Low interest rates combined with massive changes in travel behavior during the COVID-19 pandemic are leading many people to acquire cars. Before making a significant financial commitment to a vehicle, it is important to understand the financing and leasing options that are available to you as a consumer to determine which is most advantageous. In this Navigator, we discuss car leasing and financing and compare the pros and cons of each strategy.

Buy Outright, Finance, or Lease? Considerations for Your Vehicle

A car is a common but significant purchase, and consumers may not be aware of all of their options when it comes to acquiring a vehicle. Different acquisition methods can lead to very different total costs and different car values remaining at the end of the payment period, so it is important to consider all of the alternatives available to you.

Purchasing a Car

Perhaps the most familiar way to acquire a vehicle is simply to purchase it, whether entirely in cash or with a combination of a cash down payment and a loan. Either way, purchasing a vehicle allows a consumer to build equity in that asset over time, leaving the consumer with full ownership at the end of any loan term. Unlike a home, vehicles are depreciating assets and wear and tear will lower its resale value, but it remains an asset that can be traded in or sold to help with the purchase of a future vehicle.

Buying Outright

Some consumers simply purchase a car outright in cash, and this is by far the simplest of the car purchase options. Without any interest paid, this is also likely to be the cheapest way to purchase a vehicle, and the buyer does not take on any financial risk associated with additional debt.

However, you may want to also consider the opportunity cost of the funds used to pay for the car. If the cash needed to purchase a vehicle would be coming from your investment portfolio, those assets would otherwise be expected to grow in value in your portfolio instead of being used to purchase a rapidly depreciating asset.

While this consideration is important no matter how you choose to purchase a vehicle, it is likely most important if you buy outright because you would be sacrificing investment growth on the largest number of up-front dollars instead of spreading it over many years with a loan or lease. If you are trying to keep your debt level in check or you have a sizeable investment portfolio and limited income, purchasing a car outright may be the best choice for you.

Financing

Especially in the current interest rate environment, financing can be an attractive option for those looking to make a purchase. Buyers make a down payment and then take out a loan for the remainder of the purchase price.

Monthly auto loan payments are calculated based on the sale price, the interest rate, and the term of the loan. These loans are available in 12-month increments and generally have terms of two to eight years. While it is certainly possible to get an eight-year term, potential purchasers should typically look at loan terms no longer than five or six years to keep the amount of interest paid to a reasonable level. Longer-term loans are also more likely to result in what is known as an “upside down loan,” which occurs when a vehicle depreciates faster than the loan is paid down. In this situation, the car is worth less than what is owed on it, which can become an issue if you need to trade in or sell the vehicle.

Financing a car only requires a down payment, typically between 10-20% of the purchase price. Monthly payments will typically be more expensive with a loan than with a lease, because you own a financed car at the end of the payment term whereas you must return a leased car. Nevertheless, the current low interest rate environment and flexible loan terms can still make monthly loan payments very affordable.

Leasing a Car

Leasing a vehicle is similar to renting an apartment: you lease a car from the dealer for some period of time (typically 36 or 48 months) without building up any equity in the vehicle through those payments. At the end of the lease term, you can either return the car to the dealer or purchase it at a predetermined amount. Some dealers may require a down payment on a lease that will lower the lease payment.

The major advantage to leasing is that the monthly payments are generally lower than the monthly loan payments would be for a similar car, since you only pay for the vehicle’s depreciation during the lease term plus an implied interest rate. Lease payments are calculated based on the sale price, the length of the lease, the expected annual mileage you will put on the car, a rent charge (essentially an interest charge), taxes and fees, and the residual value of the car. The residual value is the value of the depreciated vehicle at the end of the lease and reflects the value you would pay if you purchased the car at that point.

Leasing a vehicle has often been considered a poor financial decision because some drivers have used leasing as an opportunity to continually drive the newest car models, entering a cycle of constant lease payments without ever owning a vehicle. But with low interest rates and leasing options expanded beyond just the newest or luxury models of cars, leasing has become an attractive option for more consumers, especially those who may just need a car for a few years or who want the lowest upfront payments with the ability to purchase the car at the end of the lease.

That said, leasing a vehicle does have limitations that make it impractical for some consumers. Most leases limit the number of miles you can drive during the lease term, typically 12,000 to 15,000 per year. Drivers who need to exceed the number of miles in the contract will have to pay a fee (typically on the order of 15 to 20 cents per mile in excess of the contractual mileage). Drivers who put more than the usual wear and tear on the car or who make any modifications will also have to pay to repair or to remove the customizations before it is returned.

If your car is used for work purposes, you may be able to deduct the cost of the lease off of your corporate tax return, and this deduction can be scaled to usage: if you use the car for work 50% of the time, then you may be able to deduct 50% of your lease payments. As for financed vehicles, the tax rules offer a choice of vehicle expense deduction methods, and if you itemize the vehicle expenses, a portion of a payment can often be used as a business expense. A regular vehicle loan payment is not a deductible expense.

One further important consideration in leasing a car is that ending a lease early can be as costly as the contract itself. While a purchased or financed car could be sold or traded in at any time, even early in the loan term, ending a lease early may require you to pay significant charges. If you think your need for a vehicle may change over the term of a loan or a lease, you may be better off financing the vehicle to give yourself more flexibility.

Comparison

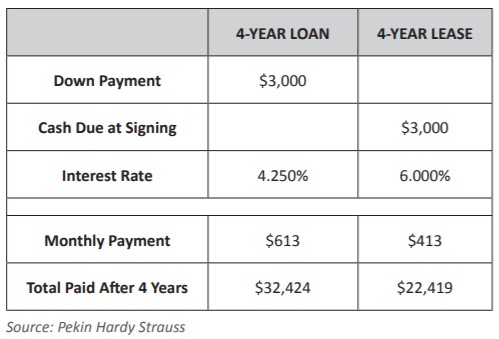

There are many qualitative differences between buying and leasing a car as outlined above, but the quantitative differences will depend on many factors like the type of car, the amount of the up-front payment, and more. The table below shows a simple comparison between financing and leasing a vehicle to illustrate the financial difference between the two. This comparison assumes the car being financed or leased costs $30,000 with a required $3,000 payment up front, whether as a down payment on a loan or upfront costs on a lease. Both are assumed to have four-year terms.

In this example, the lessee is paying a higher interest rate than the buyer. While this will not be true in every situation, interest rates on leases are generally higher than interest rates on loans. A buyer with excellent credit may be able to get as low as 0% financing on an auto loan, whereas a lessee with excellent credit would still expect to pay a more significant rate.

As is evident above, leasing a car can lead to significantly lower monthly costs, but of course the lessee does not own a vehicle at the end of the four-year term, and the driver is limited in the number of miles he or she can drive during the term.

As is the case with most financial topics, the “right way” to purchase a vehicle depends upon your personal needs and means. If you are in the market for a vehicle, we would encourage you to reach out to your Pekin Hardy Strauss portfolio manager to discuss the best strategy for you.

This article is prepared by Pekin Hardy Strauss, Inc. (“Pekin Hardy”, dba Pekin Hardy Strauss Wealth Management) for informational purposes only and is not intended as an offer or solicitation for business. The information and data in this article does not constitute legal, tax, accounting, investment or other professional advice. The views expressed are those of the author(s) as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. Pekin Hardy cannot assure that the strategies discussed herein will outperform any other strategy in the future, there are no assurances that any predicted results will actually occur.