“Winter is coming.”

─ Ned Stark, “Game of Thrones”

In the investment world, “winter” can be viewed as a synonym to recession, and, technically, winter is always coming at an uncertain point in the future. However, a number of recent economic signals highlight concerns that winter may be coming sooner rather than later, even though we most certainly do not have a crystal ball to forecast exactly when winter will come nor how severe it may well become.

We have been closely watching the economic indicators and trends provided below:

- Inflation is hitting consumers hard.

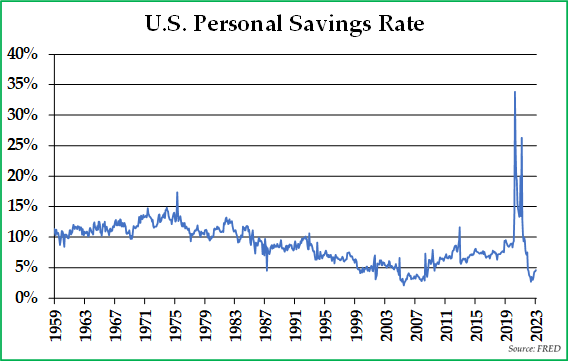

Since 2021, prices in the United States and elsewhere in the developed world have risen at a mid-to-high single-digit clip. The world is paying more for the same amount of goods and services and yet getting less for their money. In short, the quality of living has diminished with lower consumer purchasing power. Across the board, savings rates have fallen in the face of inflation, making the average person less prepared for financial emergencies, forcing many to rely on expensive loans or credit card debt to address unexpected expenses. Demand for discretionary items is falling, which should dampen economic growth.With inflation squeezing the economy, consumers are more reliant on credit cards to afford increasingly expensive necessities like rent and food (and pricey discretionary items as well). As a result, total U.S. credit card debt spiked to a record $931 billion at the end of 2022, an 18.5% increase relative to 2021.1 Juxtaposed against this increased credit card debt is an unemployment rate that stands at a 53-year low, yet credit card delinquency rates are rising.The personal savings rate, which is an important component of the financial security of U.S. households, measures how much of Americans’ disposable income remains after spending on food, rent, debt, and bills. As demonstrated in the chart at the top of the next page, the personal savings rate stands near all-time lows, reflecting the financial struggles of the average household. While some Americans are temporarily draining their savings by spending more to enjoy life post-lockdown, others are reducing savings to cover essentials because their wages simply are not maintaining pace with inflation.

- Noteworthy bank closures are inciting fears.

In March, the rapid shut-down of Silicon Valley Bank, Silvergate Capital, and Signature Bank, along with the take-under of 166-year-old Credit Suisse, stoked concerns about the health of the banking system. In response, regulators took surprisingly aggressive steps to stem the contagion. Additional banking regulation and increased expenses for the banks are in the queue, thus placing incremental obstacles for credit formation and economic growth. Moreover, instability in the financial services sector negatively impacts the allocation of resources as well as the assessment and management of financial risks.

- Corporations are tightening their belts.

Despite the well-publicized difficulty of hiring over the last few years, even highly profitable companies like Apple, Goldman Sachs, McKinsey, and Disney have announced material cuts in their respective, highly paid workforces. In February 2023, the U.S. Bureau of Labor Statistics announced that there were just 9.9 million job openings; this report represented the first sub-10 million print since May 2021 and was 1.3 million lower than the December 2022 print. Moreover, companies are tapping the breaks on capital spending with particular weakness in more economically sensitive sectors; essentially, corporations are signaling that they are preparing for muted demand and pressured profit margins.

– - The return of student loan payments looms ominously.

During the coronavirus pandemic, the Federal government issued regulations that allowed student loan payments to be temporarily paused. Ceased student loan payments are set to resume in September 2023, which will impact aggregate discretionary spending with more capital directed towards debt paydown. Notably, certain cohorts of Generation Z have never made a single debt repayment in their lives, and those people should feel this loss of discretionary capital more acutely than most.

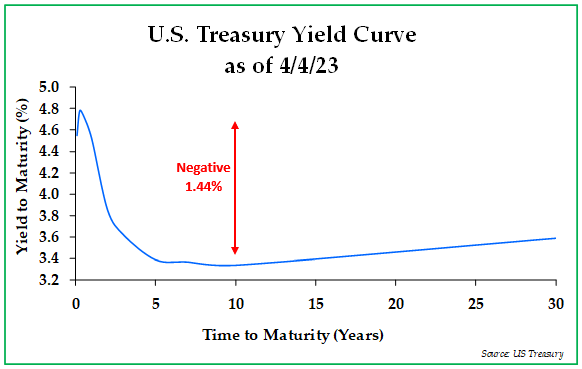

– - The inverted yield curve portends an ominous future.

The yield curve is a chart that plots the interest rates of a specific type of debt at differing maturities. The slope of the yield curve is normally upwards sloping, which indicates that investors require more return to invest capital for a longer period. Typically, an upward sloping yield curve shape indicates stable economic conditions.An inverted yield curve occurs when short-term interest rates exceed long-term rates, which is unusual because investors normally would not require a higher return to tie up their capital for shorter periods of time. As of April 4, 2023, the 90-day to 10-year U.S. Treasury yield spread stood at negative 1.44%, which is quite wide as compared to historical norms. Notably, an inverted Treasury yield curve has been one of the most reliable leading indicators of an impending recession.2

The current shape of the yield curve has serious implications for credit formation. With the Fed Funds target rate currently at 5% and banks’ estimated earnings yield on assets below that rate, depositors are moving capital to money market funds, and banks are responding by tightening their lending standards.

– - The Federal Reserve’s posture remains hawkish.

Despite the recent banking turmoil, the Federal Reserve raised the Fed Funds interest rate by another 0.25% in late March, pushing forward with its aggressive campaign to rein in inflation. Federal Reserve officials are now forecasting just one more interest rate increase this year but doing so with an increasingly uncertain tone. These interest rate increases slow economic activity, as they drive up the cost of credit for credit cards, adjustable-rate mortgages, and other variable loans.Moreover, in June 2022, the Federal Reserve began to passively shrink its assets as the underlying securities on its balance sheet matured — a process called Quantitative Tightening, which drains liquidity out of the financial system. The objectives of Quantitative Tightening are deflationary in nature and are similar to that of raising borrowing costs because it cools down an overheated economy by reducing the amount of money in circulation.

– - The U.S. stock market performance is increasingly narrow.

During the first quarter of 2023, investors rotated back into the beaten-up stocks of technology giants like Apple and Nvidia, leading to massive price gains in the worst-performing sector of 2022. Despite significant volatility, defensive stocks suffered, as stocks in consumer defensive, healthcare, and utility sectors all ended the quarter with losses. Plus, the energy sector, which led the stock market in 2022 by a large margin, was the worst-performing sector of the stock market. The narrow nature of the recent stock market moves is rather perplexing and is likely indicative of unhealthy, anemic growth as well as a possible recession looming. If the economy was exhibiting healthy growth, then the move in the stock market would be far more broad-based in nature.

– - The Federal debt ceiling simply cannot be breached.

Created by Congress in 1917, the debt ceiling is the approved debt limit for the U.S. government, which now stands at $31.4 trillion. The U.S. Treasury reached the current limit earlier this year, so it has no room to borrow incremental capital, other than to replace maturing debt. Further, Treasury Secretary Janet Yellen is pursuing “extraordinary measures” to keep the government funded. Bumping against the debt ceiling is not necessarily a new issue, as the debt limit has been increased many dozens of times over the years. Both political parties all too often engage in contentious battles with regards to this issue, usually about spending and taxing priorities.We expect that a debt ceiling agreement will be reached after significant negotiation. However, in today’s highly polarized political environment, it could be a publicly contentious process that could exacerbate market volatility and weaken confidence in the economy. Given that the Federal Reserve is trying to tame inflation, a protracted debt ceiling battle that undermines confidence would be counterproductive.

On the other side of this dizzying myriad of headwinds, certain countervailing forces play roles in positively impacting the economy. Next year is an election year, and Congress and the Executive branch will likely use fiscal policy to stimulate the broader economy in order to attract votes. Also, Federal Reserve Chairman Jerome Powell might have to reverse course in its monetary tightening campaign if financial instability increases sufficiently. While it is a backward-looking economic indicator, unemployment rates do stand near all-time lows. In our view, despite these possible countervailing forces, we believe that a recession beginning later this year is more likely than not.

Our client portfolios are generally positioned defensively in light of this bearish outlook on the economy. With regards to equities, we are favoring companies in the consumer staples, healthcare, and agriculture sectors as well as inexpensive, out-of-favor value stocks. We are also overweight energy stocks due to a significant mismatch that we see between expected supply and demand.

Beyond equities, our client portfolios are generally overweight short-term U.S. Treasuries and physical gold trusts. We own Treasuries because, in the current environment, yields have become attractive for the first time in over a decade. We own gold because gold should help to reduce portfolio volatility and is likely to perform well in an environment where inflation remains persistently elevated even while real growth is slowing.

*****

We thank you for your continued support in asking us to manage your investable assets. Should you have any questions about the contents of this letter, please do not hesitate to reach out to us.

Sincerely,

Pekin Hardy Strauss Wealth Management

1 Source: TransUnion.

2 https://www.chicagofed.org/publications/chicago-fed-letter/2018/404.

This commentary is prepared by Pekin Hardy Strauss, Inc. (“Pekin Hardy”, dba Pekin Hardy Strauss Wealth Management) for informational purposes only. The information and data in this article do not constitute legal, tax, accounting, investment or other professional advice. The views expressed are those of the author(s) as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. There is no guarantee that the types of investments discussed herein will outperform any other investments in the future. Although information has been obtained from and is based upon sources Pekin Hardy believes to be reliable, we do not guarantee its accuracy. There are no assurances that any predicted results will actually occur. Past performance is no guarantee of future results.