Life insurance can be a highly effective risk management tool that should have a place in most Americans’ comprehensive financial plans, but life insurance products should not be viewed as investments for a number of reasons. For most people, a term life insurance policy should provide cost-effective protection against the financial repercussions of the untimely demise of a family member while leaving the policyholder free to invest his or her capital in suitable investments.

As financial products go, few are more ubiquitous in the typical American’s financial plan than life insurance. According to the Life Insurance Market Research Association (LIMRA), approximately 70% of the American population has some form of life insurance coverage, whether as an individual or as part of employer-provided group coverage.

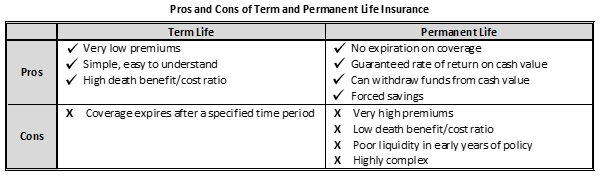

Practically all life insurance policies fall into one of two main categories: term and permanent. Both types of coverage oblige the insurance company to pay a predetermined sum to a policyholder’s beneficiaries upon the policyholder’s demise. Broadly speaking, in the case of term insurance, this promise is only valid for a specified period of time (hence the moniker “term”), whereas a permanent life insurance policy will pay regardless of when the policyholder’s death occurs.

The purpose of this Navigator is to discuss how term and permanent life insurance policies work, as well as some of the benefits and drawbacks of each.

What is Term Life Insurance?

Source: Gaudette Insurance

Term life insurance is a very common and relatively simple financial product with which many Americans are likely familiar. But exactly how does term life insurance work? In a typical term life insurance policy, the policyholder pays a fixed premium for a specified period of time in exchange for a guarantee that, should the policyholder die during the relevant period, the face value of the policy will be paid to the policyholder’s beneficiaries in a tax-free manner. Once the policy term has ended, the insurance company no longer has any obligation to the policyholder, and the policyholder must either obtain new coverage (likely at an increased premium) or simply forego coverage for the remainder of his or her life. Should the policyholder’s death occur after coverage has ceased, no death benefit will be paid to the policyholder’s beneficiaries.

Because of its limited guarantee, term life insurance is generally the least expensive way to obtain substantial protection against untimely death. Also, because term policies have no permanent cash value, they are not typically used for estate planning purposes but, rather, act as pure risk management tools, replacing the future income of a deceased policyholder. Because of its affordable cost, term life insurance is a particularly effective risk management tool; those people with young children or spouses with limited employment income should seriously consider obtaining term life insurance coverage.

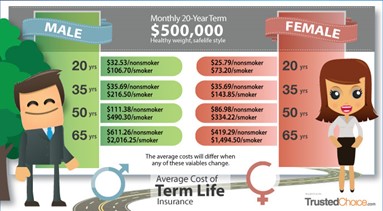

As income replacement tools, most term policies should be structured to expire around the time that the policyholder’s employment income is no longer necessary. When a policyholder reaches the point at which he or she no longer has anyone depending upon his or her employment income (such as young children or a non-income-producing spouse), there is often little need for the protection offered by life insurance. Term insurance gives policyholders the ability to purchase coverage for just the specific period of time over which it may be needed. In the United States, 20-year term life insurance policies are the most commonly purchased policies, while 10-year and 30-year term life insurance policies are also popular.1

Permanent Life Insurance

Permanent life insurance is another highly common financial product in the United States, but it is considerably more complex than term life insurance. So how does permanent life insurance work? That depends on the policy. There are several different types of permanent life insurance policies that all have different moving parts. However, they do all share one primary characteristic, as noted above: the guarantee of a death benefit, regardless of when the policyholder’s death occurs. Beyond this one key characteristic, there are a multitude of variations of permanent life insurance. Understanding these different types of policies is important when discussing permanent life insurance pros and cons, as the benefits and drawbacks may differ by policy type. Below we delve into the most common types of permanent life insurance.

Whole Life Insurance:

Source: Gaudette Insurance

Basic whole life insurance has two primary components: a death benefit and a cash value. As previously highlighted, the death benefit is the face value of the insurance contract that is paid to the policyholder’s beneficiaries upon the policyholder’s death (this amount may be adjusted up or down, depending on a few factors discussed below). The cash value of the contract, on the other hand, is a sort of savings vehicle that accrues over time as premiums are paid.

Building cash value in a whole life insurance policy is somewhat analogous to building equity in a home. Just as a portion of each mortgage payment made for a home is allocated to paying the principal of the loan, increasing the homeowner’s equity, a portion of each premium paid for a whole life insurance policy is allocated to the cash value component, increasing its value over time. Whole life insurance premiums are allocated into three primary buckets:

- Actual Insurance Costs

This is the cost of insuring against the policyholder’s death. This portion of the premium goes toward covering the eventual liability of paying the policy’s beneficiaries upon the demise of the policyholder.

– - Operating costs and profit of the insurance company

Part of a policy’s premiums is designated towards helping the insurance company cover its operating costs and the costs to administer the policy. The insurance company’s profit and the insurance agent’s commission are funded by this portion of the premium.

– - Cash Value

Part of a policy’s premiums is designated towards helping the insurance company cover its operating costs and the costs to administer the policy. The insurance company’s profit and the insurance agent’s commission are funded by this portion of the premium.

While the bulk of a policy’s cash value is derived from premium payments, cash values may be further increased through interest that the insurance company pays on the cash value. As premiums are paid into a whole life policy, the insurance company theoretically invests the cash value portion of the premium payments into conservative investments (primarily fixed income). Some of the interest that is earned on those investments is added to the cash value of the contract, and some of the interest is kept by the insurance company as profit. The rate of interest that is paid on the cash value of a contract is generally guaranteed and is determined by the insurance company upon policy commencement using a number of actuarial assumptions, including an assumed forward-looking rate of return on the insurance company’s investment portfolio. Oftentimes, this guaranteed rate of return comes with a cap on the potential rate of return achievable.2 Certain policies contain riders that allow for a greater rate of interest to be paid on cash value when investment returns exceed the company’s assumptions. However, even in those cases, the insurance company is only obligated to pay the minimum rate as stipulated in the policy contract.3 Some policies, referred to as “participating” policies, may also receive dividends that are added to the policy’s death benefit in years during which the company pays out fewer claims than expected.

The owner of a whole life insurance policy may take funds from the cash value of his or her policy, either as a withdrawal or as a low-interest rate loan. Proceeds from withdrawals and loans taken against a policy are not taxed unless they exceed the total premiums paid into the policy (i.e. if the policyholder withdraws any of the gains that have accrued in the cash value due to interest). Any funds taken out of cash value that exceed the policyholder’s basis are taxed at ordinary income tax rates. If there are any outstanding loans on a policy at the time of the policyholder’s death, the loan amount (plus interest) is subtracted from the death benefit that is paid to the policyholder’s beneficiaries. Withdrawals may also reduce the policy’s death benefit or cause the policy’s premiums to increase in order to maintain the death benefit.

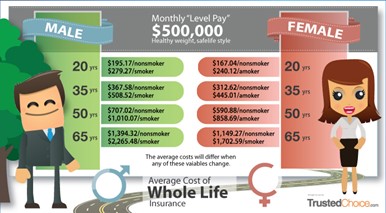

Whole life insurance premiums are set at the time of purchase and remain constant throughout the life of the contract. In most cases, this period represents the lifetime of the policyholder. However, certain policies are set up as “limited pay” contracts, meaning that all premiums will be paid over a set number of years (often 10 or 20). Other policies may also be paid entirely in one lump sum at the time of purchase.

Relative to term insurance, whole life insurance premiums are extremely high. There are three reasons for this price disparity:

- The cost to insure the policyholder is considerably greater, owing to the fact that the policy must cover the insured for his or her entire life. This means, barring unusual circumstances, the policy will pay a death benefit at some point in time. This is in contrast to term insurance, where a death benefit will only be paid if the policyholder’s death occurs during the effective term of the contract.

– - Part of the premium goes toward accumulating the contract’s cash value, which does not exist in a term contract.

– - Part of a policy’s premiums is designated towards helping the insurance company cover its operating costs and the costs to administer the policy. The insurance company’s profit and the insurance agent’s commission are funded by this portion of the premium.

It should be noted that many cash-value life insurance policies (whole, universal, variable, etc.) do not begin to build cash value right away. In many cases, a policy must be in force for a certain period of time before cash value begins to accrue, and it may take many years for the cash value to surpass the total amount of premiums paid into the policy. This is an important point to consider, given that nearly 30% of all permanent life insurance policies sold in the United States lapse within the first three years of the policy.4 Policyholders who let their policies lapse in these early years often receive little or nothing from their policies, despite having paid material premiums. This fact makes cash-value life insurance products a poor source of liquidity in the early years of a policy.

Similar to term insurance, whole life insurance can serve a number of different purposes, including as a source of retirement income, to pay for funeral expenses, to replace the income of a deceased wage-earner, and/or to protect against key person risk for a business. Historically, whole life insurance was more widely used to avoid estate taxes for inheritances, due to the fact that death benefits are tax free¬. However, as a result of the substantial increase in the Federal estate tax exemption (which now sits at $12.92 million, per person, or $25.84 million for a married couple), permanent life insurance tax benefits have decreased considerably, and these types of policies have become less useful for estate planning purposes, except for those investors who have very large estates or for those who have taxable and largely illiquid estates.

Universal Life:

Universal Life (UL) insurance is similar to whole life insurance in many ways. Because it is a form of permanent life insurance, it pays a death benefit no matter when the policyholder dies. And, like whole life insurance, it includes a cash value component. However, some key differences set universal life insurance apart from whole life insurance.

Universal life insurance evolved out of whole life insurance in order to give policyholders more flexibility with regard to the cost and benefits of their policies. While universal life has a cash value component much like whole life, a universal life policy essentially allows a policyholder to determine how much cash value he or she builds. While whole life insurance policies have set premiums and a predetermined breakdown of those premiums between insurance costs, cash value, and administrative expenses, universal life actually allows a policyholder to vary the premiums that he or she pays and to control (to an extent) the rate of cash value accumulation. While the optionality of this product can be useful, it comes at a high financial cost.

The primary variants of universal life insurance are described below:

- Variable Universal Life

(VUL) is a type of universal life insurance that shares most of the characteristics of standard universal life insurance. However, it differs in the way that the cash value is treated. While cash value in a standard UL policy grows according to prevailing market rates of return and typically includes a minimum guaranteed rate, VUL cash values are tied to the performance of various investment subaccounts. These subaccounts consist of pooled capital that is invested in stocks and bonds, similar to mutual funds. These subaccounts typically offer greater potential for cash value growth than standard UL policies, but because cash values are not guaranteed in VUL policies, there may be a greater risk since the cash value could actually decline. At the same time, such products typically do not have a cap on investment returns.

– - Index Universal Life

(IUL) is structured very similarly to variable universal life except that instead of tying cash values to the performance of investment subaccounts, cash values are tied to the performance of an equity market index, such as the S&P 500 Index. However, unlike VUL, IUL policies typically have principal protection on cash values, meaning that they will not decline in value when the index to which they are tied declines. On the flip side, there likely will be a cap on the rate of return that is earned by the cash value in an IUL policy. This could limit the growth of the cash value in years in which the underlying index does especially well and puts into question the value of the floor rate of return.

Generally speaking, permanent insurance is designed to accommodate unique estate planning needs, such as minimization of estate taxes on very large inheritances and limiting risk from creditors. However, it is generally not well-suited as an investment vehicle for most people because of its high fee structure, low returns relative to commensurate market-based vehicles, and surprisingly poor liquidity. For this reason, in our estimation, permanent insurance is suitable for a small subset of people who have these specific needs and who have no intention of relying on the policy as an investment.

Term Vs. Permanent Life Insurance

While investors may be attracted to permanent life insurance policies because of the cash value component, it is important to understand that cash value in a permanent policy may not provide the liquidity and investment return that the policyholder desires. As discussed, a policyholder’s premium payment is split into three parts: cost of insurance, cash value, and administrative/operating costs. Term policies also include an administrative/operating cost element, but at much lower levels than permanent life insurance policies. This disparity exists because of the relative simplicity of term insurance. The administrative costs of permanent policies can eat up a material portion of a policyholder’s premium, leaving less available for cash value accumulation. These higher administrative costs explain why it may take decades for the cash value of a policy to surpass the total amount of premiums paid into the policy.

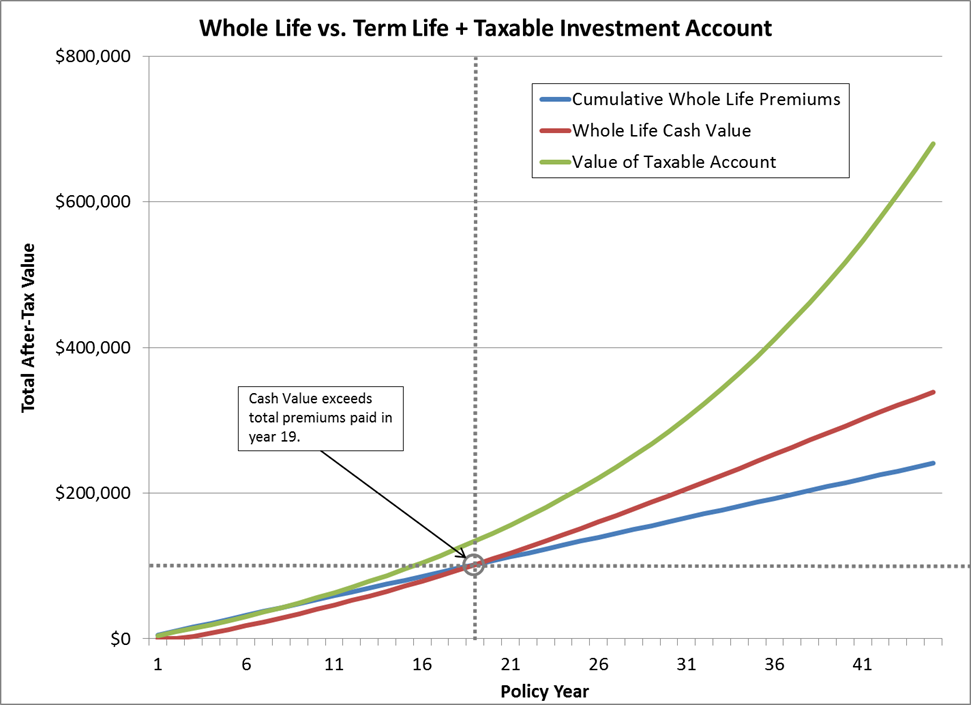

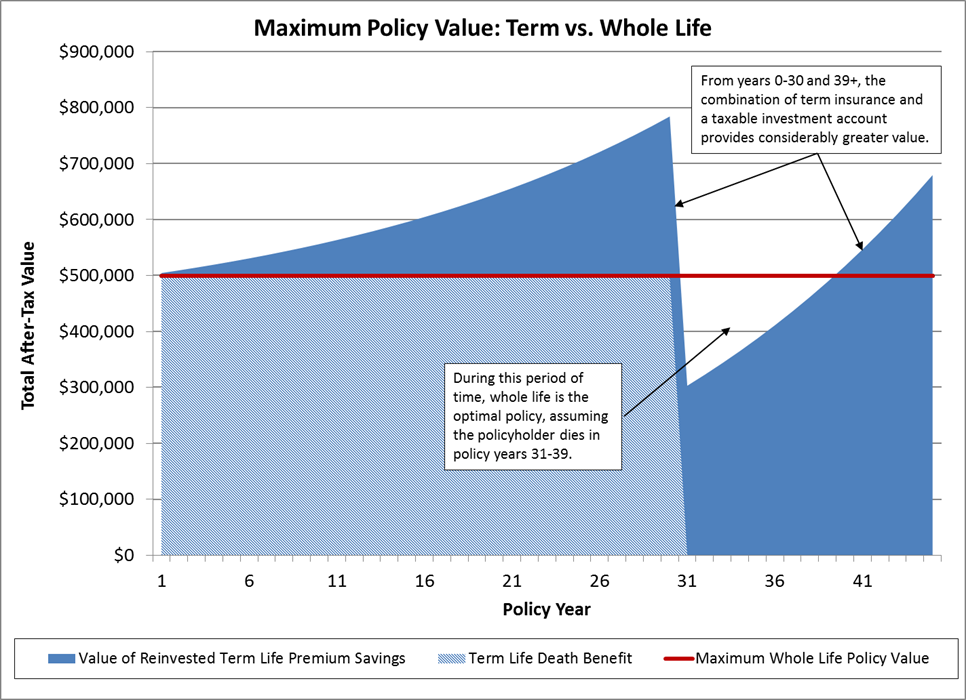

The following chart helps to illustrate this disparity. In both the whole life and term insurance examples, the death benefit is the same ($500,000 in this case). Our example assumes that the investor takes the difference between the greater whole life insurance premium and the lesser term life insurance premium and invests the capital in a taxable investment account. By a large margin, the investor who wants both 1) $500,000 of life insurance coverage, and 2) to maximize the value of his/her asset base would be better off purchasing term insurance and deploying the excess capital in a taxable investment account. We assume that this taxable account grows at an after-tax rate of 4.65%.5

In addition to illustrating the disparity between whole life cash value growth and the growth of a taxable investment account, the above example also highlights the fact that the cash value of many whole life policies does not exceed the total premiums paid into the policy for a number of years. In this example, the cash value of the whole life insurance policy does not exceed the total premiums paid until the 19th year of the policy. This is because a material portion of the premiums that are paid into the policy are going towards the administrative costs of the offering company.

The maximum value that a policyholder can receive from this whole life policy is very unlikely to ever exceed the face value of the policy, which in this case is $500,000. The term policy would provide the same $500,000 death benefit for 30 years, plus the additional capital that has accumulated in the taxable investment account. The term policy death benefit would drop to $0 after the 30-year term, but in this illustration, the taxable account would have a value of $302,000 at that time and would surpass $500,000 nine years later, when the policyholder is age 75. This is illustrated in the chart below, in which we show the maximum possible value that a policyholder’s beneficiaries would receive from each type of policy in the event of the policyholder’s death. As the chart clearly indicates, the term life policy would provide a policyholder’s beneficiaries with a materially greater benefit, assuming that death actually occurs, in every year except during a span of nine years, given our return and tax assumptions that are conservatively based on historic averages.

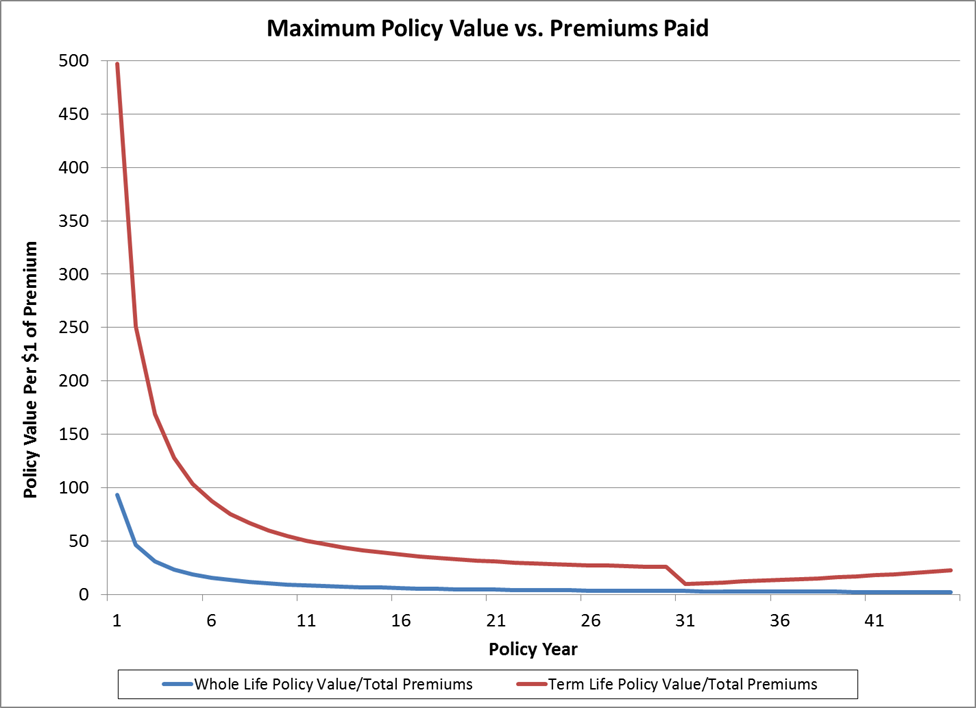

Term Insurance is a Far More Attractive Risk Mitigation Tool than Whole Life Insurance

In addition to providing the greater maximum benefit throughout the majority of a policyholder’s life, the term policy also provides the greatest benefit per dollar of premium, as the chart below illustrates.

It is also important to understand that insurance agents have a strong incentive to sell permanent life insurance products as opposed to term insurance products because of the commission structure associated with each product. As noted previously, agents who sell permanent life insurance products receive very large commissions on whole life policies. The sale of a term insurance policy, on the other hand, will typically result in a commission that is only a small fraction of what the agent would earn on the sale of a comparable whole life policy.6 This commission structure is heavily skewed toward permanent life insurance products, and therefore strongly encourages agents to sell these types of products, regardless of suitability to the client.

For most Americans with more typical insurance needs, such as replacing the income of a deceased wage-earner, term insurance typically is the most suitable life insurance product. Given the simplicity of term insurance and its substantially lower premium structure, term insurance offers the most protection for the lowest cost (over the relevant term, of course). By purchasing a policy with a lower premium, a policyholder’s incremental capital is free to be invested in whatever way he or she sees fit. This means that the policyholder can put this capital to work in ways that could potentially earn meaningfully higher returns than might be offered on the cash value of a permanent insurance policy while also enjoying far greater liquidity.

Final Thoughts

Life insurance can be a very effective risk management tool that can and should play an important role in most Americans’ comprehensive financial plans. However, life insurance is surprisingly complex, and insurance needs tend to be very unique to each individual. It is for this reason that we strongly encourage clients to discuss their insurance needs with us before purchasing a policy so that we can help them fully understand the policy, its pros and cons, and its suitability to the client’s personal situation. While we do not sell insurance products, as our clients’ trusted advisors we believe it is our duty to help our clients find the optimal financial products that make up their comprehensive financial plans.

As always, if you have any questions about life insurance or need help figuring out the right type of insurance for your needs, please do not hesitate to reach out to us.

1 https://www.forbes.com/advisor/life-insurance/choosing-the-right-term-life-insurance/

2 It should be noted that this “guaranteed” rate of return is typically a low return hurdle in comparison to historic rates of returns, and the insurance company feels reasonably comfortable about generating that sort of return over a multi-year period.

3 Because the guaranteed interest rate that an insurance company agrees to pay on a policy’s cash value is determined at the policy’s inception, the performance of a policy’s cash value over the life of the policy is largely a matter of timing. The cash value of a policy which is initiated when prevailing market interest rates are higher is likely to outperform the cash value of a policy which is initiated when interest rates are lower, all else equal.

4 https://www.forbes.com/advisor/life-insurance/best-whole-life-insurance/

5 See Appendix for return calculations and other assumptions.

6 https://lsminsurance.ca/life-insurance-canada/2013/08/are-life-insurance-commissions-on-their-way-out

The commentary in this video and article was prepared by Pekin Hardy Strauss, Inc. (“Pekin Hardy”, dba Pekin Hardy Strauss Wealth Management) for informational purposes only (and is not intended as an offer or solicitation for the purchase or sale of any security.) The information and data in this article and video do not constitute legal, tax, accounting, investment or other professional advice. The views expressed are those of the author(s) as of the date of publication of this report and video, and are subject to change at any time due to changes in market or economic conditions. The comments should not be construed as a recommendation of individual holdings, market sectors or any particular strategy, there is no guarantee that the strategies discussed herein will outperform any other. Although information has been obtained from and is based upon sources Pekin Hardy believes to be reliable, we do not guarantee its accuracy. There are no assurances that any predicted results will actually occur.

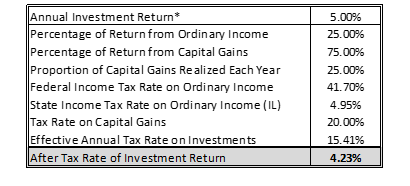

* The Annual Investment Return assumption is based on a 60% / 40%

allocation to equities and fixed income securities. Over a long period of time,

the S&P 500 has generated an average annual rate of return of roughly 10%

per year, while the bond market has generated an average annual rate of

return of roughly 5% per year. However, for the sake of conservatism, we

have assumed an equity return of 6.0% per year and a bond return of 3.5%

per year. With a 60/40 allocation, this would generate a 5.0% annual pre-tax

return.