specific terms of the contract in question in order to determine its suitability. With that in mind, if you currently own a variable annuity or are considering purchasing one, we encourage you to speak with your portfolio manager to better understand how a variable annuity may or may not fit into your overall portfolio.

- http://www.limra.com/Posts/PR/Data_Bank/_PDF/2006-2015-Annui-ties-Sales-Estimates.

- Fixed annuities will be a topic for a future Navigator.

- In finance, the word “guarantee” often times has a negative connotation to it. In the world of investments, volatility of returns can be expected, and, usually, when there is a guarantee of sorts, it usually means that the bar of the minimum guaranteed return is so low that one would question the value of the guarantee at all. It should be noted, however, that these sorts of guaranteed returns often times are the primary selling points for variable annuities.

- A GMAB rider guarantees that if, after a set number of years, the value of the annuity is lower than the total amount of purchase payments made, the annuity will be adjusted upward to equal the total value of purchase payments made to the annuity.

A GMWB rider guarantees the contract owner the ability to withdraw a set percentage of the annuity’s value from the annuity each year until the total of all withdrawals equals the original purchase payment value. This essentially acts as a “money back” guarantee in cases in which investment performance is poor.

A GMIB rider provides that a contract owner’s annuity payments will be based on the greater of the actual annuity value or a hypothetical value determined by applying a guaranteed annual rate of return.

This article is prepared by Pekin Hardy Strauss Wealth Management (“Pekin Hardy”) for informational purposes only and is not intended as an offer or solicitation for business. The information and data in this article does not constitute legal, tax, accounting, investment or other professional advice. The views expressed are those of the author(s) as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions.