“Only when the tide goes out do you discover who’s been swimming naked”

─ Warren Buffett

Last year we made our first attempt at providing 10 investment-related predictions for the upcoming year, and we are going to repeat the process for 2023.

Before starting with our 2023 predictions, we want to take a moment and review how our 2022 predictions panned out. Overall, about half of our 2022 predictions came true, while half of our predictions proved to be incorrect. We predicted a weak stock market, the popping of the meme stock bubble, outperformance by gold, increasing energy prices, rising food prices, and Republicans winning back control of Congress, all of which turned out to be correct. On the other hand, we also predicted that inflation would start to ease in the first half of the year, that cannabis would be legalized at the Federal level, that cryptocurrency applications would continue to grow, that U.S. stocks would underperform the rest of the world, and that Democrats would lose control of the Senate. These prognostications turned out to be incorrect. We also missed a prediction that significantly influenced 2022, which is the Russian invasion of Ukraine and the subsequent Western sanctions placed on Russia in response, all of which made inflation worse than we expected and caused the Federal Reserve to hike rates for higher and longer than we expected.

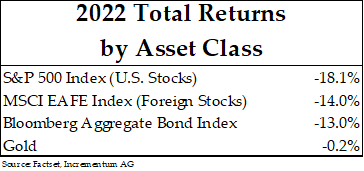

Overall, 2022 was a rather difficult year for investors with geopolitical turmoil, painfully high inflation rates, tightening monetary policy, and double-digit declines in both the stock and bond markets. The S&P 500 Index posted its worst year since 2008, while the return of the 10-year Treasury bond posted its worst year going all the way back to 1788! And overall, for balanced portfolios, 2022 was one of the worst years over the last 100 years. We wish we could be here to suggest that the investment clouds are about to part, but our job is to provide realism rather than optimism. On that note, we are bracing for continued broad market declines, at least during the first half of 2023. Inflation is still far too high, geopolitical turmoil remains very concerning, the Federal Reserve is still tightening monetary policy, and a looming U.S. recession seems increasingly likely.

More specifically, below is the list of our 10 predictions for 2023, knowing all too well that many of these will prove to be incorrect.

- U.S. Recession

During the first half of 2023, a U.S. recession begins, leading to significant layoffs which spread from the tech industry to Wall Street and eventually across the entire economy. Companies seek to reduce costs in the wake of lower share prices, weak consumer demand, and significantly higher interest costs. As layoffs increase, the unemployment rate rises to above 6%, while the U.S. budget deficit expands to more than 10% of GDP due to weakening tax revenues.

- Elevated Energy and Food Inflation

Oil prices jump to above $100/barrel during 2023. Oil demand is flattish in 2023 due to a weak economy, but oil prices remain surprisingly resilient due to declining supply. Weak consumer and corporate demand in the West is offset by rising demand for energy out of China due to its economy reopening and by the U.S. government becoming a buyer of oil as it seeks to replenish its strategic petroleum reserve (“SPR”). The oil sector outperforms again, and a nuclear power renaissance becomes increasingly apparent as new nuclear plant permits increase globally at a double-digit rate. Due to rising energy and fertilizer prices and continued low grain stocks, food prices continue to rise in 2023, up 10% vs. 2022.

- The Federal Reserve Pauses and the Pivots

The Federal Reserve stops raising interest rates once inflation drops to 5%, despite meaningful price increases in food and energy that are partially offset by a steep decline in used car prices. While intending to keep interest rates flat, the Federal Reserve finally capitulates during the second half of 2023 and gradually reduces interest rates even while it restarts Quantitative Easing (printing money to buy bonds) again to cap long-term interest rates and fund the U.S. government.

– - Bear Market in U.S. Stocks Finds a Bottom

A bear market in stocks continues during the first half of 2023, with the S&P 500 dropping to 3,000 once it becomes evident that the U.S. economy is in recession with significant declines in corporate earnings. The stock market weakness, which began with meme stocks and spread to technology stocks in 2022, finally pulls down the blue chip companies of the Dow Jones Industrial Average during 2023. With that said, we expect technology stocks to materially underperform again in 2023.

– - Bond Yields Decline, Supporting the Housing Market

Bonds perform reasonably well, resulting from U.S. Treasury bonds outperforming equities as bond prices rebound from a historically poor 2022. At the same time, mortgage rates fall to below 5%. During 2023, house prices decline by double digits in a few regions of the United States, but nationwide house prices remain surprisingly resilient, falling by less than 5% in 2023.

– - Office Market Distress

The commercial (office) real estate market experiences extreme distress; many buildings are sold for far less than their purchase price from several years ago, while other property owners find they are unable to roll their debt. Office occupancy remains below 50% as workers refuse to return to the office on a consistent basis.

– - Significant Congressional Spending

In response to recessionary pressures, Congress passes a bi-partisan, multi-trillion-dollar spending bill. The spending focuses on “anti-inflation” measures involving significant subsidies for utility bills, grocery bills, and gasoline bills. Ironically, inflation starts to re-accelerate soon after the bill becomes law. The spending measures put pressure on the dollar and force the Federal Reserve to take steps to improve the functioning of the Treasury market.

– - Ukraine Cease-Fire

Russia and Ukraine agree to a stand-off; their agreement is not exactly peace, but an uncomfortable cease-fire with newly arranged borders. Putin claims victory and that his goals were met, albeit at a high cost. President Biden’s rhetoric mirrors that of Putin. Russia remains a global pariah, but it continues trading with China and India and others interested in buying its commodities.

– - Global Trade De-Dollarization

A significant increase in the share of global trade is executed in non-dollar currencies during 2023. India, China, and even Japan increase their purchases of oil and gas with rupees, yuan, and yen. Europe becomes increasingly dependent on the United States for its energy supplies and, instead of drawing Europe and the United States closer, Europe bristles under the high costs of imported U.S. energy, and the alliance begins to fray.

– - The Dollar Declines, While Gold and Emerging Markets Rise

The U.S. dollar weakens against a basket of global currencies due to U.S. deficit spending, a reacceleration in the money supply, and foreign central banks maintaining a tighter monetary policy than the Federal Reserve during 2023. With a weakening dollar, the gold price rises above $2,100 per ounce, and emerging markets outperform. Central banks purchase even more gold during 2023 than they did in 2022.

The year could turn out to be better than these somewhat dire predictions might suggest. On the other hand, it could turn out to be worse. During periods of economic uncertainty and monetary tightening, such as is the case now, it’s often a good time to run more conservative portfolios. We still think there is too much greed in the market and not enough fear. At the same time, during periods of high inflation, such as is also the case now, it’s often a good time to own an oversized position in commodities and other hard assets.

Given our prognostication of uncertainty and continued food and energy inflation, it may make sense to own an oversized position in both hard assets and cash/short-term bonds heading into 2023.

Importantly, one year is not a particularly long investment time horizon. Our investment approach is long-term and guided by fundamental factors that go far beyond 2023, such as:

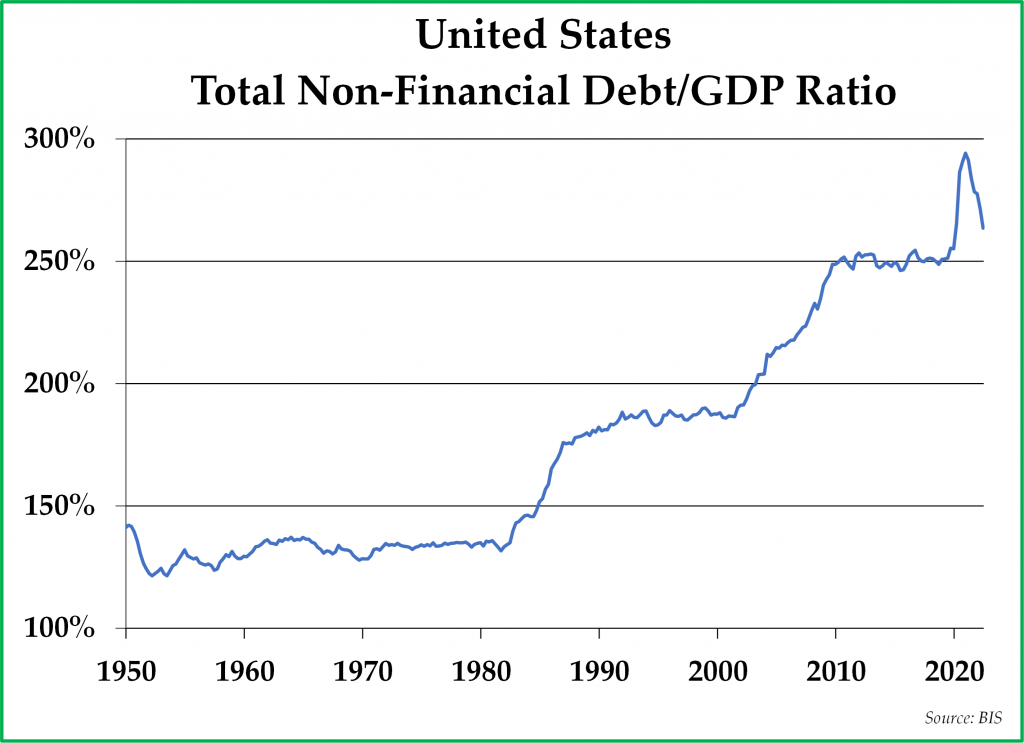

- U.S. indebtedness across the household, corporate, and government sectors is at record high levels (see chart to the right). Working off this debt will require time, elevated inflation, low real (inflation-adjusted) interest rates, and debt restructurings.

- The global economy is in the early innings of a secular bull market in commodity prices that began in 2020. Commodity bull markets usually last a decade or more and do not end until companies over-invest in future commodity production.

- Even after the declines of 2022, U.S. stocks generally remain expensive relative to history and have further room to deflate. It is likely to be a good time to be a stock picker, and it is likely to be a poor time to own passive indices of U.S. stocks.

– - As Warren Buffett put it, price is what you pay for an investment, but value is what you receive. With inflation high and interest rates rising, we believe the next few years should present excellent prospects for disciplined value investors.

We are certainly mindful of the short-term risks in the economy and the financial markets, and we are also well aware of the long-term fundamentals that should drive the markets over the next five years. Most importantly, we are allocating your capital with prudence, price discipline, and a focus on managing risk.

*****

We send you and your families best wishes for a happy, healthy, and prosperous 2023. We appreciate your trust in our stewardship of your capital and will be working very hard this year to maintain that trust.

Sincerely,

Pekin Hardy Strauss Wealth Management

This commentary is prepared by Pekin Hardy Strauss, Inc. (dba Pekin Hardy Strauss Wealth Management, “Pekin Hardy”) for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any security. The information contained herein is neither investment advice nor a legal opinion. The views expressed are those of the authors as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. Although information has been obtained from and is based upon sources Pekin Hardy believes to be reliable, we do not guarantee its accuracy. There are no assurances that any predicted results will actually occur. The S&P 500 Index includes a representative sample of 500 hundred companies in leading industries of the U.S. economy, focusing on the large-cap segment of the market. The Bloomberg US Aggregate Bond Index is a broad benchmark index for the U.S. bond market. The index covers all major types of bonds, including taxable corporate bonds, Treasury bonds, and municipal bonds. The MSCI EAFE Index is an equity index which captures large and mid cap representation across 21 Developed Markets countries. Past performance is no guarantee of future results.