Photo by tamayura39

“Do I contradict myself?

Very well then I contradict myself,

(I am large, I contain multitudes.)”

− Walt Whitman, Song of Myself

As the S&P 500 Index reaches all-time highs with an extraordinarily high valuation by most measures, how can the 10-year Treasury bond yield simultaneously be declining towards all-time lows? Usually, stocks go up when investors are increasingly bullish about the economy, while Treasury bond yields typically fall when investors are increasingly bearish about the economy and inflationary prospects, but rising stock prices and falling bond yields are both happening at the same time today. The apparent contradiction is difficult to reconcile.

It may well be that we are witnessing a temporary anomaly which occasionally surfaces in the financial markets. For example, oil prices skyrocketed to $144 per barrel in 2008 at the same time that the housing bust and the financial crisis were starting to accelerate. How could oil prices have risen to record highs just as aggregate demand was falling off a cliff? That anomaly corrected a few months later when oil prices declined by more than 75% to $34 per barrel.

Just as the oil price surge in 2008 turned out to be a temporary phenomenon, the conflicting signals between the stock and bond markets today may also be a short-term anomaly. If the stock market is correct and the bond market is mistaken, then bond yields should start to increase. On the other hand, if the bond market is right, and the stock market is wrong, a correction in the stock market would likely be coming soon.

However, what if it is not an anomaly?

The Bond Market

A fundamental axiom of bond investing is that when bond prices increase, ceteris paribus, bond yields decline. Similarly, when bond prices fall, bond yields rise. Needless to say, this relationship can be somewhat counter-intuitive. From November 2018 through June 2019, 10-year U.S. Treasury yields declined from 3.23% to 1.99%, which is the lowest yield for 10-year Treasuries since 2016, a year in which 10-year Treasury yields hit a new all-time low of 1.36%. It seems strange for yields to compress in the face of a rising stock market, but several reasons could explain this phenomenon:

- Increasing Recession Concerns

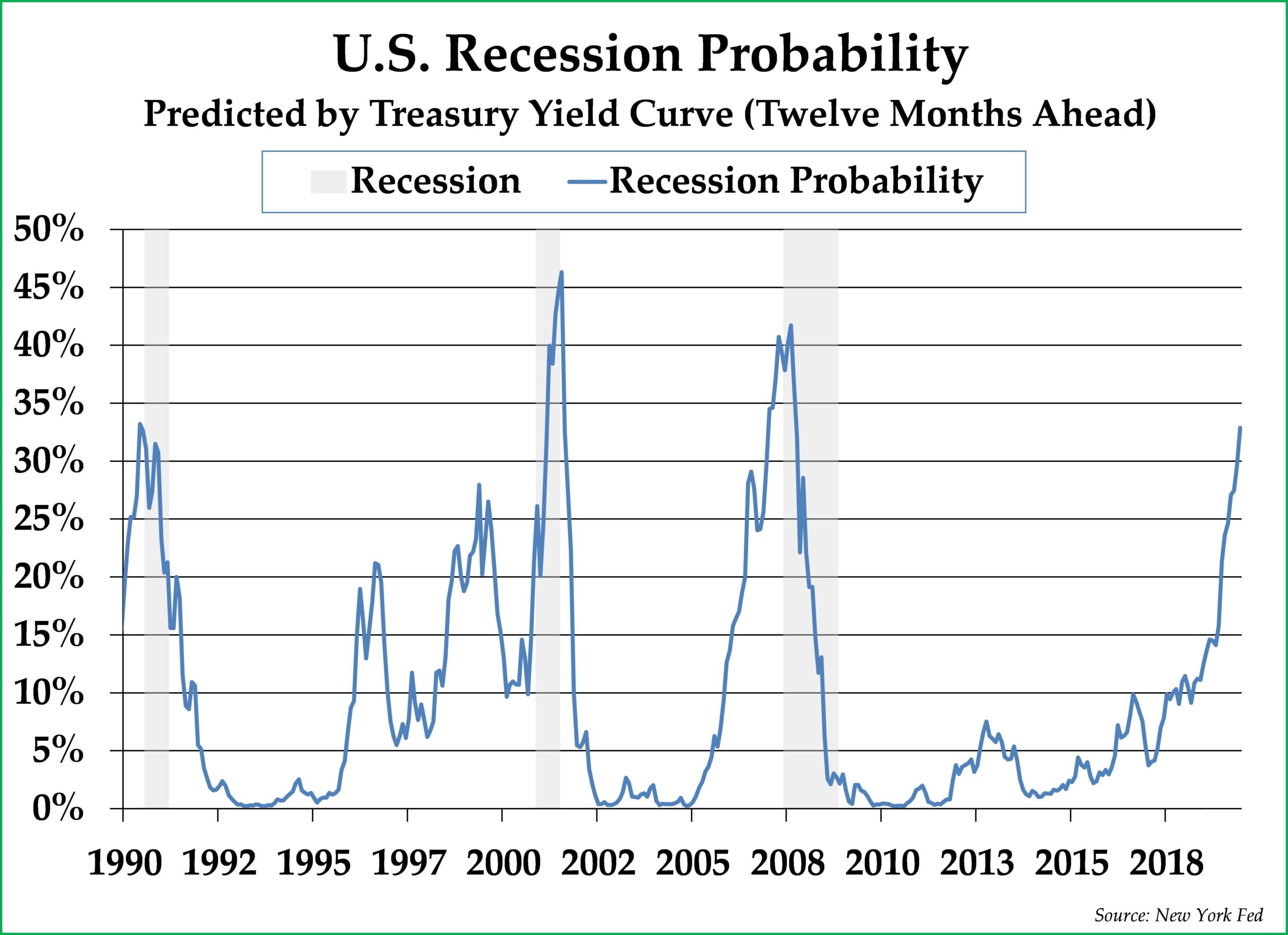

Investors tend to buy U.S. Treasuries when they think a recession is imminent. The Treasury yield curve, which is currently inverted, is warning that a recession might be coming; the Federal Reserve Bank of New York uses the yield curve as an indicator to estimate that the chance of a recession within the next 12 months is as high as 33% (see chart to the right). The longer the yield curve remains inverted, the more likely it is that a recession is soon coming. Besides the inverted yield curve, which we wrote about in detail during our Q1 letter, other signals are also suggesting that the U.S. economy is, at the very least, slowing down if not approaching a recession. With growth slowing and the increasing possibility of a recession ahead, investors might be increasing their allocation to U.S. Treasuries, driving bond prices up and yields down.

- Increasing Pool of Retiree Investors

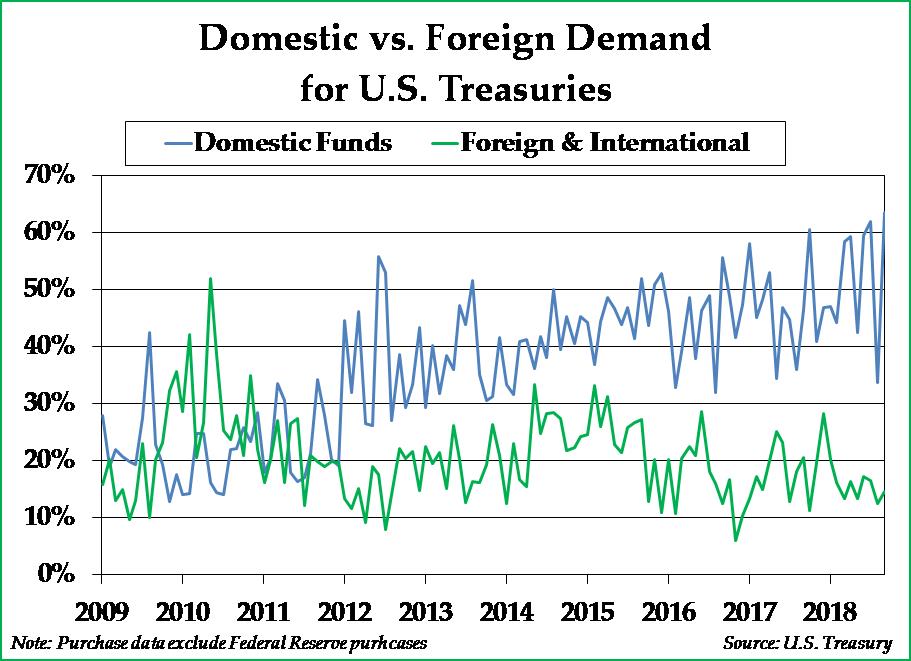

As the U.S. population ages and 10,000 new baby boomers enter retirement daily, investor demand for safety and yield should continue to increase. Retiree investors are less inclined to own an oversized allocation to risk assets like stocks, opting instead for U.S. Treasuries and other less volatile assets. As demonstrated in the chart below, domestic investors have been purchasing an increasing share of U.S. Treasury auctions. It is possible that the strength in bonds recently is partly attributable to increasing demand by domestic investors who are aging and seeking a safe haven, although it is difficult to understand why domestic demand for Treasuries would be discernably different today than it was eight months ago.

- Federal Reserve as a Treasury Buyer

Last year, the Federal Reserve reduced the size of its balance sheet by selling some of its U.S. Treasury holdings. This incremental supply increase pushed down Treasury bond prices and pushed up Treasury yields. However, with the stock market correction that took place in Q4 2018 and with economic numbers weakening, the Federal Reserve is signaling that it will soon cease its selling of U.S. Treasury bonds and begin to buy U.S. Treasury bonds once again. Whether it is to fund the U.S. budget deficit or to push investors back into riskier investments, the Federal Reserve is communicating to investors that large-scale asset purchases of U.S. Treasuries may soon resume. Investors may be buying U.S. Treasuries now to front-run the Federal Reserve and enjoy the price appreciation that could take place once the Federal Reserve becomes a buyer again.

- Negative Yielding Foreign Bonds

As crazy as it may sound, a huge share of government debt across the world pays a negative yield, which means that investors in such bonds are paying government issuers to hold their money for them. A record $12.5 trillion of foreign bonds are now generating a negative yield, and that yield is becoming increasingly more negative as the global economy continues to weaken and as central banks communicate their willingness to do whatever it takes to provide additional monetary stimulus. While U.S. Treasury yields might appear to be low relative to what investors could earn twenty years ago, Treasury yields are high compared to most other sovereign debt in the developed world such as the debt of Japan, Switzerland, Germany, and Sweden.

Perhaps, then, the bond market is making sense. With the economy slowing, baby boomers aging, and the Federal Reserve increasingly inclined to become a Treasury buyer, many investors are finding Treasury bonds to be attractive.

The Stock Market

However, if all of the above is true, why is the S&P 500 Index testing all-time highs right now?

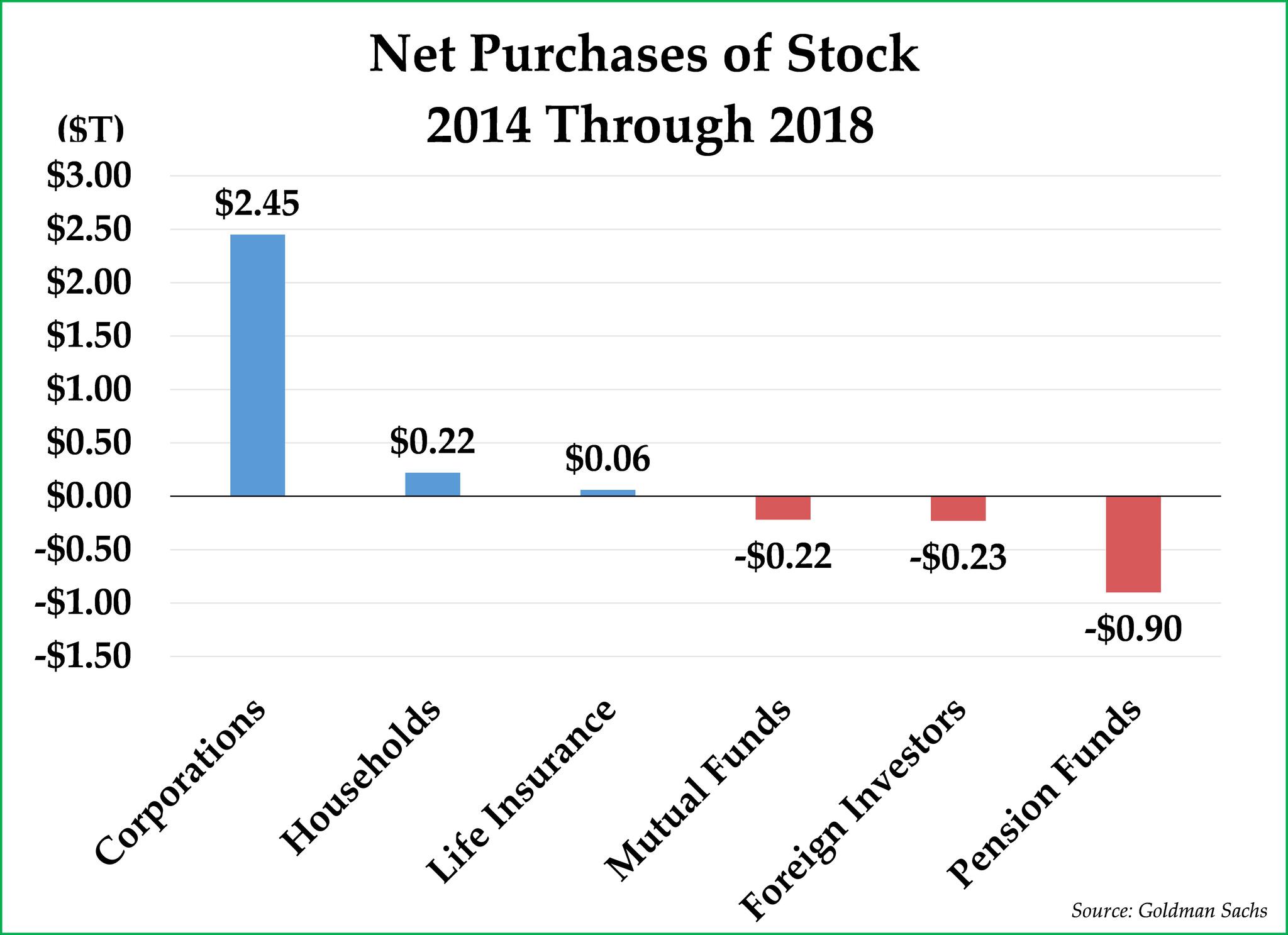

- Corporate Buybacks

With bond yields so low, it remains inexpensive for companies to issue bonds and use those bond proceeds to buy back their own stock. While corporate buybacks create weaker corporate balance sheets and amplify long-term stock market risk, they nevertheless create incremental short-term demand for shares and boost share prices. This trend has been driving the U.S. stock market for the past five years. Also, with corporate bond yields pitifully low, private equity funds can more easily finance the acquisition of publicly traded companies with cheap debt. While baby boomers might be reallocating their investments towards bonds, other investors, namely corporations and private equity firms, are using leverage to buy stocks.

- The Fed “Put”

The U.S. stock market, in many respects, has become a significant driver of the U.S. economy over the past 20 years. Pension plans depend on a rising stock market. So, too, do retirees. Employees with 401(k) plans, while not yet retired, have to increase their savings rate if the U.S. stock market does not continue to deliver attractive returns. The Federal Reserve knows this, and Federal Reserve monetary policy has evolved since the Financial Crisis to focus increasingly on preventing the stock market from correcting. After the correction in December 2018, the Federal Reserve immediately stopped tightening and communicated a far more dovish monetary policy stance. Investors may be buying stocks because they expect the Federal Reserve will do whatever it takes to keep the stock market party going and it simply may be that “There Is No Alternative” to buying U.S. stocks (also known as the “TINA” effect). - Inflation Hedge

The U.S. budget deficit is worsening due to increasing military expenditures, growing medical and retirement entitlements, recently enacted tax cuts, and rising debt service obligations, with no end in sight. At the same time, an emerging consensus is developing that the dollar is too strong relative to other currencies, making it difficult for U.S. manufacturers to compete. President Donald Trump and Senator Elizabeth Warren have both remarked recently that a weaker dollar is a critical factor to America’s future economic competitiveness, and economists like Harvard’s Carmen Reinhart advocate that the Federal Reserve should keep bonds yields well below the inflation rate to reflate the economy. While seemingly overvalued, stocks may be an attractive hedge for those investors looking for inflation protection. - Interest Rate Manipulation

Because the Federal Reserve has enacted policies in recent years to influence not only the interest rate of short-term bonds but also the interest rate of long-term bonds, some investors do not believe that the yield curve provides a useful signal for upcoming recessions and are therefore less concerned about an imminent recession.

Unlike 2008, when the Federal Reserve appeared to be asleep at the switch, central banks around the world appear to be on alert today, for better or for worse, and stand ready to provide markets with liquidity to avoid another crisis. Ultimately, whether the rising stock market or falling bond yields are correct depends in no small part on whether the U.S. economy is entering a recession or just another soft patch.

If a recession is coming or has already arrived, corporate earnings are likely to fall, credit spreads should rise, and corporations will find it more expensive to issue bonds to buy back their own shares, all of which should result in a challenging market for stocks and bonds with high levels of credit risk. Under this scenario, we will be glad to have our clients invested in gold, Treasury bonds, and short-term, high-quality corporate bonds. These securities should provide portfolio stability as investors flock to safe-haven investments while the Federal Reserve cuts interest rates and once again expands its balance sheet to buy U.S. Treasuries.

On the other hand, if the economy is just going through a soft patch rather than a recession, the Federal Reserve’s monetary easing efforts during the second half of the year should reflate the economy and allow the stock market to continue rising, driven by corporate buybacks. Under this scenario, inflation expectations should increase once again along with economic growth as the soft patch recedes. Today, many of the more attractively priced stocks available are cyclical companies, with already pessimistic discounts due to increasing concerns about slowing growth, declining global trade, and growing geopolitical concerns. Should growth re-accelerate, cyclical stocks and the stocks of companies that are exposed to global trade should perform well, similar to what happened in 2017 as economic expectations improved. Under this scenario, stocks could keep rising.

It is much less evident today than it was during the first half of 2008 that the economy is heading into a recession. The New York Fed’s recession probability of 33% does not seem terribly off to us. Of course, the New York Fed does not have a crystal ball on these matters — nor does anybody else. Without knowing the future with any level of certainty, we are keeping our client portfolios diversified, with a constant eye towards committing capital to high-quality businesses which are selling at a sufficiently large discount to their fair values.

We would also suggest that it makes more sense for investors to focus on the big picture rather than what happens to the economy in the next few months. As we see it, U.S. fiscal deficits are set to rise sharply in the coming decade, and it seems unlikely that foreign investors will pick up the tab. We expect the Federal Reserve to fill in the gap, buying U.S. Treasuries to fund these deficits. This scenario is likely to cause the U.S. dollar to depreciate and create an environment where gold and stocks rise in nominal price while long-term Treasury bonds are unable to compensate investors adequately for the inflation risk they are taking. As this occurs, the choice between more volatility and more inflation protection versus less volatility and less inflation protection will become an increasingly important topic of conversation for investors.

Thank you for your trust in asking us to build your financial plan and invest your capital in accordance with your risk tolerance, your life goals, and your investment values. We hope you and your family have a wonderful summer.

Please do not hesitate to reach out to us with any questions.

This commentary is prepared by Pekin Hardy Strauss, Inc. (dba Pekin Hardy Strauss Wealth Management, “Pekin Hardy”) for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any security. The information contained herein is neither investment advice nor a legal opinion. The views expressed are those of the authors as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. Although information has been obtained from and is based upon sources Pekin Hardy believes to be reliable, we do not guarantee its accuracy. There are no assurances that any predicted results will actually occur. Past performance is no guarantee of future results.