“It is God’s way to bring the lofty low.”

─ Herodotus, Histories 7.10e

The ancient Greek historian Herodotus placed that warning in the mouth of Artabanus, as he tried to restrain King Xerxes before the Persian invasion of Greece. The Persian empire Herodotus described in his seminal work, Histories, and the Iran of today are separated by millennia, yet both ancient Persia and modern Iran were and are a serious force with whom to be reckoned by other world powers.

As of this writing, the current conflict has become harder to dismiss as a brief melee like the Twelve-Day War in 2025. Following failed weekend talks, the United States has moved to a naval blockade of shipping of Iranian ports and coastal areas. Front-month crude oil remains above $90/barrel, and the physical oil market has been far tighter than the price of oil futures would suggest. The September 2026 WTI crude oil contract, which settles on August 20, still sits near $80/barrel. Because the oil market appears sanguine about the Strait of Hormuz remaining closed, the stock and bond markets likewise seem rather nonchalant about the current disruption. Indeed, consensus earnings expectations remain surprisingly firm. FactSet noted on April 2 that total estimated Q1 2026 earnings had moved higher since year-end, and even after some downward revisions, the S&P 500 is still expected to produce double-digit profit growth. Indeed, that is not the posture of a market expecting a supply shock-induced recession.

As we have said in past letters, war is always inflationary. In the case of this war, roughly 20-25% of the world’s oil and natural gas trade that normally passes through the Strait of Hormuz has ceased entirely. In addition, roughly one-third of the global fertilizer trade travels through the Strait of Hormuz; as a result, urea fertilizer prices have risen materially since the war began. In the early phase of such a supply shock, investor behavior involves cutting leverage, selling positions, thus causing assets with strong fundamentals to decline in price temporarily. That is how we would interpret the recent weakness in gold, silver, platinum, and copper. These declines looked to us more like short-term de-risking and margin-driven liquidation; over time, we believe the prices of these commodities should also rise as a medium-term consequence of war, increased fiscal deficits, and a supply shock that raises energy prices and shortages.

We do not have a crystal ball; we do not claim to know the future of this war and its consequences better than anyone else. For that reason, we are wary of speaking with false precision about military outcomes. What we do know is that the range of outcomes for investors remains wide. This war is occurring at a time when the world economy was already becoming more de-globalized, more regional, and more inflationary. In the recent past, we have been emphasizing these broader economic forces repeatedly, including a structurally weaker dollar over time, foreign investors becoming less eager to own richly valued U.S. assets, continued demand for gold as a reserve asset, and the case for real assets, selective foreign exposure, strong balance sheets, and owning companies with pricing power. We believe this conflict accelerates these already existing trends.

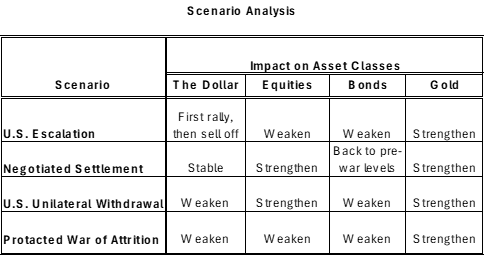

Below are several future scenarios we are considering as possible outcomes of the war:

- The United States Escalates from Blockade to a Broader Campaign

If the blockade is followed by sustained strikes on bridges, power plants, ports, water systems, transport links, and other infrastructure, the result would likely be a more severe and longer-lasting supply shock. President Trump has threatened attacks on bridges and power plants if Iran did not accept his terms. In such an environment, oil prices would likely move materially higher from current levels, and refined products could become even tighter than crude oil. Fertilizer prices would likely rise further as natural-gas-linked inputs, shipping costs, and insurance costs move higher in unison. Corporate earnings would come under pressure across transportation, chemicals, industrials, consumer cyclicals, and other energy-intensive sectors. The dollar would probably rally at first because crises still generate demand for dollar liquidity. Over a medium-term horizon, however, a deeper war that intensifies fiscal strain and forces lower interest rates into an oil spike would likely be negative for the dollar in real terms and constructive for gold. As fiscal spending on the war accelerates, Treasury yields would spike, putting downward pressure on bond prices. - A Negotiated Settlement Reopens the Strait

This scenario would result the best economic outcome for all parties. A genuine settlement restraining Iran’s nuclear program and bringing sanctioned Iranian oil back onto the market would lower the war premium embedded in energy and restore shipping volumes over time. Oil, natural gas, and fertilizer prices would fall meaningfully from current levels, although probably not all at once. A negotiated settlement would not quickly reverse the physical damage already done to refineries, export terminals, pipelines, and LNG infrastructure. In this scenario, the dollar would lose some of its safe-haven bid, corporate margins would stabilize, and gold could pause or correct in the short run. That said, the long-term trends toward deglobalization, reserve diversification, higher fiscal spending, and a weaker dollar would persist, which would be long-term bullish for gold and global equities. Bond yields would likely move towards their pre-war trading range, while corporate earnings would likely be strengthened by an operating environment with low and stable energy prices. - The Trump Administration Declares Unilateral Victory and Withdraws

In this scenario, U.S. ships would withdraw from the Persian Gulf even while Iran retains practical control over the Strait of Hormuz. Passage through the Strait going forward would likely become contingent on Iranian approval, tolls, and/or non-dollar settlement. If a meaningful share of energy trade begins to move toward yuan, gold, bitcoin, and/or other non-dollar mechanisms at the margin, the long-term structural support of the U.S. dollar would erode further, while structural support for non-dollar reserve assets would conversely strengthen. Gold would likely benefit not just as an inflation hedge, but as a neutral reserve asset replacing U.S. Treasuries. Inflation in the United States would likely accelerate, and corporate earnings would rise with it, especially among companies that generate substantial earnings in foreign currencies. At the same time, cash and bonds would likely underperform due to upward pressure on interest rates. - A Protracted War of Attrition Develops, like the Ukraine-Russia War

This scenario may be the most damaging one of all the options. A protracted war would not necessarily produce the largest one-day market moves. However, like the Ukraine-Russia War, it could keep pressure on the world economy for much longer than investors currently expect. Protracted conflict might mean recurring strikes on infrastructure, disrupted shipping, higher insurance costs, depleted energy inventories, and the steady accumulation of accelerating inflationary pressures. It also means that the real economy eventually catches up to the headlines, hurting chemical companies, straining food and fertilizer markets, slowing the AI build-out, crushing consumer discretionary demand across the world, and forcing energy rationing and emergency measures across multiple countries. In this scenario, the chance of an inflationary recession (stagflation) increases considerably, which would be detrimental for most asset classes.

Another risk to this scenario is that energy-importing countries might have to sell liquid dollar assets, such as Treasuries or U.S. equities, to defend their currencies and pay for much higher energy bills. If that were to happen, the same shock that lifts inflation could also tighten financial conditions, putting additional pressure on capital markets. If policymakers eventually respond with more liquidity to offset that pressure, the dollar may still enjoy intermittent safe-haven rallies while weakening over time in real purchasing-power (inflation-adjusted) terms. Gold, commodity producers, and businesses with real assets and pricing power would likely hold up better than long-duration financial assets.

There are other scenarios that might represent some combination of the four scenarios we described, with a corresponding combination of consequences.

Investment Implications

The common thread across most of the scenarios we described is not a set of factors that should lead to increasing wealth. Wars usually destroy wealth by compressing margins, raising input costs, depreciating currencies, and eroding purchasing power. In light of this conflict, we are investing especially carefully right now to avoid permanent impairment, maintain liquidity, and own assets that can withstand a wider range of outcomes than the market is currently discounting. As previously stated, Mr. Market seems to believe the war will end soon with limited negative economic consequences. While we cannot predict each turn in the conflict, let alone how it will end, we can protect capital and own an overweight position in assets that outperform in an inflationary or stagflationary environment.

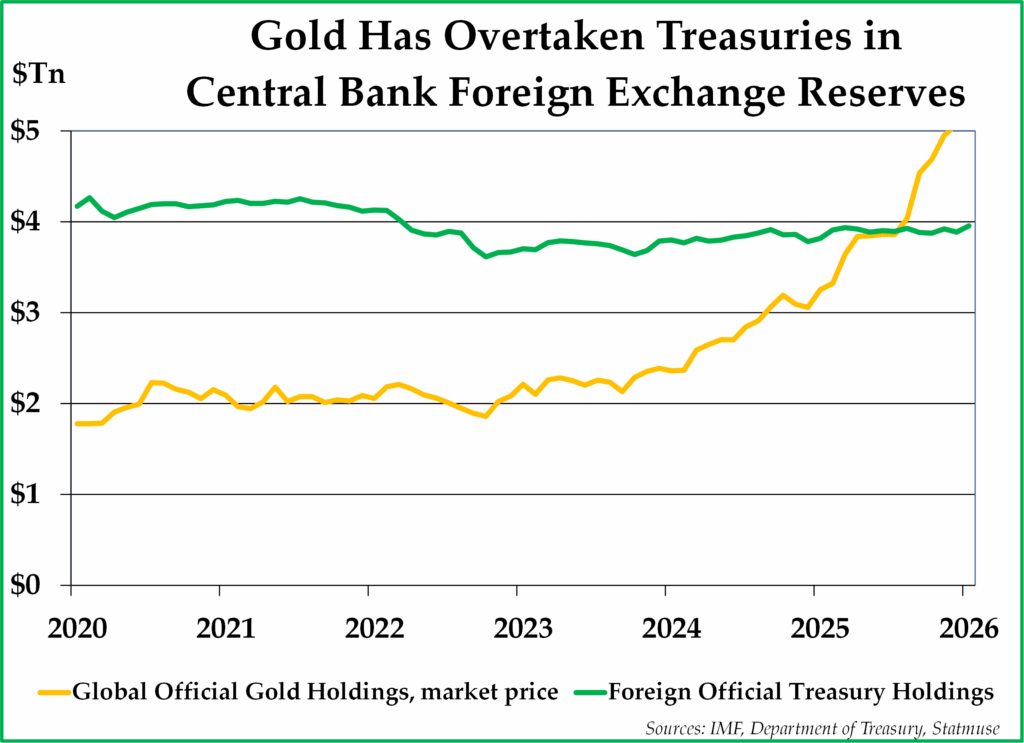

Across three of our four scenarios, and arguably across all four if any settlement proves partial or temporary, the medium-term consequence remains inflationary. Higher energy costs are already beginning to flow through to fertilizers, food, freight, petrochemicals, and manufactured goods. We believe central banks are likely to continue holding a smaller allocation to U.S. Treasuries and a larger allocation to gold (see chart on the following page). Across all four scenarios, the dollar may enjoy temporary bursts of strength, but the medium- to long-term outcome is likely a weaker dollar, higher commodity prices, continued strength in gold, and upward pressure on interest rates.

*****

Finally, we wish to thank you for your continued trust. Periods like this are a reminder that our stewardship matters most to our clients when the future is hard to see clearly. We do not take the responsibility of protecting your hard-earned capital lightly, and we are grateful for the opportunity to continue doing that work on your behalf.

Sincerely,

Pekin Hardy Strauss Wealth Management

This commentary is prepared by Pekin Hardy Strauss, Inc. (dba Pekin Hardy Strauss Wealth Management, “Pekin Hardy”) for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any security. The information contained herein is neither investment advice nor a legal opinion. The views expressed are those of the authors as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. Although information has been obtained from and is based upon sources Pekin Hardy believes to be reliable, we do not guarantee its accuracy. There are no assurances that any predicted results will actually occur. The S&P 500 Index includes a representative sample of 500 hundred companies in leading industries of the U.S. economy, focusing on the large-cap segment of the market.