“It’s the economy, stupid!”

─ James Carville

The reputations for presidents in the annals of history often rise and fall with the fluctuations in the economy. As President George H.W. Bush would tell you from personal experience, the health of the economy plays a significant role in determining the potential re-election of an incumbent president and the public’s historical view of each president. With regards to popularity, political strategist James Carville wisely and succinctly made the statement set forth above. Because of the strong tie between the economy and approval ratings, presidential elections have become a typical crossroads for assessing the economic record of the incumbent president. Furthermore, no president in history has tied the success of his Administration to the economy and the stock market more than President Donald J. Trump.

In recent months, we have received an increasing number of questions about the upcoming election, with clients asking us what will likely happen to their investment portfolios if President Trump or former Vice President Joe Biden wins the election.

Our view is that presidents maintain far less control over the economy or the markets than most people think. Economic growth and stock market performance remain highly dependent on where the country is in the economic cycle. The president has little influence over the technological and demographic forces that impact the economy. Moreover, the president cannot unilaterally set interest rates, print money, make laws, pass spending bills, and change the tax code; the president needs the cooperation of Congress and the Federal Reserve to accomplish such actions.

The economic tools solely available to the president are limited to using his bully pulpit, nominating Federal Reserve governors, conducting foreign policy, and signing executive orders. Indeed, Trump has aggressively used all these tools in an attempt to bolster economic growth. Nevertheless, the causation between such presidential actions and economic results is often uncertain and difficult to prove with any kind of confidence.

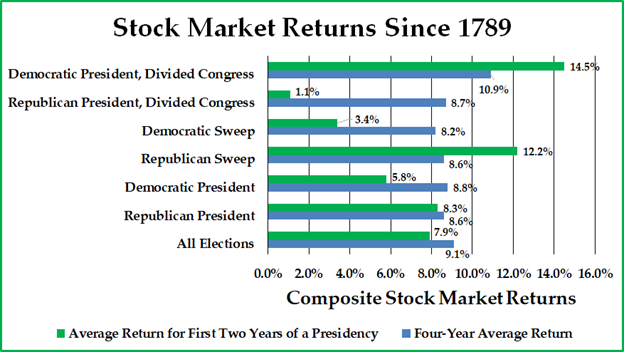

The chart set forth at the top of the next page depicts the stock market returns throughout U.S. history, depending on the party affiliation of the president and the Congress. Importantly, this data involves cobbling together several indices over a long period during which the economy and the two major political parties were continually evolving. In addition, past performance is not an indicator of future performance. For these reasons, we harbor our doubts that these figures can be relied upon to forecast future returns of the stock market or make investment decisions.

Significant differentials in stock market performance exist between the two political parties in the first two years of a presidency, but, by the end of the presidential term, these differentials have essentially vanished. Stock market returns have been stronger under Democratic presidents than under Republican presidents, but not by much (0.2% differential per year).

Over a more recent period from 1926 to 2019, occupancy of the White House was roughly shared between the parties; the United States had a Republican president for 46 years and a Democratic president for 48 years. Over that more recent period, the average annual return for the S&P 500 Index under a Republican president was 9.1%, while a Democratic president oversaw S&P 500 annual returns of 14.9%.[1] The performance differential compared to the data set forth above is due to several factors, including but not limited to the facts that Republicans held the Oval Office during both the Financial Crisis and the Great Depression and that Democrats presided over the subsequent recoveries.

Breaking down these returns by the individual president, Democratic President Bill Clinton boasted the highest annual S&P 500 Index returns under his tenure; the stock market climbed 17.2% per year under Clinton. Bringing up the rear was Republican President Herbert Hoover, who took power right before the Great Depression began; the stock market return generated an annual return of negative 27.2% while Hoover was in office.[2]

As previously mentioned, the president has far less control over the capital markets than most people assume. Clinton did not catalyze the mass commercialization of the Internet or cause a large portion of the Baby Boomer generation to be at their maximum earnings potential during his presidency. Most historians do not pin the Great Depression on Hoover’s shoulders; rather, the lion’s share of the blame was attributed to an inadequate monetary response by the Federal Reserve and an insufficient fiscal stimulus by Congress until years later. Importantly, Clinton benefited from the lucky timing of a stock market bubble peaking as he left office, while Hoover suffered from the unfortunate timing of a stock market bubble peaking as he arrived in office. The data simply does not bear out singular credit to Clinton or blame to Hoover for the investment returns generated under their respective tenures.

Overall, history suggests that markets seem to ignore the party affiliation of the president. Government policies supported by the president do put their imprint on the economy, but lasting policy fingerprints usually affect the economy and the markets over a long period and generally are the result of bipartisan legislative compromises.

Commonalities Between the Candidates

In an election season, it is easy to identify policy differences as they are highlighted in political ads, news articles, and debates. Nevertheless, when it comes to the economy and the markets, we would suggest that certain similarities exist between the two presidential candidates.

First, the hard line drawn on trade with China by Trump is likely to expand with a Trump second term. His trade policies promote mercantilism, and he uses protectionism to defend U.S. industries from foreign competition and reduce the U.S. trade deficit. A President Biden would likely ease U.S./China tensions to a certain degree, likely in coalition with other key trading partners. However, given policymaker rhetoric on both sides of the political spectrum on this issue and increasing skepticism of China’s intentions with voters, it is reasonable to question whether Trump’s approach towards China would soften much under Biden.

Second, no matter who wins the election, powerful technology companies are expected to face increased government pressure. President Trump would likely accelerate the broad-scale regulatory scrutiny of technology companies that marked his first term, in our view. That effort has included allegations of anti-conservative free speech limitations, antitrust investigations of Alphabet and Facebook, and actions against Chinese-controlled Internet companies such as TikTok and WeChat. Biden has also been somewhat critical of the American technology behemoths; he has said that he would support stricter antitrust oversight and privacy rules.

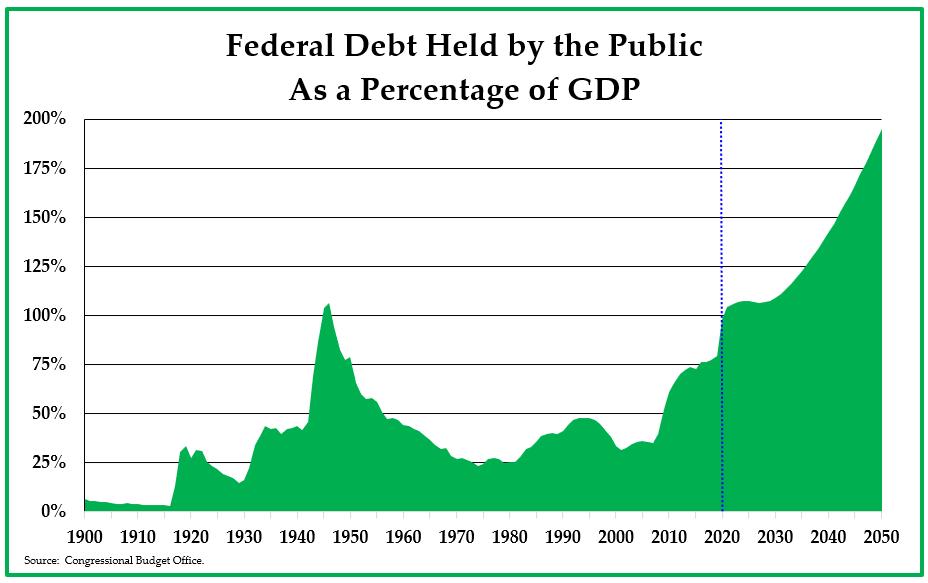

Third, both candidates are predisposed towards an increased government deficit. As shown in the graph to the right, the Congressional Budget Office has projected that public debt is on track to hit almost 200% of GDP by 2050 with no changes to tax or spending policies, a height currently achieved only by Japan in the developed world. If re-elected, we believe Trump would likely seek further tax cuts and a $2 trillion infrastructure spending program to stimulate the economy. In contrast, Biden has proposed that he would roll back Trump’s signature tax cuts while also supporting a more than $3 trillion recovery bill to address budget holes in state and local governments, grants and loans to small businesses, and climate-friendly infrastructure investments.

Fourth, regardless of the election, the Federal Reserve will almost certainly monetize increasing U.S. deficits by expanding its balance sheet to buy Treasuries with newly printed electronic money. The Federal Reserve’s dovish monetary policies are likely to result in near-zero interest rates during most if not all of the next presidential term and, relatedly, continued financial speculation along with an increased risk of higher inflation.

Economic Policy Divergences

To be fair, these are the primary economic commonalities between these two Presidential candidates; from an economic perspective, they stray from one another most significantly regarding taxes and regulatory oversight. Indeed, there is a myriad of other differences between Trump and Biden, but, again, the purpose of this analysis is to specifically highlight the major economic and market impacts associated with these candidates.

As previously mentioned, these two candidates are opposed to one another with regard to the tax policy. Trump wants taxes to remain low (or possibly go lower), and Biden wants the wealthy and corporations to pay higher taxes. We would reiterate that any tax change would require a bill passed by Congress.

During the Trump presidency, regulations generally have been loosened across the board. Whether the regulations entail oil drilling restrictions in the Arctic National Wildlife Refuge, financial compliance rules, manufacturing pollutant regulations, etc., the Trump presidency has cut red tape everywhere possible. Trump’s role has deregulation champion has made it easier for companies to conduct business and expand profits, albeit with negative externalities related to such loosened regulations. Should Biden become president, we believe he would likely reverse many of Trump’s regulatory changes.

Asset Class Impacts

Both Biden and Trump would try to enact policies that will inevitably impact the financial markets, but that impact would be felt over a far more extended period. In the face of COVID-19 and record-breaking deficits, the Federal Reserve has communicated that it is unlikely to raise interest rates for years, thus providing easy money for investors to speculate and for companies looking to expand. Regardless of who occupies the White House over the next four years, interest rates are likely to remain painfully low for years, and, therefore, returns from Treasury bonds are likely to be anemic.

Continued low corporate taxes and increased deregulation should have a marginally positive impact on earnings for U.S. companies. Thus, on the surface, one might come to the logical conclusion that a Trump presidency would likely be better for stock investment returns. However, the historical data provided above simply does not support that point. Stock returns over the next four years are far more likely to be driven by stretched valuations, weak demographic trends, Federal Reserve actions, the continued spread of COVID-19, productivity, inflation, and other factors that are simply out of control of one person. In our view, it is not possible to say with any certainty which presidential candidate would be better for the stock market.

Regardless of who the president is, we think gold prices should continue to grind upwards. As discussed in our last quarterly commentary, today’s environment remains conducive to rising gold prices. Helicopter money is falling at an accelerating pace, thus causing inflationary pressures that boost gold. On an inflation-adjusted basis, interest rates are negative and are poised to stay that way for years. Gold is under-owned by investors and offers significant portfolio diversification for investors.

In the final analysis, there are little data to base investment decisions on which candidate we think might win the White House or which party will likely control either house of Congress. We remain focused on making long-term investments in high-quality companies that are reasonably priced and creating specific asset allocations built around individual risk preferences and income situations. In the context of the health of the capital markets, the presidential race is mostly noise.

In the face of the COVID-19 global pandemic and the most chaotic, divisive election in years, we wish health, safety, and happiness to all of our clients. We thank you for your continued trust.

Pekin Hardy Strauss Wealth Management

[1] Source: Standard & Poor’s.

[2] Source: Standard & Poor’s.

This article is prepared by Pekin Hardy Strauss, Inc. (“Pekin Hardy”, dba Pekin Hardy Strauss Wealth Management) for informational purposes only. The information and data in this article do not constitute legal, tax, accounting, investment or other professional advice. The views expressed are those of the author(s) as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. There is no guarantee that the types of investments discussed herein will outperform any other investments in the future. Although information has been obtained from and is based upon sources Pekin Hardy believes to be reliable, we do not guarantee its accuracy. There are no assurances that any predicted results will actually occur. Past performance is no guarantee of future results. The S&P 500 Index is a widely recognized, unmanaged group of stocks that is representative of a broad market.