Photo by cacaroot.

“In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.”

– Rudiger Dornbusch, economist

Value investing can be a challenging endeavor, even in the best of times. It involves investing long-term capital in companies that are unknown, unloved, or unpopular. In our view, the only reason value investing receives any attention is that it has historically outperformed the broader equity markets over the long-term when applied in a disciplined and consistent manner.[1] That being said, when value investing underperforms over multi-year periods, as is the case today, skeptics wonder what the heck value investors were thinking by investing in such undeserving companies.

In 2015, the equity markets experienced the sixth year of an extended period of outperformance by growth stocks. Large cap value stocks underperformed large cap growth stocks by a whopping 11.5% in an incredibly bifurcated market environment. This means that expensive stocks in glamorous companies have become even more expensive, while inexpensive stocks in slower-growth, out-of-favor companies have become more attractive. In 2015, there were a few stocks whose share prices continued to increase in value at a very rapid rate, and a large number of stocks that generated negative returns.

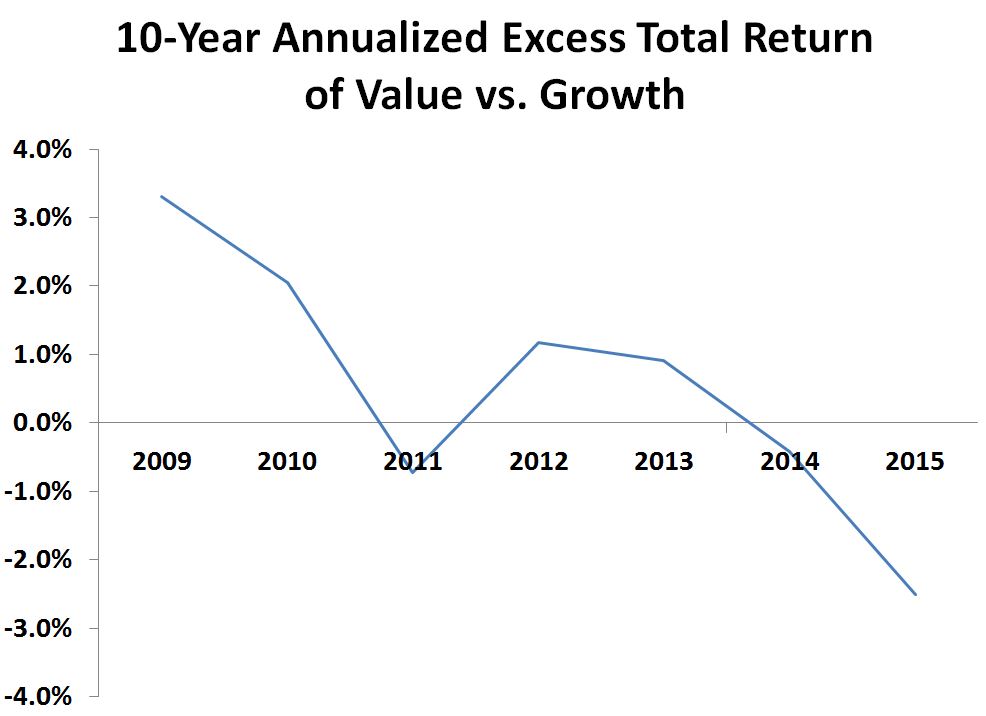

The chart provided at the top of the next page illustrates the underperformance of value stocks relative to growth stocks since 2009 and reinforces the notion that recent years have been a challenging time to be a value investor. Today’s growth darlings are large-cap tech companies, such as Netflix, Facebook, Amazon, and Salesforce.com. These stocks far outpaced the market in 2015 as their P/E ratios expanded and bolstered the -0.87% performance of the MSCI World Index.

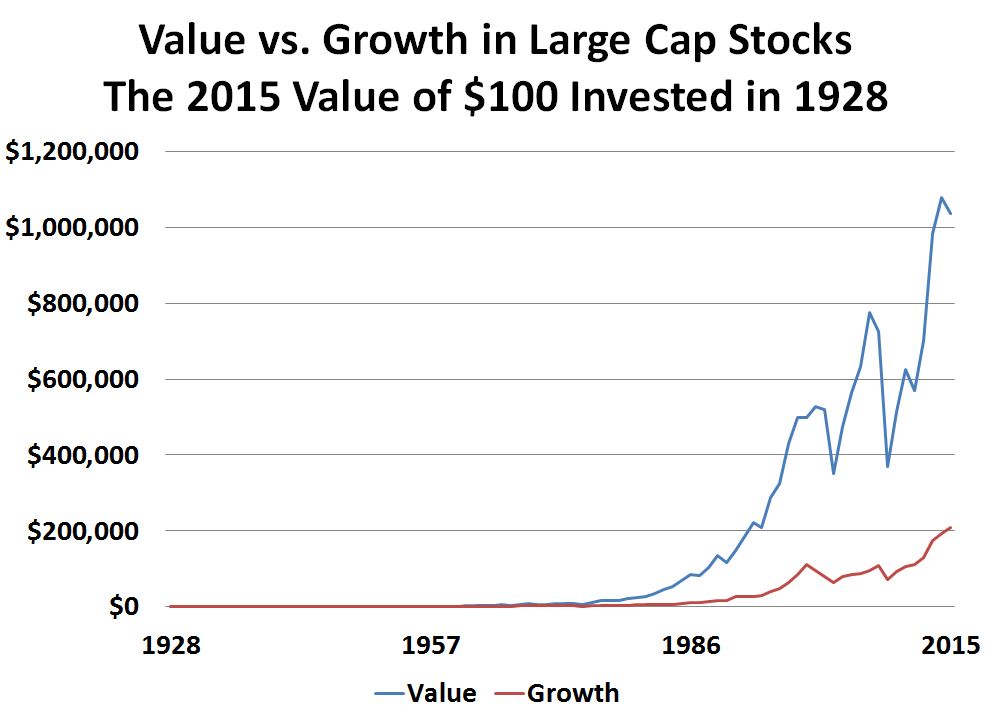

Looking beyond recent history, large cap value stocks have outperformed large cap growth stocks by 2.0% per year on average since 1927, while small cap value stocks outperformed small cap growth stocks by 4.4% per year on average. While value investing can underperform growth investing in a pronounced way over multiple years, as it is doing today and as it did in the late 1990s during the dot-com bubble, value investing remains a superior strategy, in our view, because of its track record and because it is built on the principle of buying stocks whose share prices are depressed and selling stocks whose share prices are expensive.

{kind=link}

Value Is Currently Underperforming Growth….

Source: Ibbotson & Associates.*

…But Has Outperformed Over the Long-Term

Source: Ibbotson & Associates

*Growth: Fama-French Large Growth TR USD, ValueL Fama-French Large Value TR USD

Our value investing approach, similar to that pursued by Warren Buffett and Benjamin Graham, entails selectively investing in quality, undervalued companies that are temporarily out of favor, and then waiting for Mr. Market to change his mind about the attractiveness of owning such companies. Sometimes the wait is a long one; in the case of the performance of value stocks versus growth stocks, the wait has lasted for six years. Today’s extended outperformance of growth stocks and underperformance of value stocks reminds us of the market environment that investors experienced during the dot-com bubble in the late 1990s.

At this point, some investors might ask the question, “Isn’t it time to throw in the towel and begin buying the growth stocks that are going up in price?” In our view, investing in overvalued companies just because their share prices are rising is a recipe for permanent capital losses. Speculators learned this lesson the hard way when the dot-com bubble burst, and then they learned it again when the housing bubble burst.

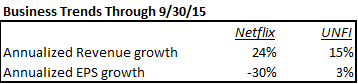

Two Illustrative Examples: United Natural Foods (UNFI) versus Netflix (NFLX)

Clients sometimes ask us to describe examples of value stocks and growth stocks, so we are going to compare United Natural Foods (UNFI), a value stock, and Netflix (NFLX), a growth stock, and use these stocks to illustrate the differences. UNFI is a leading natural food distributor, while Netflix is a leading distributor of over-the-top (OTT) video content. Both companies are leaders in their respective industries.

During the past 12 months, Netflix has grown revenues at a faster pace than UNFI, but Netflix’s earnings per share have declined by nearly one-third. Meanwhile, UNFI revenues have grown at a double-digit rate, and earnings per share have increased. That said, organic revenue growth at UNFI is decelerating due in part to the loss of an important customer (Albertsons). Revenue growth at Netflix remains strong due to the continued expansion of the company’s OTT subscription service.

In 2015, Netflix was one of the few stocks that generated meaningfully positive returns, as the Netflix share price increased by 134%. Its share price increased faster than its revenues, despite a decline in earnings per share. Investors are currently valuing Netflix at an all-time high multiple of sales of 8x, which is far more expensive than the 1x sales multiple that investors were willing to pay for its shares just four years ago. As a multiple of operating profit, investors are valuing Netflix at 150x, which is triple the 50x operating profit multiple that investors were willing to pay for Netflix shares just one year ago.

In contrast, 2015 was a horrible year for the UNFI share price. Despite revenue and EPS growth, its share price has declined by half. Today, the company is valued by investors at a sales multiple of 1x and an operating profit multiple of 10x. UNFI’s business has grown consistently for years, and it is usually a popular stock among growth investors. However, this is one of the few times in which UNFI has been thrown into the value trash bin; the last time UNFI traded at valuation multiples this low was during the financial crisis.

We want to also compare and contrast current management behavior with respect to personal stock transactions. Netflix management generates additional compensation through stock option grants, and management regularly exercises their stock options and sells their Netflix shares to the public. As for UNFI, at today’s stock price, management has been taking their hard-earned compensation and buying additional UNFI shares on the open market.

In 2015, owning Netflix shares represented a home run, while owning UNFI would have been a disaster. The story of these two stocks was the story of growth and value last year. We suspect that UNFI’s share price has much better prospects over the next five years than the NFLX share price.

The Path to Monetary Normalization

In our last quarterly letter, we mentioned that cash in U.S. dollars had outperformed almost every other asset class in the world since the end of the Federal Reserve’s quantitative easing program (October 29, 2014). We think the strength of the dollar and the underperformance of more risky assets — particularly commodities and emerging market currencies – has been driven by the implicit monetary tightening, in the form of a stronger dollar, that has occurred since Fall 2014.

Monetary tightening continued with the Federal Reserve’s decision in December 2015 to finally raise interest rates for the first time in almost a decade. We view this decision as a remarkable policy change made all the more remarkable because deflationary pressures in the global economy at the moment are weighing far more heavily than inflationary factors. We believe the Federal Reserve is trying to reverse the easy monetary policies that have taken place over the past five years and that have inflated financial assets, despite weak economic growth.

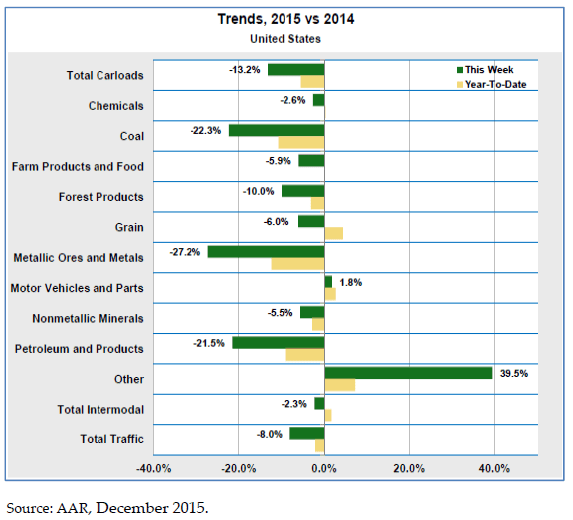

The industrial and materials sectors are already contracting, and global exports have

declined to the second lowest level since 1957. In the United States, railroad car loadings, which is a useful economic indicator, generated a 1.1% decline in 2015, and the decline rate is worsening, not improving (see chart to the right).

Since the financial crisis of 2008, economic growth has been driven by Federal Reserve policies that encourage credit growth. Using the credit expansion logic of Popeye’s friend Wimpy, when you buy hamburgers today that you promise to pay for on Tuesday, the economy grows. And, when interest rates are kept artificially low for years, private and public credit grows even faster than the economy. In the United States, private credit is currently growing at a 5% annual rate.

However, by ending its quantitative easing policy last year and raising the Fed Funds rate by 0.25% in December, the Federal Reserve has begun reversing the economic machinery that has inflated asset prices and driven the growth of the global economy since 2009. Low interest rates inflated asset prices, encouraged credit growth, and led to six years of tepid economic expansion (and a far more indebted global economy). Higher interest rates will reduce private credit growth, and declining private credit growth will dampen GDP growth. We certainly have been here before — the last two recessions were caused by the Federal Reserve raising rates and deflating the asset bubbles that it had previously created with interest rates that were too-low-for-too-long.

In summary, as long as the dollar continues to rise against other currencies at the same time as the Federal Reserve raises interest rates, we expect the economy to continue slowing. We believe the risk of a recession is high and growing at the moment.

Gold’s Investment Merits

We have held an allocation to gold over the past several years in client portfolios as a hedge against a decline in the dollar’s purchasing power, and that allocation has detracted from performance until the events of early 2016. Our concerns arise in light of how leveraged and unsustainable the monetary system has become with record levels of debt and derivatives. Over the last two years, gold has continued to decline in value versus the dollar, although gold has performed better than almost every fiat currency besides the dollar. There are several reasons why, looking out five years, we continue to be comfortable owning a meaningful gold position at current prices.

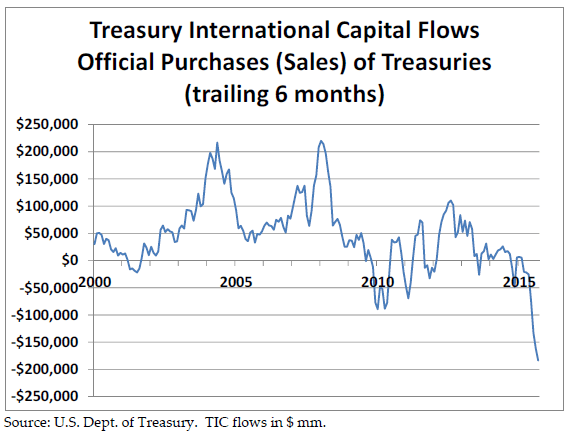

1. Foreign central banks are selling their U.S. Treasuries. The primary export of the United States over the past 35 years has been trillions of dollars of Treasury bonds, which have become the central pillar of the international monetary system. Our trading partners sell their goods to the United States in exchange for dollars, which foreign central banks have used to purchase Treasury bonds to be held as foreign currency reserves. By purchasing Treasury bonds instead of goods, foreign central banks have kept interest rates low and held up the exchange rate value of the dollar. However, beginning in 2015, foreign central banks, led by the People’s Bank of China, ceased accumulating U.S. Treasuries, and began selling them at a record pace. Whatever the reasons, this de-dollarization of foreign reserves represents a significant change for the international monetary system which will result in lower demand for the U.S. dollar over the long-term.

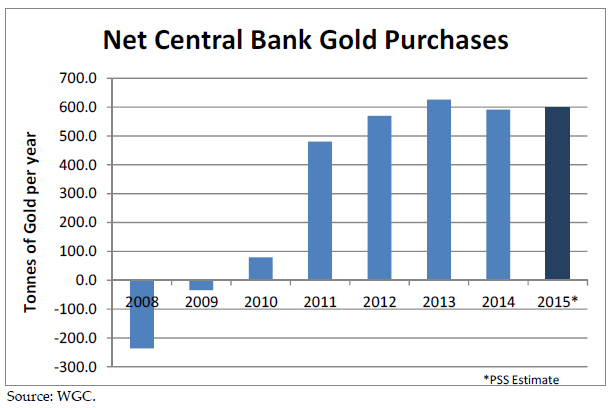

2. Foreign central banks are buying gold. Ever since the financial crisis, and perhaps in anticipation of the monetary policy changes now being implemented, foreign central banks have been accumulating gold as a hedge against their dollar denominated (U.S. Treasuries) foreign reserves. These purchases continue unabated. The People’s Bank of China, which has been the largest seller of U.S. Treasuries, has also begun disclosing its monthly purchases of gold. While central banks are reducing their holdings of U.S. Treasuries, they have been acquiring gold in 2015 at a pace of 125 to 150 metric tons per quarter. An increase in central bank gold reserves in conjunction with a decline in dollar reserves is decidedly bullish for gold.

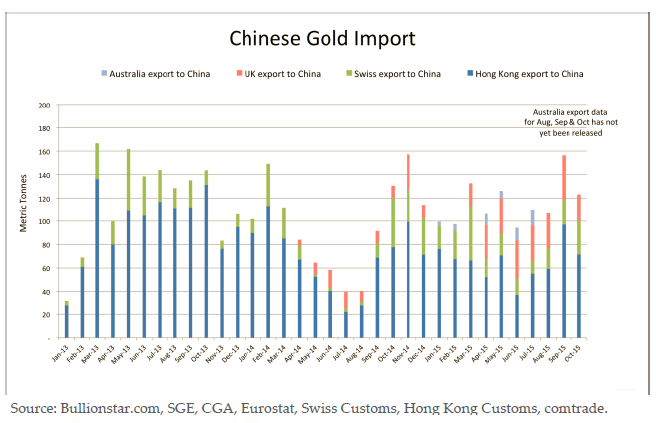

3. Since 2013, physical gold has been moving from West to East at a steady but rapid pace. China has imported gold from Western countries at a rate of at least 100 metric tons per month. Meanwhile, the largest physical gold exchange traded funds (GLD), which owns gold stored in London, has realized an inventory decline of more than 50% since the beginning of 2013. We think the demand for physical gold from China and India will eventually result in physical supply shortages that is likely to be resolved with a higher price for physical gold.

Given the strength of the dollar and gold’s strong long-term fundamentals, we expect that our patience will be rewarded over the intermediate period ahead.

Interim Comments on the Financial Markets in January

As we write this letter, the financial markets are experiencing a heightened level of volatility, and the S&P 500 Index has declined by approximately 8% year-to-date in 2016. “Risk-off” assets such as the dollar, gold, and US Treasury bonds have strengthened while global equities, emerging market currencies, and high yield (junk) bonds have declined in value. As a result of a slowdown in China, an oversupplied oil market, and continued strength in the U.S. dollar, deflationary pressures are building in the global economy which are adversely affecting financial asset prices. We have been surprised at the extent and duration of the current chaos in oil prices, but we anticipate that oil prices will bottom in 2016 as U.S. oil production continues to decline.

We have no crystal ball to predict where the market is going in 2016, but we generally think it is prudent to own a diversified portfolio of uncorrelated, reasonably valued asset classes. Due to elevated equity valuations, we remain underweight stocks compared to our strategic allocation targets. Even after the recent market correction, most stocks have a poor risk-reward profile at current share prices. With your fixed income investments, we are generally continuing to keep your bond maturities short, as we seek to generate a modest level of income while we wait for interest rates to eventually rise.

We wish you a happy, healthy, and prosperous 2016, and we thank you again for trusting us as your financial advisor. During the current volatile market environment, we hope that you will not hesitate to reach out to any of us with your questions and concerns.

Sincerely,

Pekin Hardy Strauss Asset Management

[1] Source: Ibbotson & Associates.

This commentary is prepared by Pekin Hardy Strauss, Inc. (dba “Pekin Hardy Strauss Wealth Management”, “Pekin Hardy”) for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any security. The information contained herein is neither investment advice nor a legal opinion. The views expressed are those of the authors as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. Pekin Hardy Strauss Inc. cannot assure that the type of investments discussed herein will outperform any other investment strategy in the future. Although information has been obtained from and is based upon sources Pekin Hardy believes to be reliable, we do not guarantee their accuracy. There are no assurances that any predicted results will actually occur. Past performance is no guarantee of future results.

Fama-French value stocks are defined as those that have high ratios of book value to market value and growth stocks are defined as those that have low ratios of book value to market value. The S&P 500 Index measures an index of 500 stocks chosen for market size, liquidity and industry grouping among other factors. The MSCI World Index is a widely followed, unmanaged group of stocks from 23 international markets. Individuals cannot invest directly in these indices, however, an individual can invest in exchange traded funds or other investment vehicles that attempt to track the performance of a benchmark index.