We have published this Navigator at this same time each of the past several years in order to highlight the importance of IRAs and to encourage our clients to make their annual IRA contributions prior to the tax filing deadline. Given the vital nature of this topic, we will continue to re-publish this Navigator each year with contribution and deductibility rules updated for the new tax year. We hope that you will find this updated letter to be helpful and informative.

Individual Retirement Accounts, or IRAs, are one of the most powerful savings and investment tools currently available to investors. An IRA allows assets to grow unencumbered by the drag of taxes, and IRA contributions may be tax-deductible in some cases. This article discusses the key role that an IRA should play in most investors’ savings and investing strategies and examines the primary characteristics pertaining to each of the four most common types of IRAs.

Unless you have unusually dutiful and wealthy children who intend to take care of you when you retire, it would be remiss of you not to take advantage of investing in an individual retirement account (IRA), regardless of your income level. By maximizing contributions to an IRA, these accounts help to reduce potential tax liabilities today and allow the assets to grow tax-deferred for many years. Uncle Sam only allows investors to contribute a limited amount to an IRA each year, and there is no “doubling down” the following year if an opportunity to contribute is missed. The tax code allows older savers to make additional “catch-up” contributions, but even this provision only allows for an incremental $1,000 per year after age 501

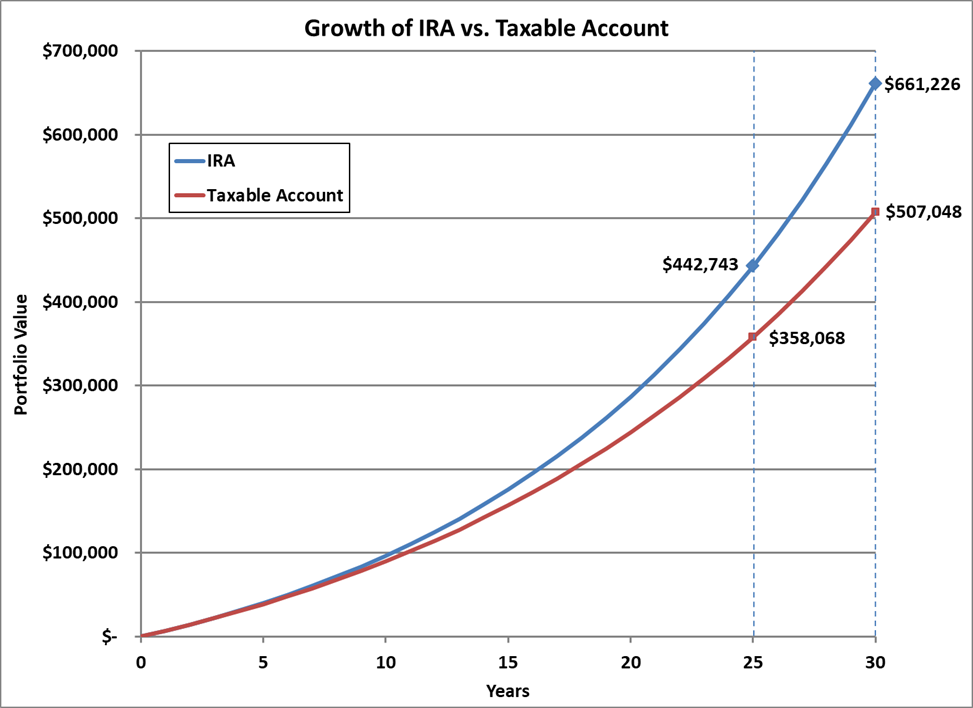

As the maxim goes, “time in the market is more important than timing the market,” thanks to the powerful impact of compound returns. To illustrate the power of compounding over time, let us provide an example. An investor contributes the maximum allowed ($7,000 for tax year 2025) in an IRA this year; assuming a 7% annual return compounded over 25 years, the original $7,000 contribution would grow to $37,992. After 30 years, the original contribution would have grown to $53,285. The investor would earn an additional $15,293 (or more than twice the original investment!) just by investing for an incremental five years.

Better yet, assuming the investor were to save $7,000 in a retirement account every year for the next 25 years, starting this year (and again assuming a 7% annual return), the retirement account would increase to $442,743 at the end of that period. After 30 years, the retirement account would increase to $661,226. That represents a nearly 50% difference due entirely to having saved for an additional five years! Furthermore, for an investor in the highest federal income tax bracket and who lives in the state of Illinois, for example (Illinois residents are currently subject to a 4.95% state income tax rate), the value of an IRA after 30 years could be more than 30% greater than a taxable account utilizing the same saving and investing strategy. The chart below provides a graphical representation of how an IRA and a taxable account might grow over time for such an investor, assuming a 7% annual rate of return and annual contributions of $7,000. For the sake of simplicity, we have not adjusted these numbers for inflation, but they nonetheless provide a clear illustration of the power of “time in the market,” as well as the potential benefits of investing in a tax-deferred investment vehicle.

Source: Pekin Hardy Strauss

The returns assumed in this illustration are not guaranteed, and each investor’s actual experience may be different.

Because investment gains in IRA accounts are tax-deferred or tax-exempt, IRAs can provide investors with the flexibility to change investments whenever necessary without creating a taxable gain. There are four main variants of IRAs that are available to investors, and each type has its advantages and drawbacks, depending on an investor’s age, employment situation, income-tax bracket, distribution needs, etc. The balance of this article will focus on the reasons that a person might utilize one type of IRA over another, as well as the rules and regulations governing each type. Of course, the ultimate decision of which IRA is the appropriate vehicle for you to use should be made in consultation with your portfolio manager.

Traditional IRA

An investor is eligible to invest in a traditional IRA regardless of income level. The primary benefit of a traditional IRA account is that there are no income taxes on investment earnings until withdrawals are made. Investors are allowed to start withdrawing money from a traditional IRA at age 59½ without a penalty, though ordinary income tax rates apply to any distributions. The age at which withdrawals become mandatory changed as part of the Secure Act, from age 70½ to age 72, except for individuals who reached age 70½ prior to January 1, 2020. The Secure Act 2.0 pushed the mandatory withdrawal age further to age 73 starting in 2023. IRA owners who reached age 72 in 2022 must adhere to the previous rules and receive required distributions from their IRAs. If money is withdrawn prior to age 59½, a 10% Federal penalty tax will be applied to the withdrawal in addition to regular income taxes, which will apply to all earnings and any amounts that were originally contributed on a tax-deductible basis. Mandatory withdrawals, called Required Minimum Distributions, or RMDs, are calculated according to the investor’s life expectancy and account size and grow over time as a percentage of the portfolio.

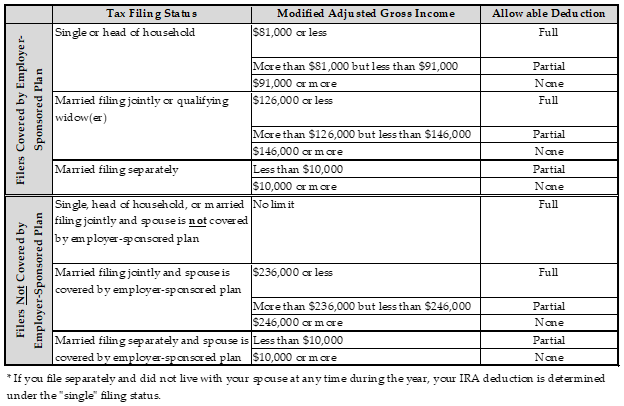

A traditional IRA lets you put away as much as $7,000 annually, as of tax year 2025, or $8,000 if you are age 50 or older (these limits will increase to $7,500 and $8,600 for tax year 2026). The tax deductibility of contributions is dependent on your income and whether or not you have an employer-sponsored retirement plan, such as a 401(k). Anyone who has earned income, regardless of age, can make a traditional IRA contribution.2 To deduct a traditional IRA contribution from taxable income, an investor’s Modified Adjusted Gross Income, or MAGI, must be less than IRS income limits; these limits are set by the IRS each year and depend upon a taxpayer’s filing status. Investors whose incomes exceed these limits may still be eligible for a partial deduction, but these deductions are phased out as income approaches an upper limit set by the IRS. The table below outlines the contribution and deduction limits for traditional IRAs for tax year 2025 (these limits will increase for tax year 2026).

Please note that even if you do not qualify for a tax deduction, it may still make sense for you to contribute to an IRA because of the attractive tax shield that an IRA creates for a portion of your investment income.

Traditional IRA Deduction Limits

Source: IRS

Roth IRA

While traditional IRA earnings compound on a tax-deferred basis, Roth IRA earnings compound on a tax-exempt basis. Unlike a traditional IRA, there are no taxes on Roth IRA withdrawals when you withdraw money during retirement. There are also no age limits on eligibility for a Roth IRA, and, unless the laws change, there are no Required Minimum Distributions. However, investors who wish to open and/or contribute to a Roth IRA must meet certain income requirements, which depend on tax filing status. Because of the tax treatment differential, a Roth IRA typically is a better retirement vehicle than a traditional IRA, assuming that an investor meets the requirements to contribute to a Roth IRA.

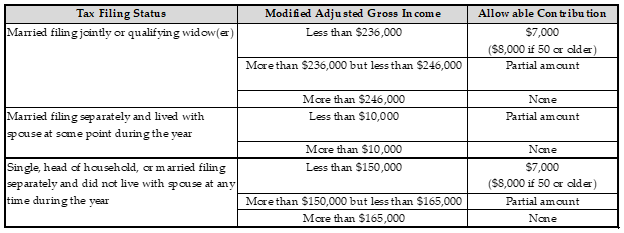

Contribution limits for Roth IRAs are the same as for traditional IRAs (currently $7,000 with a $1,000 incremental catch-up for people older than 50; these limits will increase to $7,500 and $8,600 for tax year 2026), and investors can contribute the maximum amount to a Roth IRA, regardless of whether or not they participate in employer-sponsored retirement plans. As with a traditional IRA, withdrawals can be made from a Roth IRA without penalty after age 59½, provided that the account has been open for more than five years.3 Failing to meet these requirements may result in a penalty tax, ordinary income tax, or both being applied to the withdrawal. Tax year 2025 contribution limits for Roth IRAs are shown in the table set forth below.

Roth IRA Contribution Limits Source IRS

Source IRS

While the Roth IRA contribution limits listed above prevent high-income earners from making direct contributions to a Roth IRA account, anyone can convert a traditional IRA into a Roth IRA, regardless of income level. Some higher-income investors rely on this conversion option every year, by making an annual contribution to their traditional IRA and then converting those traditional IRA assets to Roth IRA assets (often referred to as a “Backdoor Roth IRA Contribution”). It should be noted that some Roth IRA conversions may be taxable events if the investor has any traditional IRA assets that have not yet been taxed as ordinary income.

SEP IRA

A Simplified Employee Pension (SEP IRA) may be the best retirement account option for sole proprietors and small businesses with up to 100 employees. Employers can contribute as much as 20% of self-employment income each year, and this limit rises to 25% if the business is incorporated. Contributions are capped at $70,000 for tax year 2025 and will increase to $72,000 in 2026 (assuming this falls below the 20% and 25% limits). As with most other non-Roth retirement accounts, investment returns grow tax-deferred until money is withdrawn.

Contributions to SEP IRA accounts can be made by both the employer and by the employee. Contributions made by the employer on an employee’s behalf must be the same percentage for each employee annually. These contributions are tax-deductible as a business expense and are not mandatory every year. However, employers must decide each year whether or not to fund their accounts, and if they make contributions for themselves, they must also make contributions for all eligible employees.

In general, any employee who has worked for the same employer in at least three of the past five years should be allowed to participate in a SEP IRA, provided that he or she is at least 21 years of age and earns at least $600 annually. SEP IRAs carry the same rules as traditional IRAs when it comes to employee contributions. Employees can contribute up to $7,000 or $8,000 if they are age 50 or older for tax year 2025 (these limits will increase to $7,500 and $8,600 for tax year 2026). Sole proprietors are subject to the (higher) employer limits rather than the employee limits.

Any withdrawals that are made from a SEP IRA prior to age 59½ are subject to ordinary income tax, as well as a 10% penalty. Like Traditional IRAs, withdrawals from SEP IRAs become mandatory after age 73, at which point all withdrawals are taxed at ordinary income tax rates.4

SIMPLE IRA

A Savings Incentive Match Plan for Employees (SIMPLE IRA) is an alternative to 401(k) plans for businesses with 100 or fewer employees. These plans are a win-win for employers and employees. Employers can either match employee contributions or simply contribute 2% of employee salaries up to the statutory contribution limits. Employers who match employee contributions may match up to the lesser of 3% of each employee’s salary or the $16,500 employee contribution limit for tax year 2025 ($20,000 if the employee is age 50-59 or 64+; $21,750 if the employee is age 60-63). These limits will increase to $17,000, $21,000, and $22,250 for tax year 2026. Notably, the IRS implemented some changes for tax year 2025 that allow for even greater contributions for some smaller plans. Employers with 25 or fewer employees must allow contributions up to $17,600 for employees under age 50, $21,450 for employees aged 50-59 or 64+, and $22,850 for employees aged 60-63 (these limits increase to $18,100, $21,950, and $23,350 for tax year 2026). Employers with 26 to 100 employees may voluntarily allow for the higher contribution limits. Like other IRA plans, SIMPLE IRAs grow tax-deferred until withdrawals are made.

There are no age limits on participation in a SIMPLE IRA plan. However, withdrawals made before age 59½ may incur a steep 25% penalty if the withdrawal is made within the first two years of joining the plan, and there may still be a 10% penalty for withdrawals taken after the first two years. Money in SIMPLE IRAs is locked into the accounts, so an employee who moves to another employer within two years of joining a plan must wait until the two years have passed before moving the money to another plan in order to avoid a penalty.

***********************************************************************************************

As noted above, IRAs are powerful savings tools that should generally be maximized each year. Given the real possibility of increasing tax rates in the future, investors would be wise to consider every tax-sheltering opportunity afforded to them. IRAs provide one important such opportunity. We would urge anyone who is eligible (and able) to consider making the maximum contribution to his or her IRA each and every year. If you are already contributing the maximum amount to a 401(k) plan, then you have taken an important step in preparing for retirement. However, although contributions to an IRA may not be tax-deductible for you, we would still encourage you to consider making IRA contributions in addition to your 401(k) contributions in order to take full advantage of all of the tax-sheltering options that have been made available to you.

If you do not yet have an IRA, do not delay talking to your portfolio manager to discuss whether opening and contributing to one makes sense for you. For those who already have an IRA, we encourage you to make contributing to your account every year a high priority. As the examples we discussed showed, even one year of delay can make a major difference over time, due to the power of compounding. And, as always, we are more than happy to help you to understand how best to take advantage of IRAs.

1 The annual catch-up amount will increase to $1,100 in 2026

2 Prior to the passing of the Secure Act, those who had reached age 70 1/2 could no longer contribute to an IRA, but the new legislation allows older savers who are still working to continue contributing to their IRAs as long as they are earning income.

3 Withdrawals of an investor’s basis in a Roth IRA (the total of all contributions) can be withdrawn at any time without penalty, as these are after-tax dollars

4 This does not apply to SEP IRA owners who reached age 72 prior to January 1, 2023. These individuals must adhere to the previous rules and receive required distributions from their SEP IRAs.

This article is prepared by Pekin Hardy Strauss, Inc. (“Pekin Hardy”, dba Pekin Hardy Strauss Wealth Management) for informational purposes only and is not intended as an offer or solicitation for business. The information and data in this article does not constitute legal, tax, accounting, investment or other professional advice. The views expressed are those of the author(s) as of the date of publication of this report and are subject to change at any time due to changes in market or economic conditions. Pekin Hardy cannot assure that the strategies discussed herein will outperform any other investment strategy in the future, there are no assurances that any predicted results will actually occur.