“Gold gives to the ugliest thing a certain charming air,

for that without it were else a miserable affair.”

─ Molière

The first six months of 2020 have been historic. Thus far, the year has offered up a global health pandemic, a synchronized global recession, rising social unrest, extreme levels of market volatility, and record-breaking fiscal and monetary stimulus. It should be no wonder that investors have begun to turn towards gold as a safe haven.

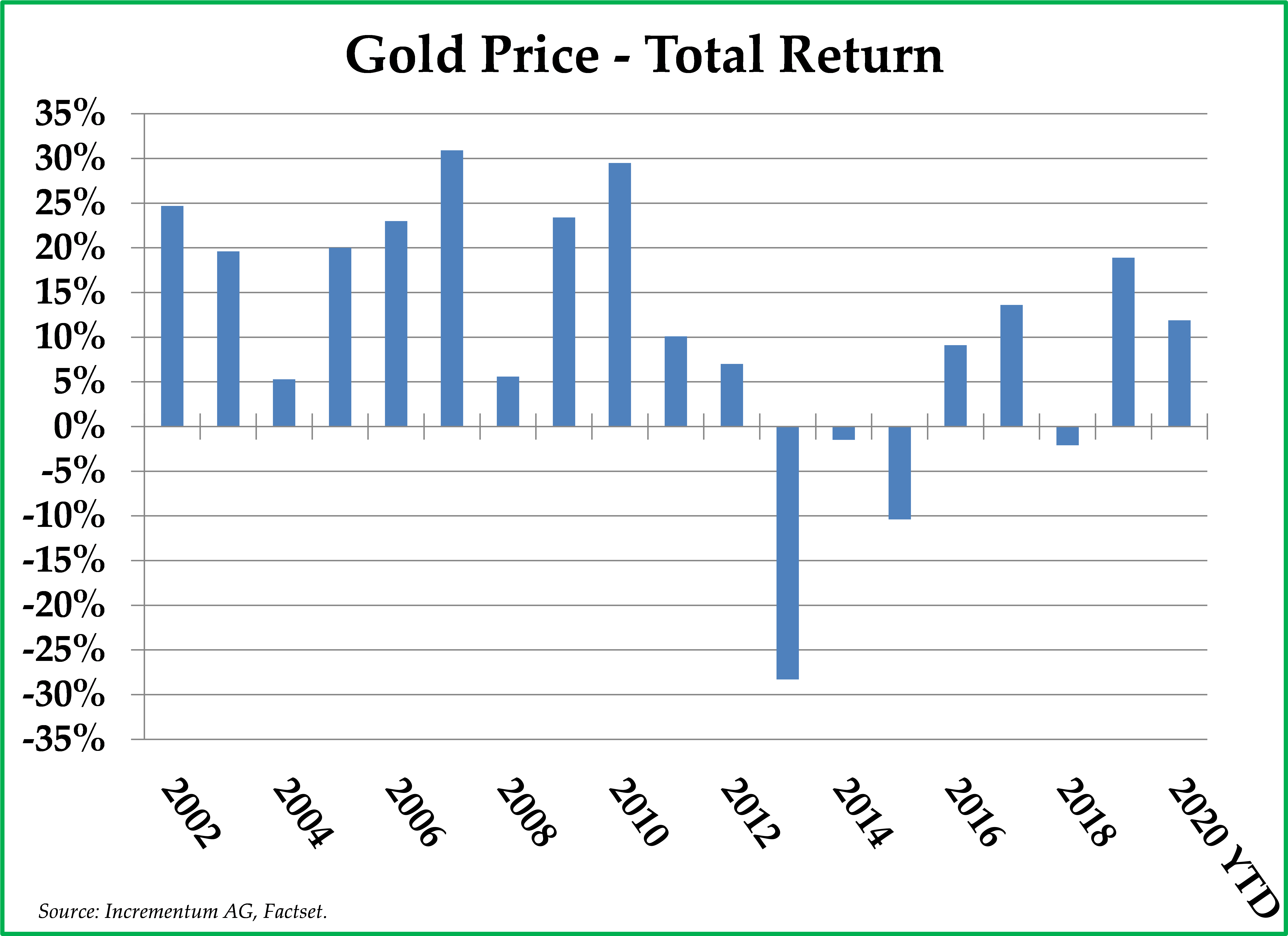

Over the year ended on June 30, 2020, the price of gold has increased by 27%; over the past six months, the price of gold has increased by 12%. The remarkable recent performance of gold has helped the performance of our clients’ portfolios during a period of enormous economic, political, and social instability. Despite a markedly increased gold price, we remain bullish on gold going forward, for reasons outlined below:

- Gold’s Track Record In the Bubble-Bust Era

When the Dot-com bubble deflated in 2000, the Federal Reserve debased the dollar at a level not experienced in decades. Federal Reserve Chairman Alan Greenspan slashed the short-term interest rate from 6.5% in January 2000 to below 2% in January 2002, and he kept the short-term interest rate below 2% for years thereafter. In response, the real estate market boomed as households applied low-cost financing to bid up home prices. When the housing market crashed six years later, Alan Greenspan’s successor, Ben Bernanke, dropped the short-term interest rate from 5.25% in June 2007 to below 0.25% in January 2009, and he kept the short-term interest rate below 0.25% for years thereafter. This year, the Federal Reserve has again pushed the short-term interest rate down to nearly 0% in order to protect the financial system from yet another crash.

–

This brief history is highly relevant to our gold investment thesis. During this era of bubbles and busts, fueled by low-interest rates and unprecedented levels of monetary debasement, gold has generated a 9.3% annualized return, far outperforming the investment return of the S&P 500 Index, which has produced an annualized return of 5.7%.1 Simply put, the driver of this phenomenon is this: as the dollar depreciates and inflation accelerates, the price of gold denominated in dollars appreciates at the same time that corporate profit margins compress due to increasing costs. Looking forward, we anticipate that the Federal Reserve’s interventions will continue and monetary debasement will necessarily accelerate during the coronavirus era. For this reason alone, we believe that gold will outperform other asset classes over the intermediate period ahead.

– - Gold Offers Portfolio Diversification

We also own gold because it is a portfolio diversifier. Gold is in an asset class all by itself, with the price of gold showing limited correlation to the price movement of either stocks or bonds. Due to its low historical correlation to traditional financial assets, the addition of gold to a portfolio of stocks and bonds should enhance portfolio returns and simultaneously reduce volatility, in our view.

–

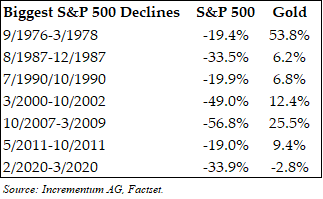

This year, our investors have experienced the beneficial effect of gold’s low correlation first-hand. The attractive returns of owning gold in 2020 have helped to offset the negative returns from owning stocks during the first half of 2020. Typically, gold has served to protect investment portfolios during the largest market declines over the past several decades.

– - Helicopter Money Has Begun to Drop

Congress and the President are likely to enact legislation approving, in aggregate, $10 trillion or more in stimulus measures this year, including steps that involve directly sending trillions of dollars of checks to households and small businesses. We believe it is likely that fiscal spending will exceed 25% of GDP during 2020. This enormous deficit will be financed by the Federal Reserve, which plans to print additional money to buy Treasury bonds that the government will issue to cover this spending. Ben Bernanke has advocated for this combined fiscal and monetary approach, called helicopter money, in a famous speech he wrote in 2002 about how to combat deflation and create inflation.While the U.S. economy remains in deflation, it is just a matter of time before this helicopter money policy creates inflation, in our view. Since the end of April, inflation has already appeared in food prices, in personal protective equipment, and in oil prices. When inflation takes hold across other sectors of the economy and the consumer price index rises above 3%, we expect that this will be a particularly favorable environment for rising gold prices, as investors will seek to own real assets which could serve as a store of value. In the 1970s, the United States experienced sustained inflation rates above 4.6%; during that period, the gold price increased 15x from $35 to $541 per ounce. We are not forecasting such an astonishing return. Still, we believe that gold is positioned to perform better than most asset classes should helicopter money cause inflation, as Ben Bernanke predicted in his 2002 speech.

– - Negative Real Interest Rates are Bullish for Gold

During World War II, the U.S. government issued a record amount of debt held by the public, representing 106% of GDP. To pay off this debt over time, the United States rolled out a series of policies including capping interest rates below the level of inflation, creating negative real interest rates, and regulating banks to force them to buy U.S. Treasuries. Over the next several decades, the United States gradually reduced its debt load as wealth transferred from savers, who earned below-inflation rates of return, to the U.S. government, who paid below-inflation rates of interest.The U.S. debt to GDP ratio is in a similar place as it was after World War II, having increased from 35% of GDP in 2007 to more than 100% of GDP now. Unsurprisingly, economists are rolling out the same playbook to help the U.S. government gradually pay down its debts. Due to bond purchases by the Federal Reserve, 30-year U.S. Treasury bond interest rates are now below 1.3%. With capped bond yields and inflation expectations starting to rise quickly, policymakers are again creating an environment for bond investors to generate negative real yields on their Treasury bond investments.Needless to say, an environment where bond yields are not compensating investors for inflation is an environment where the price of gold should rise, in our view. Negative real (inflation-adjusted) yields should nudge investors into investments like gold which are liquid, real, and held by central banks around the world as a reserve asset.

– - Gold Outperforms in Both Deflationary and Inflationary Environments

If the economy continues to shrink nominally and credit defaults accelerate, which is an unlikely scenario due to aggressive fiscal and monetary policies, the economy should remain in deflation. In such a deflationary environment, gold should serve as a safe haven, and gold’s purchasing power should increase as the prices of financial assets and commodities plummet, such as what occurred in March 2020 and also during the Great Depression and the 2008-2009 Financial Crisis. In response to continued deflation, the Federal Reserve is likely to do whatever it takes to provide liquidity, reflate financial assets, and provide funding for additional fiscal spending until deflation finally turns into inflation. Then, when inflation eventually does take hold, investors should continue to buy gold as a store of value. Whether as a safe haven in deflation or as a store of value in inflation, gold should outperform during extreme economic events.

– - Gold is Undervalued

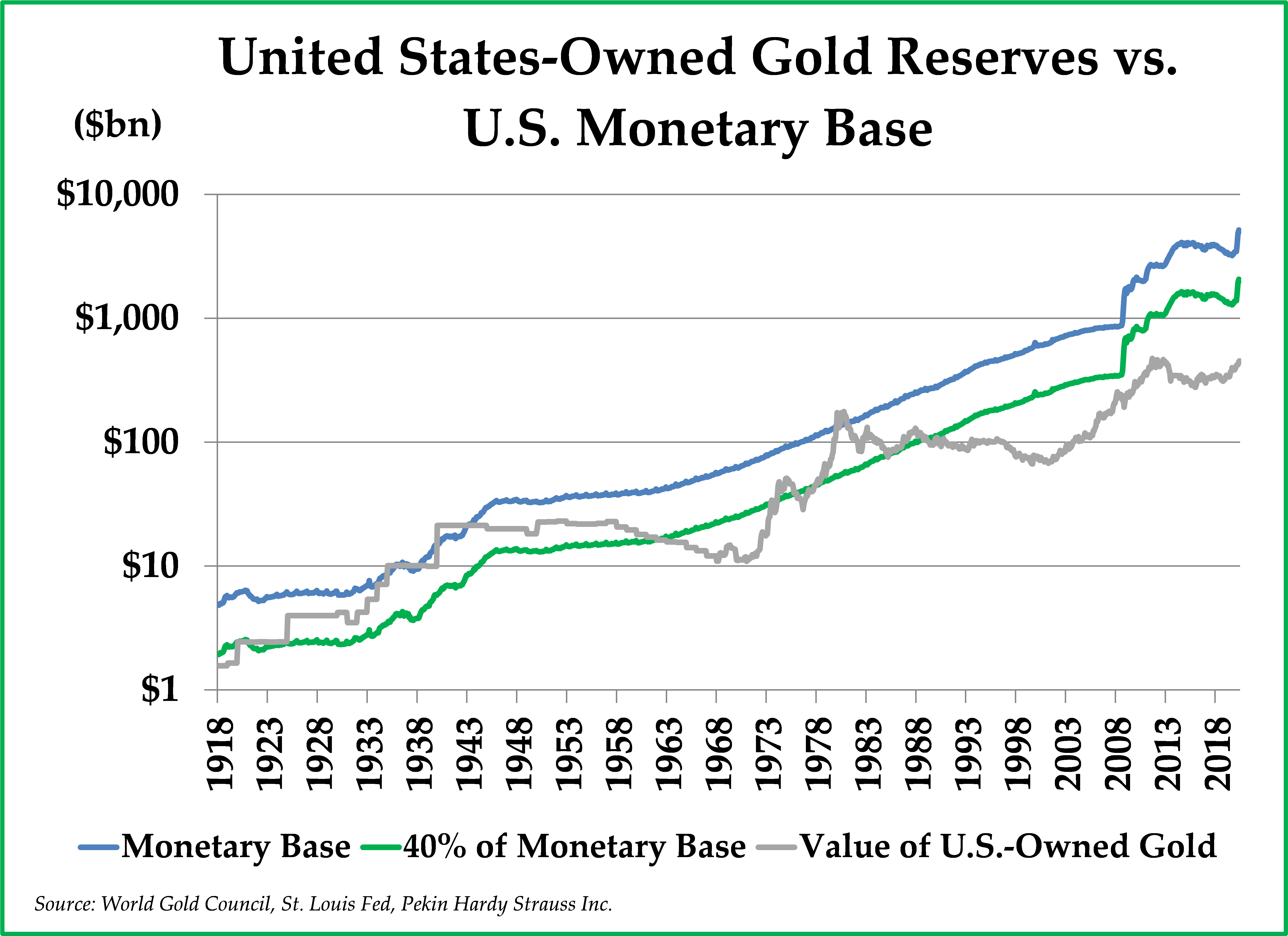

When Congress passed the Federal Reserve Act in 1913, the Act required 40% gold backing of all Federal Reserve notes that were issued. While the dollar is no longer backed by gold, a strong connection has continued to exist between the value of U.S. gold reserves and the U.S. monetary base. The supply of money has increased manifold over the past 107 years, and the money supply increase has accelerated sharply this year. While the gold price has increased by 12% during the first half of 2020, the money supply rose at an even faster pace, by 20.9%. In other words, the rise of the gold price has not been keeping pace with the remarkable rise in the money supply in 2020.Moreover, the rising gold price has not kept pace with the increase in the money supply since the creation of the Federal Reserve. The value of U.S. gold reserves relative to the U.S. monetary base has fluctuated over time, rising to more than 100% in 1981, but it currently stands at close to an all-time low of just 9%. Our bullishness concerning gold going forward is informed in no small part by two fundamental factors. First, gold appears inexpensive relative to the enormous growth of the U.S. monetary supply. Second, we expect that the money supply will continue to grow at a rapid rate in the years ahead.

–

–

– - Gold is Underowned

Despite gold’s attractiveness as an investment, it remains an underowned asset for several reasons. First and foremost, it is not available as an option in most employer-sponsored retirement plans. Similarly, gold is not available as an option in 529 education savings plans. Pension plans generally do not own any gold either. As a result, the market capitalization of all of the gold that exists in the world is only $8 trillion, which is just a little bit larger than the expected Federal budget deficit in 2020.The typical investment portfolio is currently a 60/40 balanced portfolio, which means 60% is allocated to stocks and 40% is allocated to bonds. For young investors, the portfolio might be tilted towards an increased allocation to stocks, while older investors own more bonds. Regardless of the stock/bond mix, if the average investor were to allocate just 5% of his or her portfolio to gold, the gold price would have to rise significantly to accommodate the incremental investor demand and capital flow into gold.

– - Gold Is Currency Crisis “Insurance”

If it occurred, a currency crisis of some sort would be a worst-case scenario for the dollar and, at the same time, a best-case scenario for the price of gold. With that said, our gold bullishness does not hinge on a currency crisis; continued monetary debasement alone at accelerating rates creates a perfect environment for rising gold prices.We believe that gold is the best asset to own in a currency crisis. A currency crisis is generally precipitated by deficit spending and money printing that become so egregious that foreign investors move their capital out of the country, resulting in a local currency that drops sharply in purchasing power. The central bank then finds itself having to print even more money to fund further borrowing, which results in even higher prices. And so on.In Lords of Finance – the Bankers Who Broke the World, Liaquat Ahamed described how the Weimar hyperinflation occurred in post World War I Germany, which followed the typical path of a currency crisis:

Von Havenstein [chairman of the Reichsbank] faced a real dilemma. Were he to refuse to print the money necessary to finance the deficit, he risked causing a sharp rise in interest rates as the government scrambled to borrow from every source. The mass unemployment that would ensue, he believed, would bring on a domestic economic and political crisis, which in Germany’s current fragile state might precipitate a real political convulsion. As the prominent Hamburg banker Max Warburg, a member of the Reichsbank’s board of directors put it, the dilemma was ‘whether one wished to stop the inflation and trigger the revolution,’ or continue to print money. Loyal servant of the state that he was, Von Havenstein had no wish to destroy the last vestiges of the old order.

If this dilemma sounds familiar to you, it sounds familiar to us. However, this is not our base case; the United States, in contrast to Germany during the Weimar Republic, issues the world’s reserve currency, which is a significant difference. The dollar remains the most widely used fiat currency in the world. Moreover, private investors are still investing their capital in the United States. While we are expecting the dollar to depreciate, a currency crisis, while possible, remains an unlikely scenario.

We have asked ourselves what will happen to the U.S. dollar as the debt/GDP ratio increases from 100% to 200% during the next decade or as the fiscal deficit increases to 25% of GDP by the end of this year. We have similarly wondered what might cause foreign private investors to bring their money home or invest their capital elsewhere. Without knowing the answers to these questions, we are sleeping better at night with our clients owning gold as currency “insurance”.

Having summarized the reasons for our bullishness and having purchased a core position in gold in our clients’ investment portfolios, we want to offer a word of warning. Gold’s price can go down meaningfully before it goes up. Indeed, our clients have suffered through several meaningful drawdowns since we first began buying gold in 2005. In 2008, the price of gold crashed by 34% before recovering. In March 2020, the gold price corrected by 15% before rising again quickly. And, between 2011 and 2015, the price of gold declined by 45% before starting to rise again.

When the gold price corrects, as it did in March, we expect to hold onto our clients’ positions or, if anything, use it as an opportunity to buy more gold at a less expensive price. Our decision to sell gold in the future will be driven by our judgment that gold is fully valued or that the fundamentals that support a higher gold price have changed. We look forward to that day, because it will be good news for the economy and the world.

We hope that you are doing well and that you and your families are staying healthy. At Pekin Hardy Strauss Wealth Management, we are continuing to work from home to minimize the risk of the coronavirus spreading within our office, but we are engaged and ready to talk to and meet with you. Please do not hesitate to reach out to your portfolio manager to arrange a video meeting or phone call to discuss any questions or concerns that you might have about your financial plan or investment portfolio. Thank you again for your trust in our firm’s ability to navigate your retirement savings through this uncertain time.

Sincerely,

Pekin Hardy Strauss Wealth Management

1 Source: Factset, 12/31/99‐6/30/2020.

2 We talked about this important speech at length in our last quarterly commentary

This commentary is prepared by Pekin Hardy Strauss, Inc. (dba Pekin Hardy Strauss Wealth Management, “Pekin Hardy”) for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any security. The information contained herein is neither investment advice nor a legal opinion. The views expressed are those of the authors as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. Although information has been obtained from and is based upon sources Pekin Hardy believes to be reliable, we do not guarantee its accuracy. There are no assurances that any predicted results will actually occur. Past performance is no guarantee of future results. The S&P 500 Index includes a representative sample of 500 hundred companies in leading industries of the U.S. economy, focusing on the large-cap segment of the market. The Consumer Price Index (CPI) is an unmanaged index representing the rate of the inflation of U.S. consumer prices as determined by the U.S. Department of Labor Statistics.