Personal Finance Strategies to Combat Inflation

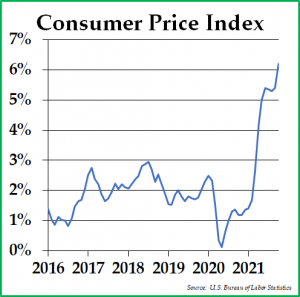

Inflation has risen significantly this year, and an increasing number of investors, including ourselves, expect inflation to remain high for at least the next three years. In a persistently high inflationary environment, there are steps that you can take as a consumer that reduce the deleterious impact of inflation on financial management and your household finances. As inflation rises, so too does the impact of inflation on financial planning decisions. In this Navigator, we suggest some of the best personal finance strategies that might allow you to reduce inflation’s bite on your family’s budget.

Inflation has arrived, and it does not appear to be going away anytime soon. Consumers are experiencing higher prices on food, gasoline, rent, and many other everyday goods and services. Many

families are modifying their investment strategies by allocating capital to real assets like apartment buildings or to hard currencies like gold and silver.

Setting aside investment strategies for a moment, how do you combat inflation as a consumer? In fact, there’s plenty that you can do. The question of how to handle inflation is one that we are increasingly receiving from clients.

As inflation changes, so do people’s time preferences for their money. If you expect inflation to be lower in the future, you are more likely to delay gratification by saving and investing your money for the future. Conversely, if you expect inflation to increase, you are probably more inclined to spend your money today, perhaps because you fear that your money may buy less in the future. As such, it may be well worth considering making some common-sense changes to your personal financial planning approach, ranging from the way you finance your home to the kind of automobile you purchase to the way that you buy your food.

Now, if you think inflation will not stay high and will fall back down to the 1% to 2% range where it remained for much of the past decade, it probably does not make sense to make any changes in your behavior. However, suppose you are concerned that price increases will stay above 3% on average and that real (inflation-adjusted) interest rates will remain negative. In that case, you may want to reconsider some of your financial planning decisions, while making sure that they reflect your individual financial situation and personal tolerance for risk.

- Buy Rather Than Rent:

In an inflationary period, the rent vs. buy decision generally favors buying over renting your home. When you are a renter, your landlord will likely hike your rent at the level of inflation when your lease comes due each year. This might be acceptable when inflation is low, but it is much less desirable when inflation is high. As a renter, your housing costs are unprotected from inflation. In contrast, there are two strong reasons to buy your home. First, as a homeowner, your mortgage payments can be stable with a fixed rate mortgage. Second, the replacement value of your home is likely to increase with inflation because the cost of land, materials, and labor are all rising with inflation. Being a homeowner helps to protect you from inflation.

– - Finance Your Home With A Mortgage:

Today, it is a terrible time to be a lender or a bond investor, as interest rates are not high enough to compensate investors for inflation. However, it is an ideal time to be a borrower, assuming that you do not take on more leverage than you can handle. If you get a fixed rate mortgage with a long maturity, you are using inflation to your benefit. Some homeowners are borrowing money for 30 years and paying less than 3% per year in interest expenses; moreover, these homeowners are also benefiting from the potential tax deduction on interest expenses. However, the very best thing about a mortgage is that the inflation-adjusted value of your mortgage payments declines as inflation rises.

– - Get An Auto Loan

Interest rates on auto loans are also low right now. If you expect inflation to remain high, it makes sense to finance your car purchase for the same reasons it makes sense to finance a home purchase. Just make sure to seek out fixed-rate loans extended as far as possible. If you can get an interest rate below 3% and borrow responsibly, you will end up paying off your debt in the future with cheaper dollars.

– - Improve Your Energy Efficiency

If you own a car that uses a lot of gasoline, you should get ready psychologically and financially for higher prices at the gas pump in the future. You might want to think about reducing your future gasoline bills by purchasing a car that is more fuel-efficient or, even better, runs on electricity. At home, you could consider installing solar panels to reduce your future electricity bills. To reduce your heating and cooling costs, you have other levers to pull, such as sealing your windows and doors, installing high-efficiency lighting, or purchasing a learning thermostat to optimize your heating and cooling. Energy efficiency projects will help to mitigate the rising costs of energy.

– - Prepare For Shortages

Shortages are common in inflationary environments. For that reason, you may want to consider creating and maintaining an emergency supply of non-perishable food and other essentials for periods when stores cannot resupply themselves. Yes, this includes buying surplus toilet paper, but it also means stocking up on canned goods and other non-perishable items that you can find on sale. Fortunately, with prices rising quickly in the face of low interest rates, buying emergency supplies can represent a high interest rate savings vehicle: the likelihood is that the prices of goods will increase at a much faster rate than the interest rate on your checking account.

– - Buy Longlasting, Durable Products

When you are looking to purchase a durable good, such as a washer or dryer, buy a quality product that will not likely need to be replaced or serviced anytime soon. Although your purchase price might be higher, the investment could result in lower total expenditures over the period of your ownership.

– - Follow A Budget

Put together a budget and focus especially on the expense categories that inflation might affect most acutely in the future such as transportation, food, utilities, education, and healthcare. Think about ways to stretch your budget further, such as shopping at less expensive stores or bulk stores like Costco. Also, consider expenses that you can cut or reduce without affecting your quality of life.

While consumers may dread inflation, it is possible to prepare for it. If you believe that inflation is going to increase or just remain high, you can help mitigate its effects by making significant purchases now, taking on reasonable amounts of debt at low interest rates if possible, and preparing your home and your family for cost increases. You cannot control how inflation rises and falls, but you can control your own financial decisions and make choices today that will help you manage inflation tomorrow.

We invite you to discuss your concerns about inflation and ways to reduce inflation’s impact on your household with your Pekin Hardy Strauss advisor. As we said earlier in this note, there are risks to making financial planning decisions to reduce your exposure to inflation. By trying to combat inflation, you could easily create other problems. We can help you understand the risks and make a more informed decision which makes sense for your particular circumstances. Please schedule a meeting with your advisor if you would like to explore this topic further.

This article is prepared by Pekin Hardy Strauss, Inc. (“Pekin Hardy”, dba Pekin Hardy Strauss Wealth Management) for informational purposes only. The information and data in this article does not constitute legal, tax, accounting, investment or other professional advice. The views expressed are those of the author(s) as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. Pekin Hardy cannot assure that the strategies discussed herein will outperform any other investment strategy in the future. The Consumer Price Index (CPI) is an unmanaged index representing the rate of the inflation of U.S. consumer prices as determined by the U.S. Department of Labor Statistics.