The COVID-19 pandemic is the most significant economic event since World War II, and the extent of its impact is still far from known. It will be months or possibly years before we can fully grasp the fallout of this global crisis. However, one thing is certain: more than ever, now is a time for financial prudence and sound decision-making. While asset prices have been punished and we expect markets to remain volatile, there are actions that investors can take to mitigate the financial risks that they face from the pandemic and even potentially benefit from the temporary effects of this event. In this Navigator, we discuss nine strategies that you can employ in the immediate term to better position yourself financially in this “new normal.” Though no one knows how long the pandemic will last nor how long it will take for society to resemble the one we remember, the recommendations we discuss in this Navigator may help you to better weather the economic storm ahead and potentially make material improvements to your long-term financial health.

Prudence in a Time of Panic: Nine Personal Finance Strategies for Today’s Uncertain World

Set forth below are nine actions that investors should consider taking in the near term to manage or even benefit from the impacts of the coronavirus pandemic. Some of the strategies we discuss may not apply to your personal situation, but we encourage you to read through each strategy and identify which, if any, may be beneficial to you.

Refinance Your Mortgage

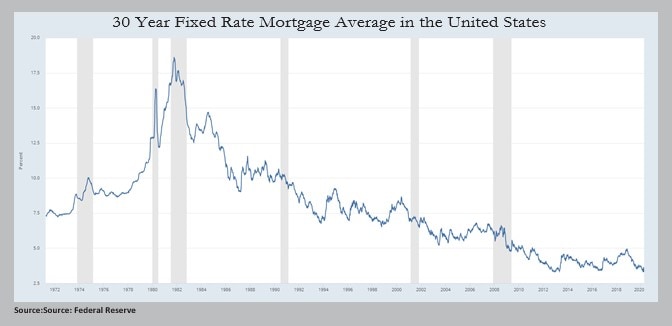

As the potentially devastating economic effects of the coronavirus started to become clear in early March, the Federal Reserve’s first response was to lower the federal funds rate in order to ease pressure on banks and encourage lending activity. The central bank lowered the federal funds rate on March 4th and again on March 16th, as policymakers became increasingly concerned about the fallout from the virus. One of the most visible effects of these Fed moves was an attendant drop in mortgage interest rates. Though mortgage interest rates were already low by historical standards, the Fed move in early March sent mortgage rates plummeting to all-time lows (see chart on next page).1 This represented a significant opportunity for new homebuyers and current homeowners alike to save materially on mortgage interest costs.

While mortgage interest rates have crept up marginally since the lows recorded in early March, rates remain very low. To be sure, not all loans are equal, and there are some stresses in the jumbo loan market, so these types of loans may be more expensive or more difficult to obtain.

Overall, if you are a homeowner with an outstanding mortgage loan and have not considered refinancing your mortgage, we encourage you to do so. While the rates currently available to you may or may not provide enough interest savings to justify the costs of refinancing, we believe it is prudent to consult your bank or mortgage broker sooner rather than later to inquire about rates and costs in order to determine if refinancing makes sense for you.2

Do a Roth Conversion

The sudden, swift, and steep decline in asset prices that began in late February and continued through March as a result of the COVID-19 pandemic has been painful and unnerving for investors. However, it has also created an opportunity for investors with pre-tax IRA assets to convert to Roth IRA assets while minimizing the associated tax impact.

An investor with pre-tax IRA assets who converts those assets to a Roth IRA while prices are depressed will owe less in taxes than if he or she converted those same securities while markets were still trading near all-time highs. As markets ultimately recover from this downturn, the converted assets can increase in value without the investor ever having to face any additional tax burden related to these assets. Furthermore, if you find yourself in a lower tax bracket in 2020 as a result of diminished income, then that may be another reason to convert a traditional IRA to a Roth IRA in the near term. If you have contemplated converting pre-tax IRA assets to Roth assets but have not followed through, now may be an especially opportune time to revisit such a strategy.

Make Stock Gifts

For investors who have a desire to gift assets in a tax-efficient manner, now may be a favorable time to do so while asset prices are down. Federal gift tax rules currently allow investors to make gifts of up to $15,000 per recipient per year without requiring that a gift tax return be filed with the IRS. Additionally, gifts that fall below the $15,000 annual limit do not count toward one’s lifetime gift tax exclusion. If you are looking to reduce the size of your estate by gifting assets but want to avoid exceeding the annual gift tax exclusion, doing so while asset prices are depressed could allow you to remove more assets from your estate without triggering gift tax reporting requirements.

Reassess Your Budget

The economic consequences of the COVID-19 pandemic are likely to be significant and broadly felt. However, the ultimate duration and severity of these consequences and their impact at the individual level remain unclear. Given this uncertainty, one of the most prudent actions you can take is to conserve cash by avoiding unnecessary expenses. We believe it is wise to revisit one’s budget periodically regardless of the economic environment, but now seems an especially appropriate time to examine your expenditures for potential cuts. Minimizing your discretionary expenses is a simple but highly effective way to protect yourself against the adverse effects of an economic downturn, and we strongly encourage you to go through this exercise sooner rather later.

We understand that reducing your spending is anything but easy. For most people, making sustainable spending reductions requires a shift in mindset. One approach to managing spending that we believe could be helpful for clients is a Japanese system called “Kakeibo,” which translates literally to “household financial ledger.” The system, developed more than 100 years ago by Japanese journalist Hani Motoko, emphasizes keeping a handwritten journal of all expenses, as well as approaching non-essential purchases deliberately and mindfully after considering a series of questions about each purchase. Approaching one’s finances using the Kakeibo system can help establish a clearer understanding of the motivation behind purchases and create a healthier relationship with one’s money. If you would like to learn more about Kakeibo, you can read about it here.

If you are simply unsure about how much you are spending, there are a number of tools that can help you track and analyze your spending. Our Wealth Center financial planning system has a robust budgeting tool, and there are many budgeting apps available for mobile devices that are either free or available for a nominal cost, including Mint, You Need a Budget, and Clarity Money, to name a few. You can also use this simple Excel budgeting template to help you think through and track your various expenses. Finding a system that works for you and getting a better understanding of your spending will go a long way toward helping you build a prudent, sustainable budget.

Increase Your Emergency Savings

In times of economic turmoil, cash is king. This is true for individuals and businesses alike. Just as businesses have been cutting costs and pulling on their credit lines in order to build their cash cushions, individuals should be looking for ways to increase their own cash cushions to better weather the current economic storm. In a “normal” economic environment, we typically recommend that clients keep three to six months’ worth of expenses in an emergency savings fund. For those who are at low risk of experiencing a loss of income as a result of the COVID-19 pandemic, this level of savings is likely still appropriate. However, for others whose incomes may be at greater risk, increasing their emergency savings to cover six to twelve months’ worth of living expenses may be prudent.

One of the best ways to increase your savings is to simply cut unnecessary expenses (see our previous recommendation on reassessing your budget) and set aside any resultant savings in your emergency fund. You may also consider delaying the purchase of certain items that are not immediate needs (such as clothes, household appliances, etc.) and funnel those dollars into your emergency savings instead. You could even defer retirement savings for a period of time in order to increase your liquid savings. We would simply caution you against missing your opportunity entirely to save for retirement in 2020. If you decide to defer retirement savings for a period, we strongly encourage you to revisit the topic later in the year and make up for any missed contributions if possible.

Forego Your Required Minimum Distribution (RMD) from Your IRA

In the past couple of weeks, we sent clients a series of communications outlining the various provisions of the CARES Act that was recently passed by Congress in response to the COVID-19 pandemic. One of the provisions that we discussed was the suspension of RMDs for 2020. Our previous communication provides important details about this temporary change and can be read here, but the key takeaway is that account holders or beneficiaries who would otherwise have been required to take an RMD in 2020 may forego their distributions entirely for the year. Given the clear tax advantages of IRAs over taxable accounts, it is nearly always optimal to leave assets in an IRA as long as possible. In addition, since RMDs count as taxable income whereas distributions from non-retirement accounts do not, we would advise you to forego your 2020 RMD if you are able to do so.

Obviously, we understand that many clients rely on distributions from their IRAs to meet various expense needs, and those clients should continue taking distributions as needed. However, clients who are able to meet their expense needs using sources other than their IRAs should take advantage of this opportunity to leave IRA assets untouched in 2020. In the coming weeks, we will be communicating with all clients who are affected by this change to determine their preferences regarding their 2020 RMDs.

Apply for a Paycheck Protection Program Loan

In addition to helping individuals and families deal with the fallout from the COVID-19 pandemic, the CARES Act also includes a number of provisions intended to help businesses of varying sizes. The Act targets small businesses, specifically, with the creation of the Paycheck Protection Program, or PPP. Administered by the Small Business Administration (SBA), the PPP is a forgivable loan program that is designed to assist small businesses with payroll and other operating expenses with the stated goal of reducing layoffs. Most businesses with fewer than 500 employees are eligible for the program, and loans through the PPP are forgivable if certain conditions are met. You can read more about the details of the program here.

If you are a small business owner or are self-employed, we strongly encourage you to consider applying for a loan under the PPP. Loan terms are highly favorable toward borrowers, and some or all of the loan may be forgiven based upon workforce retention. Loan applications are available through all SBA approved lenders. Small business owners and self-employed individuals should contact their banks to inquire about the program and begin the application process.

Revisit Your Asset Allocation

An investor’s risk tolerance consists of two interwoven parts: the ability to tolerate risk and the willingness to tolerate risk. The ability to tolerate risk is determined by an investor’s age, income, expenses, asset base, and a number of other concrete factors. It is an objective assessment of how much volatility an investor should tolerate in order to achieve his or her financial goals. The willingness to tolerate risk, on the other hand, is a subjective assessment of an investor’s psychological and emotional ability to cope with asset price volatility. This second part of the risk tolerance equation is where problems typically arise. Oftentimes, investors believe their willingness to tolerate risk is greater than it really is, and it is only in times of market turmoil that their true willingness to tolerate risk is revealed. These investors can only deal with upward price volatility. The recent volatility in the capital markets has likely revealed such a mismatch for many investors.

The intensity of the recent market sell-off was enough to shake even the most hardened market veterans. As an investor, it was nearly impossible to watch the market’s violent moves without experiencing some stress. However, while some degree of concern was warranted, investors whose asset allocations were appropriate for their individual risk tolerances should still have been able to sleep at night, despite Mr. Market’s spasms. Unfortunately, many investors likely found themselves worrying about their mounting portfolio losses over the past few weeks. If you fall into this camp, you should revisit your asset allocation and consider making changes so that your allocations properly align with your risk tolerance.

Review Your Financial Plan

One of the best ways to ease an anxious mind during economic and market upheaval is to create a financial plan or review your existing plan to ensure that it is complete and up to date. Though financial market performance typically commands the bulk of investors’ attention, we believe that having a sound financial plan and adhering to that plan over time is considerably more important for one’s long-term financial health than market performance. If you are interested in either creating a financial plan or reviewing a plan already in place, please reach out to your portfolio manager.

Closing Thoughts

It remains to be seen how long the U.S. economy will be shut down to combat COVID-19, but we strongly encourage you to consider implementing the strategies outlined above sooner rather than later. The attractiveness of certain strategies (e.g., mortgage refinancing) could change materially depending on market dynamics. Thus, we suggest you identify those strategies which are most applicable to your personal situation and consider discussing them with your portfolio manager in the immediate period ahead.

[1] https://www.housingwire.com/articles/mortgage-rates-fall-to-an-all-time-low/

[2] As a general rule, a 50-75 bps reduction in interest rate typically justifies refinancing, though closing costs and your duration in the home must also be considered.

This article is prepared by Pekin Hardy Strauss, Inc. (“Pekin Hardy”, dba Pekin Hardy Strauss Wealth Management) for informational purposes only and is not intended as an offer or solicitation for business. The information and data in this article does not constitute legal, tax, accounting, investment or other professional advice. The views expressed are those of the author(s) as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. Pekin Hardy cannot assure that the strategies discussed herein will outperform any other investment strategy in the future, there are no assurances that any predicted results will actually occur.