![]()

Photo by pogonici

The costs associated with college education in the United States have skyrocketed over the past 40 years, creating significant financial challenges for families who wish to provide for their children’s education. The large and growing financial burden posed by college education calls for thoughtful planning and disciplined saving on the part of parents. Fortunately, valuable savings tools are available to help families meet their education savings goals. This article discusses the most common education savings vehicles and provides guidance regarding the extent to which families should consider saving for education. Additionally, we discuss alternative strategies for helping families meet the financial challenges posed by college education costs.

Managing the Growing Cost of Education

For most parents, funding their children’s college educations is one of the most significant financial undertakings that they will ever encounter. Unfortunately, the undertaking is made more difficult by college education costs which continue to rise at a faster rate than inflation. To succeed in saving enough for college, it is critically important for parents (and grandparents) to save funds each year for college expenses in order to make the financial challenge a more achievable goal.

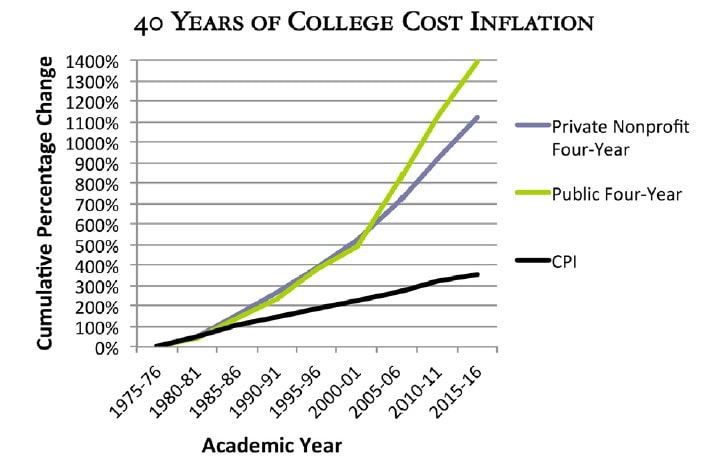

As the chart below illustrates, over the past 40 years, the average cost of tuition and fees at a private four-year university have increased 11-fold. Over that same period, the average cost of tuition and fees for a public four-year institution has increased by a multiple of nearly 14 times!

These increases in education costs have outpaced the increase in the broader cost of living (as measured by the Consumer Price Index) by 3% and 3.5% per year, respectively, over this time frame.1 Moreover, while there is no guarantee that education costs will continue to increase in the future at these historic averages, the numbers certainly argue for planning and preparation by parents who wish to assist their children with college education costs.

Source: The College Board, Annual Survey of Colleges; NCES, IPEDS data

The purpose of this Navigator is to provide initial guidance to families as they begin thinking about how to prepare for the financial burden of college expenses. As with any financial planning topic, there is no one-size-fits-all approach when it comes to saving for college, so we encourage you to contact us to discuss your unique situation and to develop an individualized plan for meeting this financial goal.

Ways to Save for College

To facilitate families’ college savings efforts, several savings vehicles (529 Plans, Coverdell Education Savings Plans, and Custodial Plans) have been created which enjoy various tax advantages and levels of investment flexibility, though it is important to fully understand the rules that apply to each type of investment account. Below we highlight several of the more common education savings vehicles and discuss some of the pros and cons of each.2

- 529 Plans

529 Plans are education savings vehicles that are eponymously named for Section 529 of the Internal Revenue Code, which allowed for the creation of these savings plans in 1996. 529 Plans are operated by state agencies or educational institutions for the express purpose of helping families set aside money for future college costs. 529 Plans provide certain tax advantages in order to incentivize families to save for education.At the Federal level, 529 Plans compound tax- free, so long as all proceeds are used for qualified education expenses.3 Similarly, asset growth achieved within a 529 Plan is exempt from state taxes, again assuming that proceeds are used for qualified education expenses. Many states provide additional tax breaks on contributions to 529 Plans. In Illinois, for example, contributions to the state’s 529 Plans are deductible from Illinois state taxes up to a limit of $10,000 per parent annually ($20,000 for joint filers).4Contributions to 529 Plans are considered gifts for Federal tax purposes, meaning that individuals may contribute up to $14,000 per child annually to a 529 Plan without incurring gift tax consequences ($28,000 per child for couples). However, a tax provision exists that allows a parent or grandparent to make five years’ worth of allowable contributions to a 529 Plan all at once, using up their gift tax reporting exemption for those years. Unlike many other tax-advantaged savings vehicles, 529 Plans do not have any income limits that restrict who may make contributions.529 Plans are typically administered by state agencies who hire approved asset managers to manage the assets of the plans. Investment options within 529 Plans are generally limited to broad asset classes and/or age-based investments.5 Families who wish to participate in a 529 Plan offered by a state other than the one in which they live may do so, though they may forego certain tax benefits (primarily state tax deductibility of contributions) as a result. Funds invested in one state’s plan may also be used to fund education costs at a school in a different state.6

One defining feature that makes 529 Plans unique with respect to other education savings vehicles is that plan assets remain the property of the parent or other adult who establishes the account. For this reason, 529 Plan assets may be transferred from one child to another.

For example, consider a family with two children. The parents establish a 529 Plan for their eldest child’s education costs and accumulate $100,000 by the time the child goes away to college. In this example, this child receives a substantial scholarship that pays for the majority of the child’s college costs, leaving $75,000 in the 529 Plan. Because these assets belong to the parents and not the child, the assets may be used to pay for the younger child’s education costs instead with no adverse consequences.7

An additional benefit of this ownership structure is that 529 Plan assets have less of an impact in determining a child’s financial aid award than many other types of education savings vehicles because parental assets receive less weight in the calculation of aid than assets owned by the child.

- Coverdell Education Savings Accounts

Originally known as Education IRAs, Coverdell Education Savings Accounts (“ESAs”) were renamed in 2002. ESAs are similar to 529 Plans in that they allow for tax-free growth and tax-free withdrawals, as long as proceeds are used for qualified education expenses.8 However, Coverdell ESAs differ from 529 Plans in that assets may be used to cover K-12 expenses, in addition to college expenses. This point of differentiation can be a very useful advantage in favor of Coverdell ESAs. However, ESAs also differ from 529 Plans in that contributions are capped at only $2,000 per year per child, and contributions are disallowed after the beneficiary reaches age 18, whereas 529 Plans allow for contributions regardless of the beneficiary’s age. One important point to keep in mind regarding the Coverdell ESA is that all funds must be withdrawn from the account by the time the beneficiary reaches age 30 or certain tax penalties will apply.Coverdell ESAs were previously known as Education IRAs because of their similarity to Roth IRAs. They are treated effectively the same way as Roth IRAs from a tax standpoint, assuming funds are used for qualified education expenses. Coverdell ESAs also give the account owner the same high degree of investment control as Roth IRAs, allowing for fully customized investment portfolios.Unfortunately, however, the similarities do not end there, as Coverdell ESAs also have eligibility criteria similar to those associated with Roth IRAs. In order to be eligible to make a full contribution to a Coverdell ESA, a single tax filer must have a Modified Adjusted Gross Income (MAGI) below $95,000. Filers with MAGI that is between $95,000 and $110,000 may make a partial contribution. For joint tax filers, the ceilings are $190,000 for a full contribution and $220,000 for a partial contribution. Filers whose incomes exceed these limits may not contribute to a Coverdell ESA. These contribution constraints make ESAs a savings tool with limited use for some. - Custodial Accounts

A custodial account is a legal structure established under the Uniform Transfers to Minors Act (UTMA; formerly known as the Uniform Gifts to Minors Act, or UGMA) that allows for property to be irrevocably transferred from an adult to a child. Property transferred to a minor under this law becomes the legal property of the minor and cannot be returned to the grantor. A parent or other adult must act as custodian of the account, managing the assets for the benefit of the minor until the minor reaches the age of majority (typically age 18 or age 21, depending on the state). Custodial accounts are similar in many ways to trusts, though they are far simpler and cheaper to establish from a legal perspective. In fact, custodial accounts were largely designed to allow for irrevocable transfers of property without the legal costs associated with the creation of a trust.While custodial accounts are taxable legal structures, they provide certain tax advantages over other taxable accounts. Because assets that are transferred to a custodial account become the legal property of the minor that owns the account, the minor must file income tax returns, and income earned by the account greater than $1,050 is taxed at the minor’s tax rate. However, in order to prevent abuse of this feature, Congress created a rule that is commonly referred to as the “Kiddie Tax,” which stipulates that custodial account income greater than $2,100 may be taxed at the custodian’s (likely higher) tax rate. This feature makes custodial accounts far less useful for tax sheltering purposes than a 529 Plan. Custodial accounts are treated the same way as 529 Plans from a gift tax perspective.

As stated above, custodial accounts are the legal property of the minors for whom they were created. Thus, custodians must make account decisions that are in the best interest of the minor, and assets must be used for the benefit of the minor or risk incurring tax penalties. When the minor reaches the age of majority, he or she takes full control of the assets, which can be used for any purpose. For many parents, this transfer of control issue can act as a major drawback of custodial plans. Parents should fully consider the risks associated with transferring control of custodial assets before opening and funding a custodial account.

Another point to consider regarding custodial accounts is the fact that such assets weigh far more heavily in college financial aid decisions than parental assets because they are the property of the minor. In addition, unlike a 529 Plan, assets in a custodial account may not be transferred to another child.

-

Trusts

Trusts are legal structures that allow for the irrevocable transfer of property from one person to another, much like a custodial account. However, trusts are far more complex than custodial accounts and can serve many different estate planning purposes. Setting up a trust is an involved process that typically requires the assistance of an estate attorney. While some families use trusts as a part of their plan to provide for their children’s educations, education may not typically be their primary purpose. Because of the cost and complexity involved in the creation of a trust, it is typically most suitable for the transfer of large assets as part of a broader estate plan.

When College Savings Plans are Not Ideal

Assuming that the amount of wealth is sufficient, parents who can spare the money up front might want to fund educational expenses directly. Use of college savings plans applies against an individual’s IRS annual gift tax exclusion. In the case of parents with a considerable asset base, they can make such annual gifts to a trust or custodial account for their children, and, in addition, they can make direct payments to tuition, which are not subject to the gift tax rules. In this situation, one can pay for college and separately transfer money to their heirs in a highly tax efficient manner.

How Much Should I Save?

Determining how much to set aside for a child’s education costs can be tricky because it is impossible to know exactly how college costs will evolve over time, and the assumptions involved are highly dependent on the educational aspirations of the child. There are numerous online college savings calculators that are available. We have found the calculator provided by The College Board to be useful in providing an estimate of potential college costs and the level of saving that would be necessary to fund those costs.9

By using this calculator, parents can better understand what kind of financial burden they might expect as a result of their children’s education projection. Again, the key to addressing the college savings conundrum is proper planning. The earlier parents are able to address this issue and begin saving, the better able they will be to meet their college saving goals. Even parents of older children who will be attending college in the near future can benefit from establishing an education savings plan. Having something saved, even a small amount, is better than having nothing saved.

It is also worth mentioning that there may be other strategies that families can employ to reduce the financial impact of their children’s college educations. First, college-bound children might consider attending a Canadian university, the costs of which tend to be materially lower than those of American institutions because of extensive government subsidization (even to non-Canadian citizens). Second, families should also try to fully exhaust the scholarship opportunities available to them. There are thousands of scholarships granted each year to students based on educational interests, ethnic background, academic performance, hobbies, membership in various clubs, and a number of other factors. Below is a list of five scholarship

Closing Thoughts

We understand the magnitude of the challenge that parents face with respect to saving for their children’s college educations. With limited resources, important savings decisions must be made, and we would urge parents to always prioritize retirement savings above education savings. Financing for education is readily available, while the same cannot be said for retirement; one cannot borrow money to pay for his or her retirement. However, in general, we encourage parents who wish to help fund their children’s college educations to start thinking seriously about this goal as early as possible and to begin committing capital as soon as they are willing and able. And, of course, we are here to help our clients understand the challenges posed by education costs and to develop a thoughtful plan for meeting those challenges.

1 This analysis assumes that the reader will be forced to pay full price for tuition, fees, and room & board. Many universities have sizable financial aid programs, but the lion’s share of such programs are need-based. Thus, if you have a significant asset base saved and/or have high levels of compensation, then your ability to tap into such financial aid programs is highly limited.

2 A summary table comparing the various plans is provided later in this

document.

3 529 Plan assets used for purposes other than qualified education expenses are subject to a 10% penalty, as well as applicable Federal and state income taxes. See https://www.irs.gov/publications/p970/ch08.html for a description of qualified education expenses.

4 Contributions may exceed this limit, but excess contributions are not tax-deductible.

5 Age-based investments typically allocate funds to multiple asset classes in varying proportions according to the perceived risk tolerance of beneficiaries in various age groups.

6 Some states offer pre-paid tuition plans for in-state public institutions that allow families to lock in a guaranteed tuition cost, regardless of how much costs might increase prior to a child’s matriculation. Funds invested in pre-paid tuition plans can be used at private and out-of-state institu- tions, though only on a dollar-for-dollar basis.

7 A key issue to address early on is to appoint a successor to own the

529 accounts should the owner die before the money is used. Otherwise,

the money used to fund the account may be considered as a gift that has

permanently left the estate of the owner.

8 See https://www.irs.gov/publications/p970/ch07.html for a list of quali-

fied education expenses for ESAs

9 https://bigfuture.collegeboard.org/pay-for-college/paying-your-share/college-savings-calculator

This article is prepared by Pekin Hardy Strauss Wealth Management (“Pekin Hardy”) for informational purposes only and is not intended as an offer or solicitation for business. The information and data in this article does not constitute legal, tax, accounting, investment or other professional advice. The views expressed are those of the author(s) as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. Pekin Hardy cannot assure that the methods discussed herein will outperform any other.

The consumer price index (CPI) is a measure of the average change over time in the prices paid by urban consumers for consumer goods and services.