The author of The Communist Manifesto was not just a philosopher and political theorist; he was also an economist. In the 19th century, which is when Karl Marx was thinking and writing about politics, money was indeed gold and silver – or at least explicitly backed by gold and silver. One could walk into a bank and redeem U.S. dollars, British pounds, or any other common currency for physical gold. His profound statement underscores a fundamental truth that lost some relevance after the United States left the gold exchange standard in 1971 but has gained renewed significance in today’s economic landscape. Increasingly, investors and central banks have a renewed recognition that gold is a form of money with enduring value.

The last time we discussed the topic of gold in any amount of depth was after Q2 2020, at the end of a 12-month period when the gold price had just risen by 27%. We remained long-term bullish on gold then, as we remain long-term bullish now. With that said, the pathway for the price of gold has been choppy, although generally positive, and we expect the future path for gold to rhyme with the past. After our Q2 2020 letter was written, the gold price stagnated for the next 2.5 years before the bull market in gold resumed at the end of 2022.

Rather than rehash the arguments that we put forth in our Q2 2020 letter, most of which remain compelling reasons to own a core position in gold during the 2020s, we are going to discuss what has changed since then that might be causing the price of gold to rise of late. Over the last six months, the price of gold has risen 20% to reach new all-time highs (see chart on the previous page), during a period where the dollar has strengthened relative to other currencies.1

We have been asking ourselves, given the strength of the dollar, why would the price of gold be rising? In summary, we would answer that the price of gold has increased due to increasing monetary debasement, private demand in China and in other emerging market countries, and central bank policy-related demand. Importantly, we see no near-term catalyst to reverse these bullish trends.

Monetary Debasement

Since June 2020, as we expected, monetary debasement of the U.S. dollar has not just continued; it has accelerated. The money supply, as measured by M2, increased from $18.1 trillion to $20.9 trillion currently. Meanwhile, the Consumer Price Index (CPI) has increased by 21% cumulatively, which means the price of a basket of goods in the United States is now 21% higher today than it was in June 2020. Moreover, it appears that monetary debasement is set to accelerate, with the United States continuing to post very large Federal deficits and the Federal Reserve signaling that they may reduce interest rates, despite the fact that inflation remains well above its 2% long-term goal.

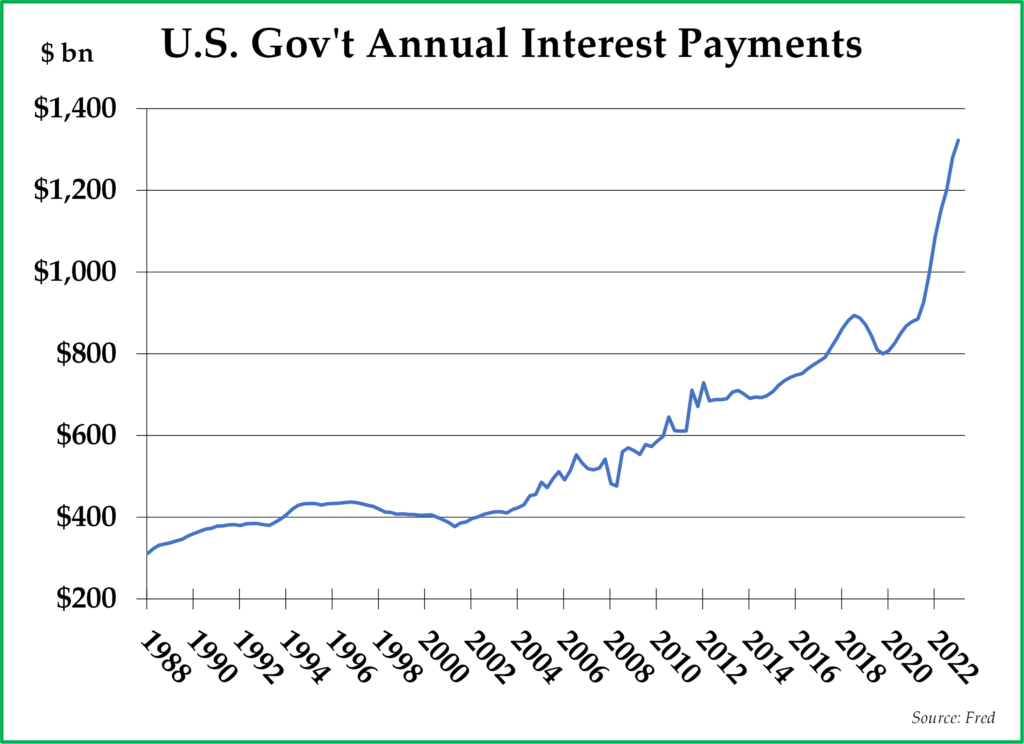

Moreover, with debt increasing and interest rates increasing since June 2020, interest payments on U.S. Government debt are skyrocketing. Current spending on debt service is now above $1.2 trillion (see chart on the previous page) and exceeds the annual spending of the Department of Defense. In addition, interest expenses are accelerating as old debt matures and is refinanced with new debt at higher interest rates. In our view, we are getting closer to the point where the Federal Reserve may have to start funding the U.S. government’s growing deficits by buying U.S. Treasuries and capping interest rates at a low level, a process also known as yield curve control or debt monetization.

Emerging Market Investor Demand

While investors across emerging markets in Asia are participating in the growing demand for gold, Chinese investors in particular have emerged in driving substantial demand for gold. With a weak domestic real estate market and a falling stock market, Chinese investors are looking for more stable stores of value for their growing wealth. Because of capital controls, Chinese investors have limited investment options, and it appears that gold may be receiving capital flows that may have previously gone into stocks or real estate.

Interestingly, U.S. investors appear to be selling gold, reflected by the recent declines in the assets under management of U.S. gold ETFs, even in the face of a rising gold price. As gold keeps reaching new highs, gold headlines are sparse, and the excitement level about the rising gold price is muted among investors. Should U.S. investors choose to move more of their capital into gold, that would be another tailwind for the gold price. However, for now, waning U.S. investor demand represents a headwind for higher gold prices.

Central Bank Purchases

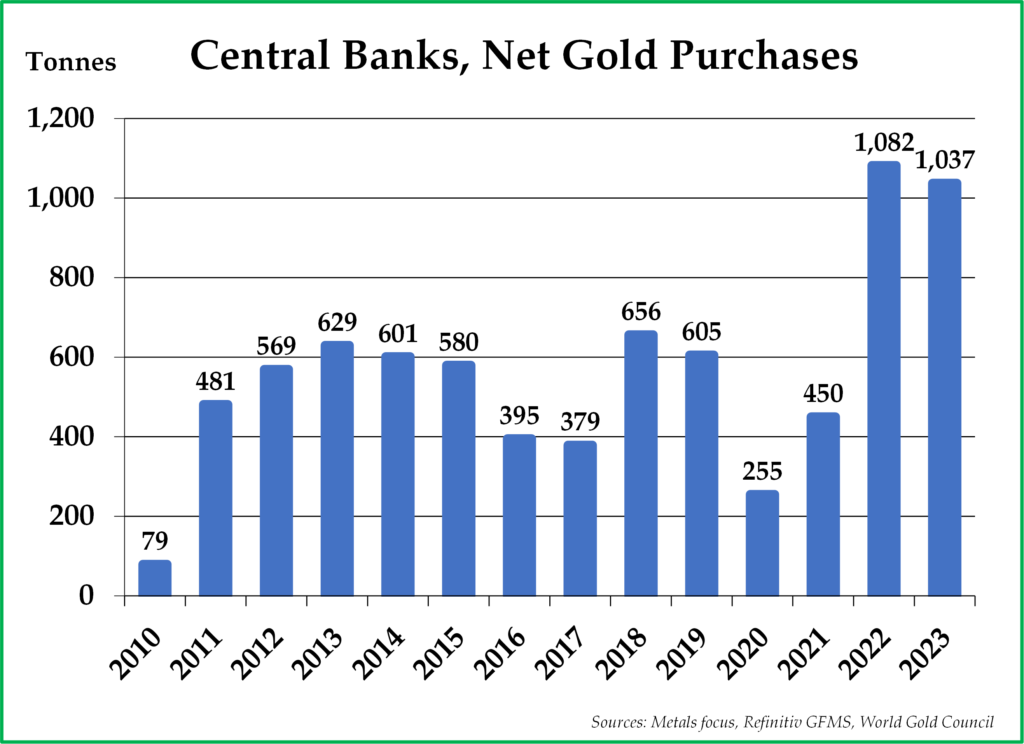

Central banks worldwide have significantly increased their gold purchases, marking a notable shift in reserve asset allocations. For the second consecutive year, central banks purchased more than 1,000 metric tons (tonnes) of gold (see chart on the next page), which is far higher than normal and more than triple the amount of gold that is mined out of the ground each year. The rationale behind this surge in central bank buying is multifaceted.

First, central banks view gold as a hedge against currency risks and a means to diversify their foreign currency reserves. Gold’s intrinsic value and historical role as a store of wealth make it an attractive asset for central banks seeking stability amid economic uncertainty.

Second, the evolving geopolitical landscape has influenced central bank behavior regarding gold acquisitions. The imposition of sanctions and geopolitical tensions by the United States and Europe, such as those applied to Russia after the Ukraine invasion, have raised concerns about the confiscation risk of owning traditional reserve currencies and sovereign debt. As a result, central banks have bolstered their gold reserves significantly ever since the sanctions against Russia were announced.

Third, the evolution of alternative monetary systems, notably exemplified by initiatives driven by the BRICS countries (Brazil, Russia, India, China, and South Africa), has reshaped perceptions of gold as a settlement reserve asset. A growing consortium of countries have embarked on a path to establish a parallel monetary framework that reduces dependency on traditional reserve currencies. Instead of conducting trade in U.S. dollars, Euros, or Japanese Yen, these countries are trading with each other in their respective local currencies, with gold serving as a neutral settlement asset to address any imbalances. This approach promotes financial autonomy and resilience, reducing vulnerabilities associated with reliance on the U.S. dollar. Central to this alternative system is the recognition of gold as a stable and universally accepted medium of exchange, particularly in cross-border transactions.

Shift in Physical Gold Flow

Due to many of the trends described already, the dynamics of physical gold flow have undergone a noticeable transformation, reflecting changing market sentiments and geopolitical shifts. Traditional gold hubs in the West, such as London and Switzerland, have experienced a decline in gold inventories and trading activity. This shift is attributed to several factors, including subdued investor interest in Western markets, declining ETF inventories, and waning COMEX open interest.

As a result, physical gold appears to be flowing from west to east, with emerging economies in Asia, particularly China, emerging as a key driver of gold demand. The rise of private investors in these regions, coupled with a cultural affinity for gold as a store of wealth, has also contributed to the eastward migration of gold flows. The net result of this shift in physical flows is that the price is increasingly being determined in Asia rather than in the West.

To conclude, we believe the surge in gold prices over the past six months reflects monetary debasement, emerging market investor demand and especially Chinese investor demand, central bank purchases, and important shifts in physical gold flow. Just looking at central bank demand for gold by itself being more than triple the annual mining supply, it would be hard to understand the gold price not rising as it has lately.

As geopolitical uncertainties persist and traditional financial paradigms evolve, we think gold is likely to increase in relevance from here as a strategic asset that transcends borders and economic cycles, with a higher commensurate with its increased relevance and, conversely, with the dollar’s depreciating value.

We have said this before, but we would reiterate that we think gold is poised to outperform the S&P 500 Index over the next decade, as it has over the past several years. As a result, we are bullishly positioned in gold in most of our client portfolios and are likely to remain so until the strong fundamentals that are driving higher gold prices change.

*****

We are grateful for your trust in our management of your investable assets and will continue to deploy your capital with prudence and discipline.

Sincerely,

Pekin Hardy Strauss Wealth Management

1 The chart on page one includes the six-month period that includes Q4 2023 and Q1 2024. As we are publishing this letter in April 2024, the price of gold has appreciated further to $2,412/ounce as of April 16, 2024.

This commentary is prepared by Pekin Hardy Strauss, Inc. (dba Pekin Hardy Strauss Wealth Management, “Pekin Hardy”) for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of any security. The information contained herein is neither investment advice nor a legal opinion. The views expressed are those of the authors as of the date of publication of this report, and are subject to change at any time due to changes in market or economic conditions. Although information has been obtained from and is based upon sources Pekin Hardy believes to be reliable, we do not guarantee its accuracy. There are no assurances that any predicted results will actually occur. The S&P 500 Index includes a representative sample of 500 hundred companies in leading industries of the U.S. economy, focusing on the large-cap segment of the market. The Consumer Price Index (CPI) is an unmanaged index representing the rate of the inflation of U.S. consumer prices as determined by the U.S. Department of Labor Statistics.