Recent legislation enacted under the One Big Beautiful Bill Act (OBBBA) introduced a new custodial, retirement-style account designed to encourage long-term investing for children. Commonly referred to as a “Trump Account,” 530A Accounts represent a new, attractive planning vehicle for certain young families with specific tax and investment characteristics.

Overview

530A Accounts benefit eligible children under the age of 18 by jumpstarting their long-term financial security.1 While structured as a type of Traditional IRA, it operates under a unique set of tax-advantaged rules during the child’s early years (the “growth period,” which ends when the child turns 18). At age 18, the 530A Account converts into a traditional Individual Retirement Account (IRA) giving the beneficiary ownership and control of the funds.

Key Features During the Growth Period

- Account Owner: The child is the legal owner (with a custodian acting on their behalf).

- No Earned Income Requirement: Contributions may be made even if the child earns no compensation.

- Annual Contribution Limit: You may contribute up to $5,000 per year from private sources (indexed for inflation after 2027)2. The first contributions can be made beginning on July 4, 2026.

- Government Seed Contribution: Children born between January 1, 2025 and December 31, 2028 may receive a one-time $1,000 Federal contribution under a pilot program. The government’s $1,000 seed contribution and the <$5,000 contribution from private sources are separate rules and do not count against each other.

- Investment Restrictions: Funds must be invested in eligible investments such as a mutual fund or ETF that primarily tracks the performance of an index of U.S. Companies.

- No Distributions: Withdrawals are generally prohibited during the growth period.3

The structure of 530 Accounts is intentionally long-term oriented with limited flexibility during the growth period. It is designed to promote disciplined savings for minors by emphasizing sustained investing and restricting early access to funds. By limiting distributions and narrowing investment options, the framework encourages setting aside capital that has the potential to generate compound returns. For families who value long-term focus, this design may be beneficial. However, it also requires comfort with reduced liquidity and planning flexibility prior to the child reaching adulthood.

Planning Considerations

The appeal of the account lies primarily in its behavioral and structural characteristics rather than its contribution size.

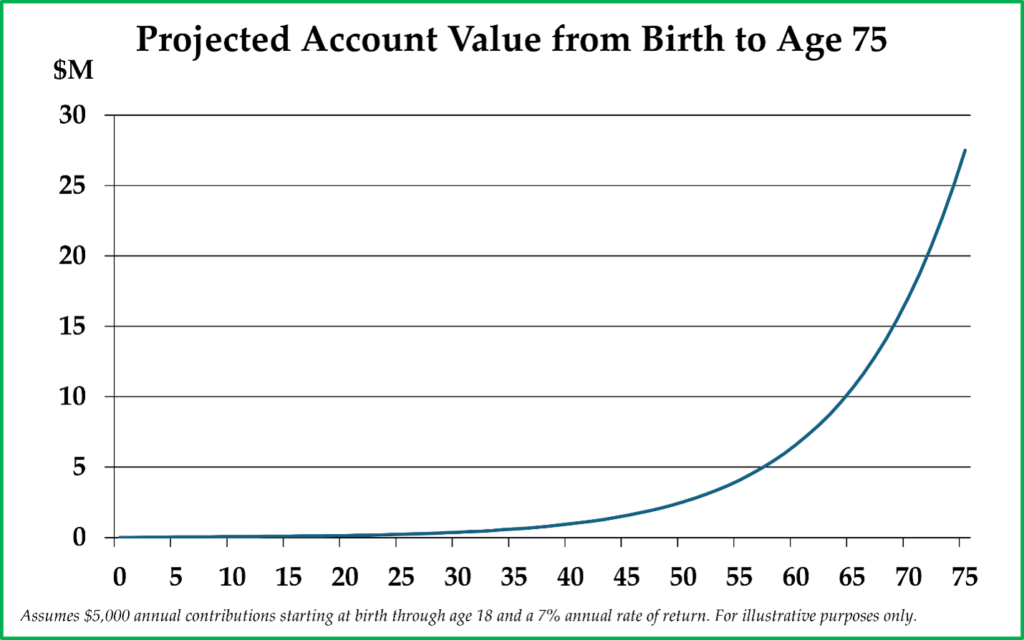

Early Tax-Deferred Compounding

Because contributions do not require earned income, families may begin funding the account shortly after birth. Consistent annual contributions at the permitted limit, compounded over 18 years, can create a meaningful start to retirement savings.

Government Seed Contribution

For families with eligible birth years (currently January 1, 2025 – December 31, 2028), the $1,000 federal contribution provides immediate initial capital free to the account owner, enhancing long-term compounding potential.

Enforced Long-Term Discipline

Unlike custodial accounts or certain other savings vehicles, the prohibition on early withdrawals creates a forced long-term investment horizon. For some families, this constraint may be a positive feature rather than a limitation.

Retirement Framing

At age 18, the account transitions into a traditional IRA. This design subtly reinforces retirement-based thinking from an early age, potentially fostering better long-term savings behavior.4

Planning Limitations

Despite its structural benefits, the 530A Account provides a complementary role in many financial planning situations. Its value depends on how effectively it integrates with existing savings strategies, tax considerations, and long-term goals.

Contribution Limits

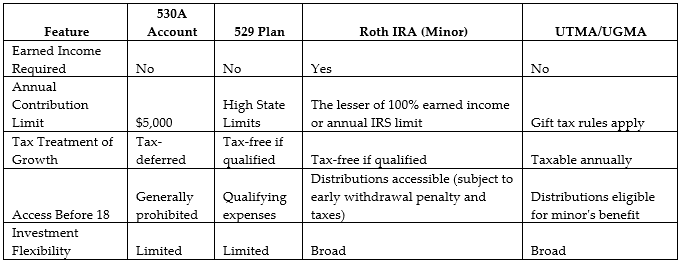

The $5,000 annual private contribution limit is relatively low relative to the 529 plan funding capacity or gifting strategies. 529 plans permit significantly higher contribution limits and Federal gift tax rules allow individuals to make annual exclusion gifts (currently $19,000 for individuals in 2026).5

Limited Flexibility Before Age 18

During the growth period, distributions are largely prohibited. Families seeking flexibility for education, extracurricular expenses, or other needs may find 529 plans or custodial accounts more adaptable.

Investment Constraints

Investment options are limited to low-cost, broad U.S. index funds meeting specific regulatory criteria. While cost efficiency is beneficial, some families may prefer broader asset allocation flexibility.

Tax Characteristics at Distribution

Beginning January 1 of the year the child turns 18, the special rules expire and, as previously mentioned, the account transitions into a traditional IRA, subject to standard IRA distribution rules, including potential early withdrawal penalties if the distributions occur before age 59 ½. Future withdrawals will generally be taxable as ordinary income unless offset by deductions or structured under applicable exceptions.

Coordination with Existing Vehicles

For education-focused planning, 529 plans generally provide greater tax efficiency due to tax-free growth when used for qualified education expenses. For working minors, Roth IRAs continue to offer distinct tax advantages due to tax-free growth and tax-free withdrawal flexibility. Custodial accounts (UTMA Uniform Transfers to Minors Act/UGMA Uniform Gift to Minors Act) offer broad flexibility in how funds may be used, though earnings are subject to annual taxation.

Source: IRS.gov

Source: IRS.gov

Each vehicle serves a different purpose. The optimal structure depends on the intended use of funds and the household’s broader tax strategy.

Who Might Consider 530A Accounts?

The account merits consideration from:

- Families with newborns in eligible birth years seeking to capture the $1,000 government seed contribution. Early funding combined with an 18-year investment horizon may create a foundation for retirement savings.

- Households that have already maximized 529 funding and wish to establish additional long-term savings for their children. 530A Accounts may serve as a complementary vehicle focused more broadly on future retirement savings.

- Families who value disciplined, long-term investment frameworks. Some families prefer guardrails that prioritize sustained compounding over liquidity. The limited distribution rules and restricted investment options may appeal to those who view structural constraints as a behavioral advantage rather than a limitation.

- Parents Seeking to Instill Early Savings and Investing Habits into their Children. This structure can be viewed as a way to introduce long-term retirement investing early in a child’s life. Since the contributions do not require earned income, parents can begin building retirement assets for a child well before the child enters the workforce.

Closing Thoughts

The introduction of this new investment account expands the available financial planning for children, but its practical impact will vary by household. The limited contribution ceiling and investment restrictions suggest that, for most families, the account will function as a supplemental vehicle alongside 529 plans, Roth IRAs for working minors, and broader estate planning strategies.

As with any legislative development, its value depends on how thoughtfully it aligns with a family’s liquidity needs, tax profile, gifting strategy, and long-term objectives. Parents with young children or expected births in eligible years should consider opening 530A accounts to benefit from the one-time $1,000 contribution at a bare minimum; post-receipt of the Federal $1,000 contribution, families can look at their own unique circumstances to understand whether to contribute additional capital to their child’s 530A Account. As for children born prior to 2025, parents should evaluate whether 530A Accounts and/or alternative vehicles best serve their financial goals for their children.

In summary, rather than replacing existing planning tools, 530A Accounts may serve as an additional building block that can be integrated into a coordinated strategy designed to support a child’s long-term financial need.

This article is prepared by Pekin Hardy Strauss, Inc. (“Pekin Hardy”, dba Pekin Hardy Strauss Wealth Management) for informational purposes only and is not intended as an offer or solicitation for business. The information and data in this article does not constitute legal, tax, accounting, investment or other professional advice. The views expressed are those of the author(s) as of the date of publication of this report and are subject to change at any time due to changes in market or economic conditions. Pekin Hardy cannot assure that the strategies discussed herein will outperform any other investment strategy in the future, there are no assurances that any predicted results will actually occur.

1A 530A Account is the official IRC name for a Trump account. For purposes of this analysis, we will be referring to these investment vehicles as 530A Accounts, although they may be commonly known as Trump Accounts.

3 Limited exceptions apply and include qualified rollover contributions, qualified ABLE rollover contributions, distributions of excess contributions, and distributions upon death of the account beneficiary.

4 The one notable difference between a Traditional IRA and a 530A Accounts is that they cannot be aggregated for certain calculations like required minimum distributions (RMDs), so they are tracked separately.