For many Americans, their home is their single largest investment, usually representing a major proportion of their net worth. Given that homes typically sell for several times a buyer’s annual income, the majority of homebuyers borrow the bulk of the money needed to buy a home and then spend the majority of their working lives paying the money back, along with substantial amounts of interest. In this Navigator, we discuss the most common mortgage types and their defining characteristics in order to help readers, especially those who are less familiar with the mortgage market, better understand these products; we follow this with an examination of some key mortgage questions and considerations that homeowners or potential homeowners may face.

Making the Most of Your Mortgage

Owning a home is often considered to be a key cornerstone of the American Dream. However, few Americans have the capital necessary to purchase a home without the support of a mortgage, especially in their early adult years when most homeowners buy their first home. Mortgage loans provide buyers with supplemental funds necessary to purchase a home, which they then repay, along with interest, over a multi-year period. Approximately 86% of U.S. home purchases are made with a mortgage, and 63% of all U.S. homeowners have a mortgage. In total, U.S. homeowners carry approximately $10.3 trillion in mortgage debt, accounting for roughly two-thirds of all household debt. Purchasing a home and entering into a mortgage contract.

Types of Mortgages

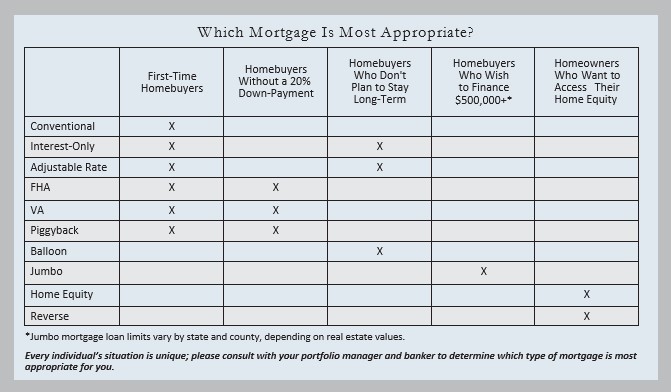

Given the magnitude of the impact that mortgages can have on one’s finances, it is important to have a clear understanding of the different types of mortgages available in the market and how they are structured. While mortgages are extremely common in the United States, not all mortgages are the same. In fact, there is a vast array of different types of mortgages with varying repayment structures, term lengths, interest rates, and other variables. Provided below is a list of some of the most common types of mortgages, along with a brief discussion of their primary characteristics.

Conventional Mortgage

A conventional or fixed rate mortgage is an amortizing mortgage with a fixed interest rate that does not change during the term of the loan. It is available through or guaranteed by a private lender or the two government sponsored enterprises, Fannie Mae and Freddie Mac. The most common type of mortgage, conventional mortgages typically have terms of 15, 20, or 30 years. Because the interest rates on conventional mortgages do not change, the required monthly payments do not change during the life of the loan. To qualify for a conventional mortgage, homebuyers must typically make a down payment of at least 20% of the home’s purchase price. Buyers who cannot meet the 20% down payment threshold may still be able to secure a conventional mortgage by purchasing private mortgage insurance (PMI), which reduces the risk faced by the lender.1

Interest-Only Mortgage

Interest-only mortgages, as their name suggests, carry provisions that allow (but do not require) homebuyers to pay only the interest on the loan for a period of time (typically the first five or 10 years of the loan term) while leaving the principal unchanged. Typically, after the interest- only period is over, the principal begins to amortize just like a conventional mortgage. Because interest-only mortgages allow homebuyers to make smaller monthly payments during the interest-only period, they are often used by first-time homebuyers who may benefit from the flexibility of lower payments in the earlier years of a mortgage. This type of mortgage is also often used by speculators who believe a home’s value is likely to rise materially during the interest-only period. Plus, the average homeowner stays in their home for 13 years, so, if one is thinking about moving sooner rather than later, interest-only mortgages may be more appropriate.

Adjustable Rate Mortgage (ARM)

There are many different variations of adjustable rate mortgages, but, in general, these loans are characterized by a fixed interest rate term followed by a floating interest rate term. A common example of an adjustable rate mortgage is the 10/1 ARM. Homebuyers who opt for this type of mortgage would pay a fixed interest rate for the first 10 years of the loan term (typically 30 years), after which time the interest rate would be free to change on an annual basis, depending upon the movement of some underlying benchmark rate (e.g., LIBOR). The interest rate for the fixed term portion of an ARM is typically lower than the rate that could be had with a conventional mortgage due to the fact that buyers are assuming the risk that rates might increase later in the life of the loan. Homebuyers who believe that rates are likely to fall or who do not expect to own the property beyond the fixed interest rate term may want to consider an ARM as a way to reduce interest costs.

FHA Loan

FHA loans are mortgages that are insured by the Federal Housing Administration, which is the largest insurer of residential mortgages in the world. Borrowers who qualify for an FHA loan may purchase a home with as little as 3.5% down and enjoy low fixed interest rates. Buyers must pay an annual mortgage insurance premium (MIP) in order to qualify for the lower down payments offered by FHA loans. FHA loans are quite popular with first-time homebuyers who do not have enough capital for a large down payment. In order to qualify for an FHA loan, a borrower must have a FICO score of at least 580 and a debt-to-income ratio of less than 43%, the borrower must have steady income and proof of employment, and the home must be the borrower’s primary residence.

VA Loan

Similar to FHA loans, VA loans are backed by the Federal government, specifically the Department of Veteran Affairs. VA loans are designed to make it easier for members of the U.S. armed forces (and sometimes their spouses) to purchase homes. VA loans do not require a down payment, and loan rates are typically very competitive. However, in order to enjoy these benefits, borrowers must meet specific military service-related requirements.

Piggyback Loan

Homebuyers who cannot make a 20% down payment when purchasing a home and who do not qualify for other programs which allow smaller down payments can either purchase private mortgage insurance (PMI) or opt for a piggyback loan (also called a “combo loan” or “second trust loan”). A piggyback loan consists of two loans taken simultaneously: one for 80% of the home’s purchase price, and the other for whatever portion of the 20% down payment the borrower cannot cover with cash. The most common type of piggyback loan is an 80/10/10 loan, which consists of one loan covering 80% of the purchase price, a second loan covering 10% of the purchase price, and finally a 10% down payment. The interest rate on the second loan is typically higher than that of the first loan. The second loan will typically also carry its own closing costs, increasing a borrower’s upfront cash requirements. However, the combined monthly costs of a piggyback loan are typically lower than they would be if the borrower had to pay PMI.

Balloon Mortgage

A balloon mortgage is structured as a standard fixed rate, amortizing loan for a set period of time (typically five or 10 years). Then, at the end of this time period, the entire remaining principal is due in one lump sum payment. Balloon mortgages typically carry lower interest rates than would be available on conventional mortgages, making them an attractive option for some borrowers. However, this type of mortgage can be quite risky and is typically only appropriate under specific circumstances. Buyers who are highly confident that they will no longer own the property when the balloon payment comes due or who believe that they will be able to refinance the loan before the balloon payment comes due may want to consider this type of mortgage.

Jumbo Mortgage

Large mortgages which exceed the limits established by the Federal Housing Finance Authority (FHFA) are called jumbo mortgages. These mortgages cannot be purchased, guaranteed, or securitized by Fannie Mae or Freddie Mac, making them somewhat riskier for lenders. Jumbo mortgages are typically used to finance the purchase of luxury homes or properties in expensive real estate markets. This type of mortgage carries unique underwriting requirements and receives different tax treatment than conventional mortgages. FHFA limits for conforming loans (mortgages which can be purchased, guaranteed, or securitized by Fannie Mae or Freddie Mac) vary by location in order to reflect the differences in real estate markets. For most of the country, the mortgage limit is $453,100, though for counties with higher real estate values, the limit can be as high as $726,525. Because jumbo mortgages are riskier for lenders, qualifications are much more stringent than for conforming loans (e.g., exemplary FICO scores, very low debt-to-income ratios) and interest rates are typically somewhat higher than rates on conforming loans.

Home Equity Loan

Homeowners who have accumulated significant equity in their homes and who wish to access some of that equity may consider a home equity loan, which is often simply referred to as a second mortgage. Home equity loans are generally structured in much the same way as traditional fixed-rate mortgages: they are typically amortizing, fixed-rate loans with set term lengths and which are secured by the same property as the primary mortgage.2 In most cases, the only significant difference is that home equity loans tend to carry higher interest rates than primary mortgages in order to reflect the increased risk borne by the lender.

Reverse Mortgage

A reverse mortgage is a very different animal from the other mortgage types described above. Standard mortgages are structured such that the bank provides a lump sum to the borrower in order to purchase a home, and then the borrower repays the lender over time, accumulating equity along the way. However, in the case of a reverse mortgage, the lender actually makes payments to the borrower, reducing the homeowner’s equity over time, and then ultimately recoups the principal, interest, and fees when the home is sold or the homeowner dies. Reverse mortgages are only available to homeowners who are at least 62 years old and who have more than 50% equity in their homes based on current value. Proceeds from a reverse mortgage can be paid in a lump sum, a specific number of payments, or as a lifetime annuity. Interest on the loan amount accumulates over time (along with various fees) and is rolled into the total loan amount. In most cases, the loan is extinguished by selling the home after the death of the homeowner, though a deceased homeowner’s heirs do have the option of paying off the loan through other means in order to keep the property. Except in the case of lump sum payouts, interest rates on reverse mortgages are variable and are typically tied to LIBOR or a similar benchmark rate.

Key Mortgage Questions

While it is important to understand the different types of mortgage loans available in the market and who might want to consider each, there are many important questions that homebuyers or homeowners often have, aside from which type of mortgage is most suitable. Below, we address some of the most common mortgage-related questions and provide some insight into how borrowers might want to think about these questions.

1. How much can I afford?

Probably the most important question that homebuyers must consider is how much to spend on a home. There are varying points of view on this question, and the answer no doubt depends on the unique financial circumstances of the buyer. However, as a general guideline (and assuming a 20% down payment), we typically recommend that homebuyers scale the size of their home purchase such that their monthly mortgage payment (principal and interest only) does not exceed 25% of their monthly after-tax income. Of course, there are other costs that homebuyers must consider as well, such as insurance, property taxes, and in some cases, HOA fees. Taking all of this into account, we suggest that homebuyers try to keep their total monthly housing costs below 30% of their monthly after-tax income. Again, this is a general rule, and we understand that each situation is unique. There may be cases where exceeding these limits is perfectly acceptable, and there may also be cases where buyers should aim to keep costs much lower than these limits.

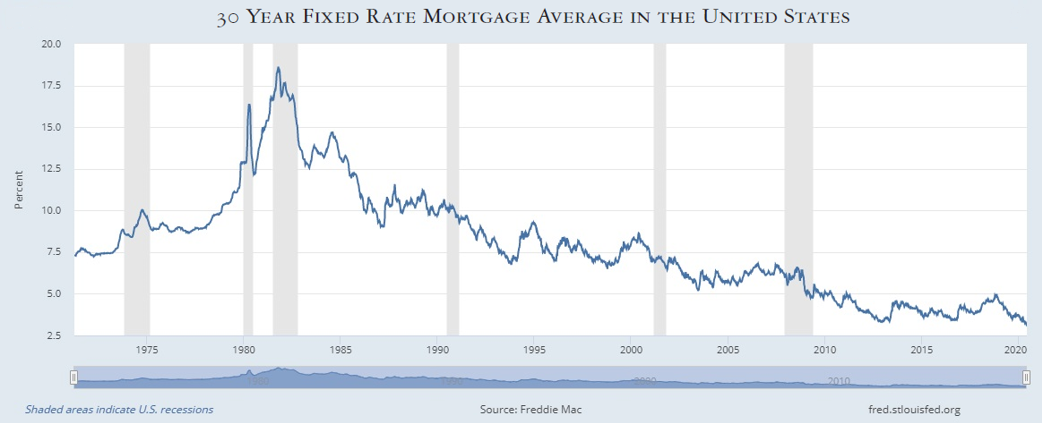

2. Should I refinance my mortgage?

For nearly 40 years, mortgage interest rates have been in a downward trend, as shown in the chart below. As interestrates fall, borrowers may want to consider refinancing their mortgages at the new lower rates. This can often be a very good idea, as it can lower monthly payments as well as the total cost of the mortgage. However, there are a few points to consider aside from just the interest rate.

- In order to determine if refinancing does, in fact, make sense, borrowers must be aware of all costs associated with the refinancing. Refinancing will often require that an appraisal be done on the property at the expense of the owner.

- Refinancing may carry loan closing costs that must be borne by the borrower, and in many cases, borrowers are required to pay points in order to obtain the lowest interest rates.3

- Extending the loan term on a refinanced mortgage can reduce monthly payments, but it can increase the total cost of the mortgage.

- If the remaining term on your existing loan is limited, lowering your interest rate may not help much financially unless you are trying to take cash out of your home.

All of these factors, along with the borrower’s expectation regarding the length of time he or she plans to stay in the home, must be considered in order to determine whether or not refinancing is the optimal strategy.

3. Should I pay ahead on my mortgage?

This is a common mortgage question, but it is one that can be difficult to answer because there is no hard and fast rule. Nearly all mortgages are free of pre-payment penalties, so paying ahead on a mortgage can be a great way to reduce the overall cost of the loan (i.e., pay less in total interest) and accumulate equity at an accelerated rate. It also provides homeowners with greater flexibility and control over their payments than reducing the loan term (e.g., going from a 30 year mortgage to a 20 year mortgage), as homeowners can simply suspend making extra principal payments whenever they deem necessary. However, while paying ahead on a mortgage has substantial benefits, one must consider the opportunity costs associated with the extra principal payments. Any principal payments made above what is required will effectively earn a “return” equal to the tax-effected interest rate on the mortgage.4 Given that mortgage rates are very low by historical standards, it is possible that homeowners may have other long-term investment opportunities available to them which could earn a return greater than the tax-effected interest rate on their mortgage. If this is the case, the optimal strategy is to pay the minimum mortgage payment and invest any excess capital in the alternate investment. This is all to say that the answer to this question is very situation-specific; if you are contemplating this strategy, please consider discussing it with us so that we can help you make the best decision for your individual circumstances.

4. Should I have a mortgage if I’m retired?

Like so many personal finance questions, this one is very situation-dependent, and it is not true that a person absolutely shouldn’t have a mortgage if he or she is retired. Many pundits advise homeowners to extinguish their mortgage debt prior to retirement and certainly many retirees do own their homes free and clear of debt, but this does not mean it is necessarily bad to carry a mortgage into retirement. Given that interest rates remain low (and mortgage interest is usually tax-deductible), mortgages can be a relatively inexpensive way for retirees to maintain a higher level of liquidity. Instead of allocating a large portion of one’s savings toward eliminating mortgage debt, retirees have the option of continuing to carry a mortgage and thus leaving their liquid capital unencumbered so that it can be used for living expenses. This strategy may be appropriate for some retirees and less so for others, but it is something that retirees can consider if they believe their liquidity may otherwise be limited.

5. Should I consider a reverse mortgage?

Reverse mortgages have been maligned in the media in recent years because they have been used by unscrupulous individuals to defraud and scam elderly homeowners. However, they have very legitimate uses and can be highly effective tools under the right circumstances. A reverse mortgage may be appropriate for an older homeowner who has accumulated significant home equity but who does not have sufficient liquidity for meeting normal living expenses. Retired homeowners whose cash and liquid investments have been exhausted may find that a reverse mortgage provides an effective means for accessing their home equity to cover living expenses without having to sell the home. However, a reverse mortgage generally should only be considered as a sort of “last resort” option for generating liquidity, as the interest and other costs associated with such products can be substantial.

Our discussion of mortgages and related questions has been far from exhaustive. Homeowners and home buyers often face all sorts of complex questions and issues related to mortgages aside from those that we have covered above. If you are a homeowner or are considering becoming a homeowner and you have any questions about mortgages, please reach out to your portfolio manager to discuss the best strategy for your circumstances.

ss to tolerate risk. The ability to tolerate risk is determined by an investor’s age, income, expenses, asset base, and a number of other concrete factors. It is an objective assessment of how much volatility an investor should tolerate in order to achieve his or her financial goals. The willingness to tolerate risk, on the other hand, is a subjective assessment of an investor’s psychological and emotional ability to cope with asset price volatility. This second part of the risk tolerance equation is where problems typically arise. Oftentimes, investors believe their willingness to tolerate risk is greater than it really is, and it is only in times of market turmoil that their true willingness to tolerate risk is revealed. These investors can only deal with upward price volatility. The recent volatility in the capital markets has likely revealed such a mismatch for many investors.

The intensity of the recent market sell-off was enough to shake even the most hardened market veterans. As an investor, it was nearly impossible to watch the market’s violent moves without experiencing some stress. However, while some degree of concern was warranted, investors whose asset allocations were appropriate for their individual risk tolerances should still have been able to sleep at night, despite Mr. Market’s spasms. Unfortunately, many investors likely found themselves worrying about their mounting portfolio losses over the past few weeks. If you fall into this camp, you should revisit your asset allocation and consider making changes so that your allocations properly align with your risk tolerance.

Review Your Financial Plan

One of the best ways to ease an anxious mind during economic and market upheaval is to create a financial plan or review your existing plan to ensure that it is complete and up to date. Though financial market performance typically commands the bulk of investors’ attention, we believe that having a sound financial plan and adhering to that plan over time is considerably more important for one’s long-term financial health than market performance. If you are interested in either creating a financial plan or reviewing a plan already in place, please reach out to your portfolio manager.

[1] PMI is a form of insurance that is paid by a mortgage borrower but protects the mortgage lender in case the borrower defaults on the mortgage. PMI typically costs between 0.5% and 1.0% of the total mortgage amount each year and can significantly increase the total cost of a mortgage. Borrowers are typically able to stop paying PMI when the loan-to-value (LTV) ratio of their mortgage reaches 80%.

[2] While most home equity loans carry fixed interest rates, there are variable rate home equity loan products in the marketplace.

[3] “Mortgage points” or “discount points” are effectively prepaid interest on a mortgage. By paying points at the time of loan closing, borrowers can obtain lower interest rates on their mortgages, saving them money over the life of the loan. One point is equal to 1% of the mortgage amount and typi- cally results in a 0.25% reduction in interest rate.

[4] Mortgage interest is tax-deductible up to a certain limit. For homes purchased prior to December 15, 2017, borrowers may deduct interest on loans up to $1,000,000. For homes purchased after this date, borrowers may deduct interest on loans up to $750,000. Interest on loan amounts above this threshold can no longer be deducted from one’s taxes.

This article is prepared by Pekin Hardy Strauss, Inc. (“Pekin Hardy”, dba Pekin Hardy Strauss Wealth Management) for informational purposes only and is not intended as an offer or solicitation for business. The information and data in this article does not constitute legal, tax, accounting, investment or other professional advice. The views expressed are those of the author(s) as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. Pekin Hardy cannot assure that the strategies discussed herein will outperform any other strategy in the future, there are no assurances that any predicted results will actually occur.