401(k) plans have grown in popularity over the past few decades and are now the preferred type of employer-sponsored retirement savings plan. Many companies have moved away from defined-benefit plans/pensions in favor of 401(k) plans. Many 401(k) plans provide both Roth and Traditional options. These two options are quite similar but differ in a few important aspects. We’ll compare the Traditional and Roth 401(k) plans and highlight the similarities and differences to help provide a clear framework for deciding which makes the most sense for you. Your current income level and tax rate, as well as your income and tax rate expectations in retirement, should be key factors in your decision.

Traditional 401(k)

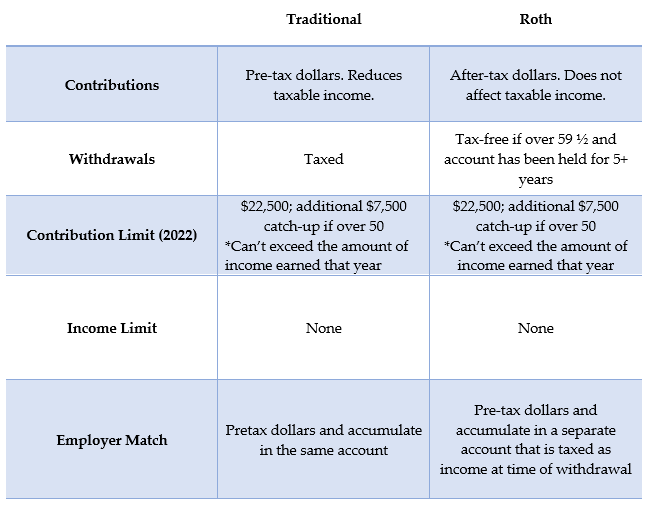

A Traditional 401(k) is an employer-sponsored retirement account that uses your pre-tax income as a source of contributions. Put simply, money is taken from your paycheck before taxes are withheld. The taxes are deferred until you receive distributions during retirement. In addition, employers often provide matching contributions and/or profit-sharing contributions. Once you start receiving distributions, those distributions will be taxed at your ordinary income tax rate, along with any applicable state taxes. The Traditional 401(k) has a contribution limit of $22,500 with a catch-up contribution of $7,500 for people 50 and older, as of tax year 2023. Penalty-free distributions from the Traditional 401(k) can begin at age 59 ½ and do not carry a holding period requirement.

Pros: Contributions to a Traditional 401(k) reduce an individual’s taxable income for the current year, as contributions to a Traditional 401(k) are made with pre-tax dollars. This benefit is especially important if you are currently in a high-income tax bracket, and you expect to be in a lower income tax bracket when you retire.

Cons: Tax rates and brackets are always subject to change and are generally difficult to predict. It is difficult to accurately forecast the tax rate that will be applied when you receive distributions during your retirement years. If tax rates increase or if you expect to have more income in retirement than you are currently generating, you may be creating a greater tax burden in retirement for yourself than is necessary.

Scenario: Let’s assume that your current salary is $200,000 and your employer offers a 100% match up to 5% of your total earnings. Let’s also assume that you will contribute $10,000 dollars of your own wages, which means that your employer will also contribute $10,000. The $10,000 that you contribute will be deductible and your new W-2 wages will be reduced to $190,000. However, when you retire and/or begin to take distributions on that money, you will have to pay federal income tax and possibly state income tax on your contributions at ordinary income tax rates, which might be higher in retirement than they are currently.

Roth 401(k)

A Roth 401(k) is an employer-sponsored retirement account that uses after-tax income as its source of contributions. Like the Traditional 401(k), if you are under the age of 50, you may contribute $22,500 for the year 2023, and you are allowed to contribute an additional $7,500 if you are 50 or older. As for the distributions from the Roth 401(k), they may be taken at age 59 ½ without penalty, but the account must have been held for at least five years. Qualified withdrawals from this account, including both contributions and any investment growth, are not taxed at all. However, any employer match is subject to tax.

Although personal contributions are made with after-tax dollars, any employer match (if one exists) would be made with pre-tax money and placed in a separate Traditional 401(k) account. This money will then be taxed when it is distributed or converted to a Roth account.

Pros: Unlike a Roth IRA, there are no income limitations to making contributions towards a Roth 401(k), making it a more accessible option for high income individuals. Also, the contribution limit is significantly greater than the contribution limit of a Roth IRA. The most important feature of the Roth 401(k) is tax-free growth. Under current tax law, the growth of the Roth 401(k) account is not taxed, and distributions are also not taxed.

Cons: Because a Roth 401(k) uses after-tax dollars, contributing to a Roth 401(k) may not make sense if you are currently in a high-income tax bracket and you are expecting a lower tax rate in retirement, which many do. Unlike a Roth IRA, Required Minimum Distributions (RMDs) must be taken from this account starting at age 73. However, when this time arises, you can roll it over into a Roth IRA account and free yourself from the RMD.

Scenario: Let’s assume again that your current salary is $200,000 and your employer offers a 100% match up to 5%. In this case the 5% or $10,000 that you contribute has already been taxed. This will not lower your W-2 wages and your gross income will show as $200,000. However, when you take a qualified distribution on this money, you will receive the amount in its entirety plus any growth and not be subject to tax. Your $10,000 employer match will be placed into a separate account and will be tax-deferred (as a Traditional 401(k) contribution).

Working in Tandem

It is possible to have both a Traditional and a Roth 401(k) and make contributions to both. If this is the case, the total contributions between the two cannot exceed the $22,500 limit ($30,000 if 50+). For instance, if you are 45 years old and contribute $18,000 in a Traditional you may only contribute another $4,500 in a Roth.

Using both accounts may make sense if you are unsure about whether your tax rate will rise or decrease in retirement. By using both accounts, you are diversifying your tax risk, paying some taxes now in order to make Roth 401(k) contributions, while waiting for retirement to pay the taxes on your Traditional 401(k) account distributions.

Source: IRS

If you are trying to decide between making contributions to a Traditional 401(k) or a Roth 401(k), we would encourage you to reach out to your advisor at Pekin Hardy Strauss for advice that is tailored to your specific situation.

For more insight on Retirement Plans and Planning read our previous Navigators from 2020 and 2019: A Retirement Planning Guide for High Net Worth Individuals and Qualified Retirement Plans: Big Benefits for Small Businesses.

The commentary in this video and article was prepared by Pekin Hardy Strauss, Inc. (“Pekin Hardy”, dba Pekin Hardy Strauss Wealth Management) for informational purposes only (and is not intended as an offer or solicitation for the purchase or sale of any security.) The information and data in this article and video do not constitute legal, tax, accounting, investment or other professional advice. The views expressed are those of the author(s) as of the date of publication of this report and video, and are subject to change at any time due to changes in market or economic conditions. The comments should not be construed as a recommendation of individual holdings, market sectors or any particular strategy, there is no guarantee that the strategies discussed herein will outperform any other. Although information has been obtained from and is based upon sources Pekin Hardy believes to be reliable, we do not guarantee its accuracy. There are no assurances that any predicted results will actually occur.