The purpose of this navigator is to show the effects working longer has on increasing retirement income. We highlight some eye-opening statistics. Pekin Hardy Strauss recognizes that every client is unique and should consider the current state of their financial situation and well-being when deciding if they should continue working.

When Should I Retire

We work most of our life hoping to someday retire and enjoy the decades of hard work. Retirement is a difficult decision, no matter who you are or what you do. Many factors play a role in deciding to retire. Common reasons are health, financial capacity, workplace culture, buyout offer or simply being burnt out. In this navigator, we will look at why working longer is helpful to secure retirement income.

Benefits of Continuing to Work Full-Time

Thinking you should have saved more may not be as big of an issue as you think. Working longer has more of an influence on retirement income than saving, in most cases. In 2018, studies from the National Bureau of Economic Research on The power of Working Longer1 have shown that working only 3 months longer has the same impact as a 1 percent increase in savings, over a 30-year period.

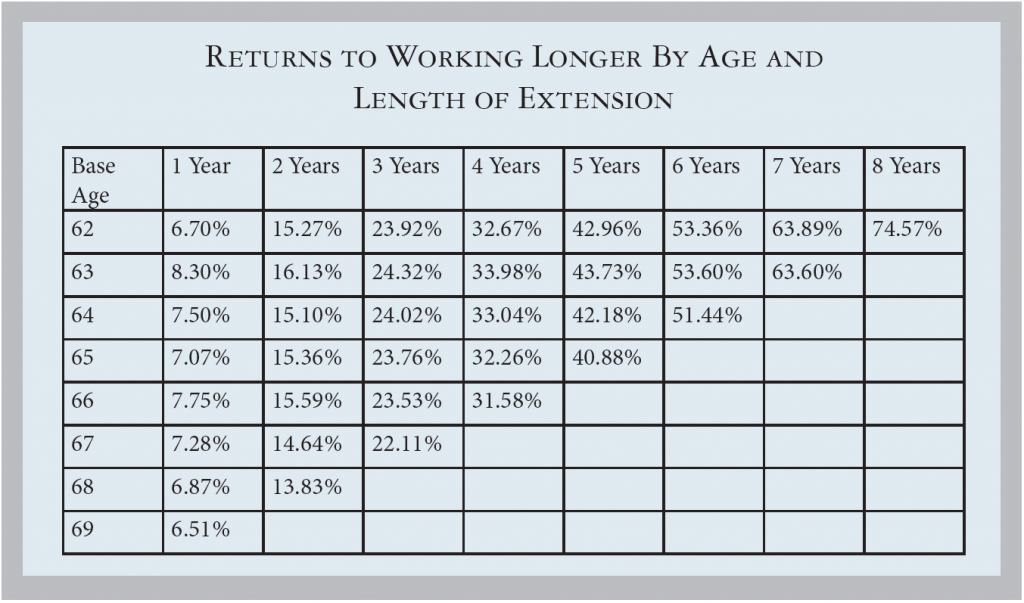

To visualize how working longer influences retirement income, let’s look at one of the National Bureau of Economic Research studies on the percentage increase of income by working 1 to 8 years longer and delaying Social Security. The first column presents the percent increase in retirement income resulting from working one extra year and delaying Social Security by one year for primary earners of age 62 through 69.

For example, if you originally planned to retire early at age 62, but decided to work for another year, your retirement income would increase by 6.7 percent. If you worked until age 67, your retirement income would increase by 42.96 percent.

Full retirement age (FRA) is between 66 and 67 depending on when you were born. By working an additional year beyond full retirement, you can boost your retirement income by more than 7 percent. If FRA is 66, working until age 70 creates a whopping 31.58 percent increase in retirement income, and 22.11 percent if FRA is 67.

Part-Time/Gig Work

Working part-time when nearing retirement is a beneficial option, and is even considered a hobby for some. It does not hold the same weight as continuing to work full-time, but it still has major benefits compared to completely calling it quits.

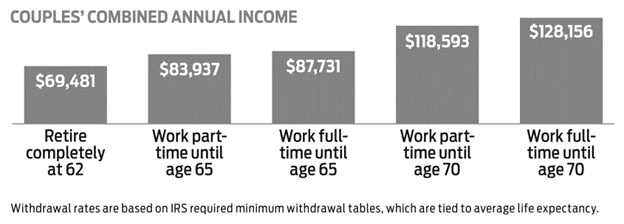

In 2017 the Stanford Center of Longevity and the Society of Actuaries analyzed the projected income of a 60-year-old married couple with a combined household income of $200,000 and retirement savings of $1 million. The annual income is made up of Social Security benefits and a yearly withdrawal rate based on life expectancy (generally 3% to 4%). The numbers are derived from the assumption that a couple will contribute 15% of their income each year while working full-time and nothing while working part-time. It also considers a 3% annualized return on savings.

The numbers above illustrate that working part-time until 65, instead of retiring at age 62, can generate an extra 20% of income and a 70% increase if you do so until age 70. The additional income and compounding effect are powerful on retirement income security.

Married Working Couples

If you and your significant other are both working, staggering retirement is a useful tactic. By retiring at different times, you can minimize or completely rid drawdowns from your portfolio and keep the option of employer-sponsored healthcare. The person/individual who decides to continue working should also continue to contribute to their retirement savings as much as possible.

While household income from employment is still flowing, there should be higher scrutiny placed on expenses during this time. The amount of income can be significantly less than when both were working. Adjusting leisure costs, when necessary, will help bridge the gap.

Pre & Post Retirement Income

The amount of time and money you spend in retirement could jeopardize your retirement income security. Your income replacement ratio, an estimation of what percentage of a person’s retirement income will be needed to maintain their lifestyle at retirement, will be a key driver in determining your retirement income. Comparing your income replacement ratio to how much your portfolio and other retirement income can provide in retirement will help determine your decision to work longer. Your income replacement ratio estimates what percentage of pre-retirement income you’ll need to maintain your lifestyle in retirement. On average it is expected that one will need 70 to 85 percent of pre-retirement income to cover expenses in retirement. If you plan to travel more frequently, or are planning a big purchase, while retired, this amount may not suffice. Conservatively speaking, you should expect to spend the same as you did pre-retirement. For portfolio withdrawals in retirement, there is a general rule to help determine how much you should spend: 4% of your portfolio the first year and adjusting for inflation every year. However, this 4% figure is not concrete and should be used as a starting point when deciding the feasibility of withdrawals.

Overall Well-Being

Not only does working longer boost your retirement income, but it also carries many health benefits. We all want to live a healthy and happy life and the age when you retire can influence your quality of life. Working helps stimulate the brain and keeps social engagement a part of your everyday life. In 2015, the CDC published a journal from a study of 83,000 older adults over a 15-year span2. It compared people who retired before age 65 and after. People who worked past the age of 65 were about three times more likely to report being in good health. Not only were they considered to be in good health, but they were also half as likely to have major health complications such as cancer or heart disease down the line. However, if you do not find what you’re doing to be interesting anymore, or are burned out, this may add stress and affect your mood. It is important to know yourself physically and mentally when making the decision to retire.

Other Considerations

Unexpected expenses can be detrimental to retirement income. Many times, retirement plans are negligent in creating a buffer in retirement income for unexpected liabilities. 19% of retirees and 24% of retired widows experience four or more shocks in retirement, according to the Society of Actuaries3. Illness and disability, major home repairs/upgrades, costly dental procedures, and other out-of-pocket- medical expenses. The additional income from an extra year(s) of working before retirement can be used as a rainy day fund that can ease these unexpected retirement expenses.

Meeting with an advisor can help formulate the decision of when to retire and create peace of mind. Everyone is unique. There may be other factors to this decision that were not mentioned. We encourage you to reach out to discuss this matter. We provide an intuitive modeling system that allows us to consider many “what-ifs” and how they could affect your retirement plan.

1 The Power of Working Longer

2 Working Later in Life Can Pay Off in More Than Just Income

3 Shocks and the Unexpected: An Important Factor in Retirement

The commentary in this video and article was prepared by Pekin Hardy Strauss, Inc. (“Pekin Hardy”, dba Pekin Hardy Strauss Wealth Management) for informational purposes only (and is not intended as an offer or solicitation for the purchase or sale of any security.) The information and data in this article and video do not constitute legal, tax, accounting, investment or other professional advice. The views expressed are those of the author(s) as of the date of publication of this report and video, and are subject to change at any time due to changes in market or economic conditions. The comments should not be construed as a recommendation of individual holdings, market sectors or any particular strategy, there is no guarantee that the strategies discussed herein will outperform any other. Although information has been obtained from and is based upon sources Pekin Hardy believes to be reliable, we do not guarantee its accuracy. There are no assurances that any predicted results will actually occur.